Bank loan income may decline if the Federal Reserve cuts interest rates. That doesn't mean investors should avoid them altogether, but it's important to understand the risks.

The Federal Reserve is expected to lower its benchmark interest rate this year. As a result, investors holding short-term bonds that are maturing soon may face lower reinvestment rates.

Fed rate cuts should also mean declining coupon rates for investments with floating coupon rates, like bank loans. Bank loans are a type of corporate debt with a number of unique characteristics that differentiate them from traditional corporate bonds. They go by a number of different names, including "leveraged loans" or "senior loans."

Bank loans generally offer higher yields than many other fixed income investments, but those higher yields come with greater risks. This article will provide a broad overview of bank loans so investors can have a better understanding of how they work and how they may fit into a portfolio.

The basics of bank loans

Bank loans are a type of corporate debt with a number of unique characteristics:

- Sub-investment-grade credit ratings: Bank loans tend to have sub-investment-grade credit ratings, also called "junk" or "high-yield" ratings. Junk ratings are those rated BB+ or below by Standard and Poor's, or Ba1 or below by Moody's Investors Services.1 A sub-investment-grade rating means that the issuer generally has high credit risk, or a greater risk of default, so bank loans should always be considered aggressive investments.

-

Floating coupon rates: Bank loan coupon rates are usually based on a short-term reference rate plus a spread. The short-term reference rate can vary, but it's usually the one- or three-month term Secured Overnight Financing Rate, or SOFR. For years, the reference rate was generally the three-month London Interbank Offered Rate (LIBOR), but that rate was retired in June 2023. The spread on the reference rate is the compensation for lending to a riskier company. Since bank loans come with increased risks—keep in mind that they're junk-rated—investors demand higher yields in case the issuer cannot make timely interest or principal payments. For example, a bank loan's coupon rate might be one-month term SOFR rate plus 3%. If the SOFR rate was 5%, then the annualized coupon rate would be 8%. Spreads can vary by each loan issue, depending on the creditworthiness of the issuer. Spreads can be as low as 1.5% for issues rated in the BB/Ba area by S&P or Moody's, respectively, and can be over 5% for riskier issues.

-

Secured by the issuer's assets. Bank loans are secured, or collateralized, by the issuer's assets, like inventory, plant, property, and/or equipment. They are senior in a company's capital structure, meaning they rank above an issuer's traditional unsecured bonds. Despite that senior and secured status, bank loans can still default and therefore should be considered risky investments given the aforementioned junk ratings.

- The potential to be redeemed prior to maturity. Bank loans generally have stated maturity dates, but the issuer can usually "call" the bond, or repay it, at any time prior to maturity. That call option is usually for the issuer's benefit, since they tend to call a loan when borrowing conditions have improved and can issue a new loan with a lower spread.

Bank loans are generally only available for large institutional investors, so most individual investors can only access the market through a mutual fund or exchange-traded fund (ETF). They also tend to be relatively illiquid; liquidity is the measure of how easily a security can be sold without incurring high transaction costs or a reduction in price.

For Schwab clients interested in learning more about funds with exposure to bank loans, clients can log in to use our mutual fund screener or ETF screener. For both, clients need to look under "taxable bonds” and then select "bank loans" as the category.

Portfolio construction and performance

Bank loans should generally be considered complements to a well-diversified fixed income portfolio. Given their greater risk of default and potentially large drawdowns, investors should consider them in moderation.

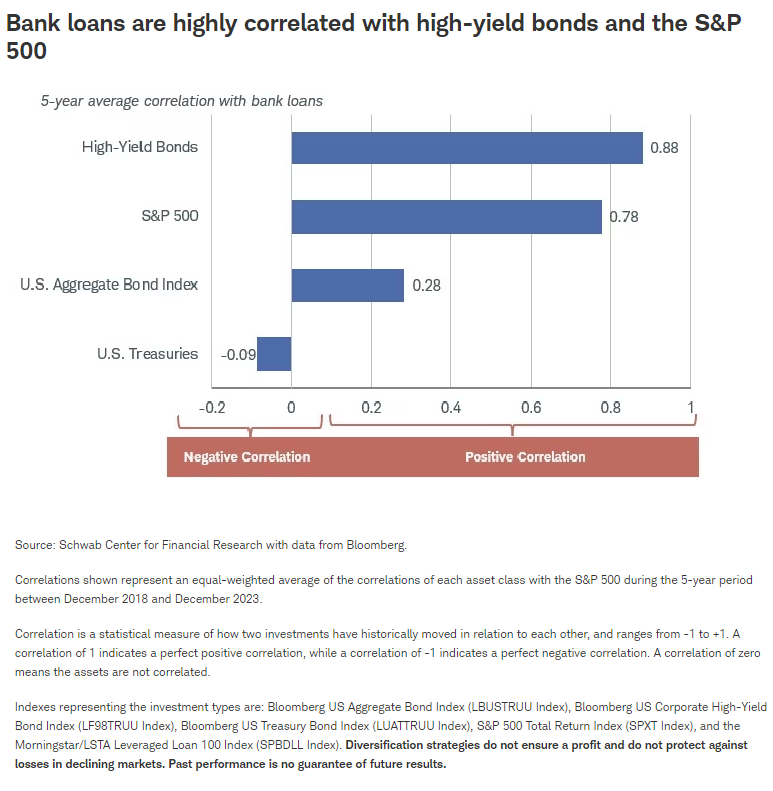

Bank loans have been highly correlated with both high-yield bonds and stocks over the last five years, with a negative correlation with U.S. Treasuries, meaning they generally don't provide much diversification from equities. That's important for investors to consider when adding bank loans to a portfolio. It helps to have investments that don't always move in the same direction, because that can smooth out performance. Given those high correlations to stocks and high-yield bonds, bank loans might not help reduce the volatility of a portfolio the way Treasuries or other highly rated bond investments might.

When considering bank loans, it's important to differentiate between interest rate risk and credit risk. Interest rate risk is the risk that a bond's price would fall if its yield increased. It's one of the foundational characteristics of bonds—that their prices and yields generally move in opposite directions. Bank loans and other floating-rate investments have low interest rate risk because the coupon rates adjust when yields rise, meaning prices don't need to fall.

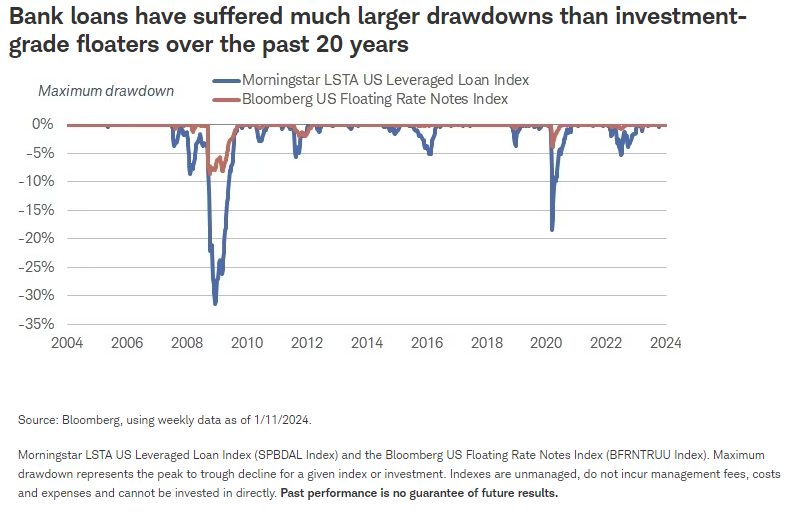

Bank loans have high credit risk, given the low credit ratings and greater likelihood of default. The chart below compares the maximum drawdowns of the Morningstar LSTA Leveraged Loan Index (bank loans) and the Bloomberg US Floating Rate Notes Index, an index of investment-grade rated corporate bonds with floating coupon rates. Drawdowns for the bank loan index have been significantly larger than those of investment-grade floaters over the last 20 years. Keep in mind that this chart only shows drawdowns, which might be important for investors who don't have the risk tolerance for such drops. But over time, bank loans have posted higher average total returns than investment-grade floaters, but with more volatility.

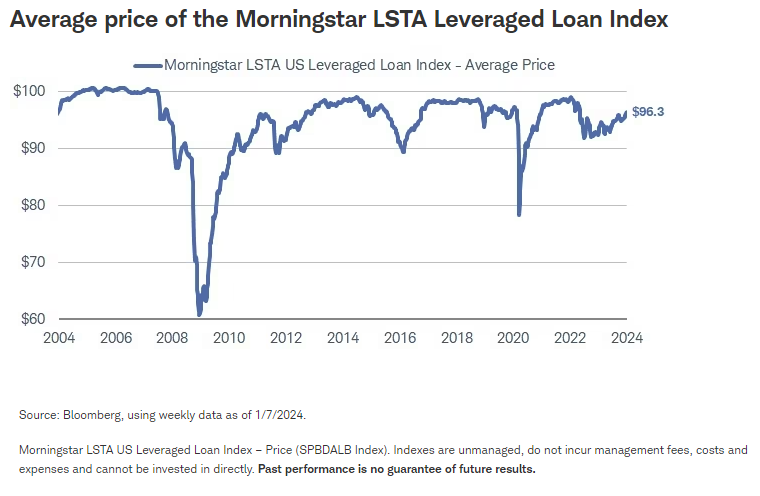

Another feature of bank loans is the asymmetric price movements. Prices can (and do) fall if there are concerns about the economy and the overall ability of loan issuers to repay their debt obligations. A plunge in price, shown below, is what drives the drawdowns shown above. But loan prices rarely rise above their $1,000 par values due to their call features. If a loan price were to rise to or above par, the issuer would likely refinance it with a new loan with better terms for the issuer.

That limits the upside for bank loan prices, especially when interest rates are falling. Because bond prices and yields generally move in opposite directions, falling yields can help pull up the values of fixed-rate bond investments, but that's not necessarily the case with bank loans.

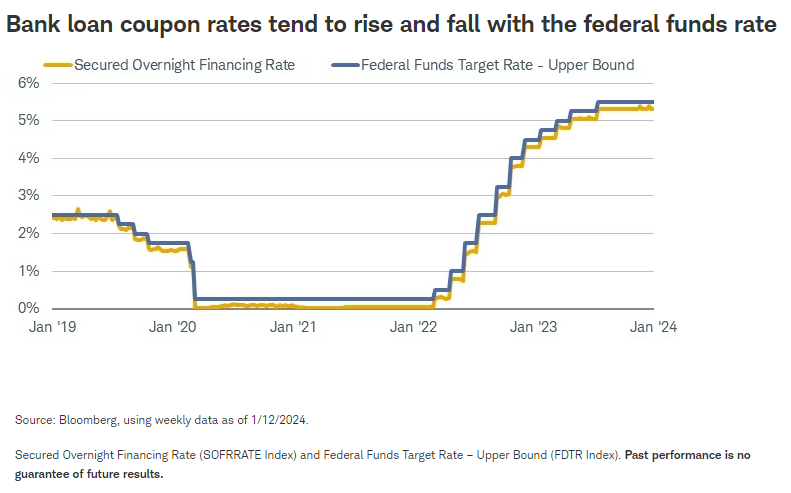

The direction of Federal Reserve policy is another important consideration. Investors are generally rewarded with higher coupon payments as the Fed raises interest rates since the Secured Overnight Financing Rate tends to track the federal funds rate. But that positive can become a negative once rate cuts seem likely, and investors might want to consider locking in investments with fixed coupon rates rather than risk seeing their coupon payment decline.

We expect the Fed to cut rates three times this year, potentially bringing the federal funds rate target to the 4.5% to 4.75% range. The median Federal Open Market Committee (FOMC)projection suggests three rate cuts, as well. Assuming inflation continues to ease, "real" interest rates—those adjusted for inflation—could continue to rise if the Fed holds steady. Cutting rates as inflation falls allows the Fed to maintain a restrictive policy.

What to consider now

Investors who hold or are considering investing in bank loan funds should be prepared for their income payments to decline as the Fed cuts rates. That doesn't mean investors need to avoid bank loans today, however, because they still offer relatively high yields and the prospects of a "soft landing," or an economic slowdown that avoids recession, can help keep their prices supported. However, we suggest any investment be done in moderation.

We've been suggesting investors consider intermediate- or long-term bonds to lock in yields with certainty rather than face reinvestment risk with short-term bonds once the Fed begins cutting rates, as we expect later this year. That guidance rings true for bank loans as well, as their coupons should gradually decline over time.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Bank loans typically have below investment-grade credit ratings and may be subject to more credit risk, including the risk of nonpayment of principal or interest. Most bank loans have floating coupon rates that are tied to short-term reference rates like the Secured Overnight Financing Rate (SOFR), so substantial increases in interest rates may make it more difficult for issuers to service their debt and cause an increase in loan defaults. A rise in short-term references rates typically result in higher income payments for investors, however. Bank loans are typically secured by collateral posted by the issuer, or guarantees of its affiliates, the value of which may decline and be insufficient to cover repayment of the loan. Many loans are relatively illiquid or are subject to restrictions on resales, have delayed settlement periods, and may be difficult to value. Bank loans are also subject to maturity extension risk and prepayment risk.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in a declining market.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab