Short-term bond yields are high currently, but with the Federal Reserve poised to cut interest rates investors may want to consider longer-term bonds or bond funds.

High-quality bond investments remain attractive. With yields on investment-grade-rated1 bonds still near 15-year highs,2 we believe investors should continue to consider intermediate- and longer-term bonds to lock in those high yields. By focusing more on short-term bond investments, investors likely will face reinvestment risk once the Federal Reserve begins to cut interest rates, as it is widely expected to do this year.

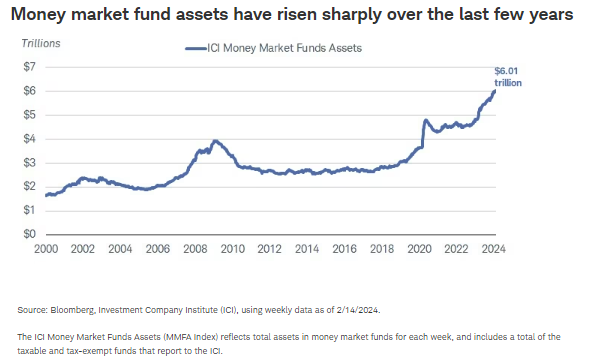

However, investors may be a bit reluctant to do that given how high short-term yields are. Why invest in a longer-term bond when it offers a lower yield than what you can earn in short-term investments like Treasury bills, short-term certificates of deposit (CDs), or money market funds? It's a question we're asked often, and if it's a question you're asking, you're likely not alone. The amount of money market fund assets has been rising sharply for years—their yields have risen sharply following the aggressive pace of Federal Reserve rate hikes that began nearly two years ago.

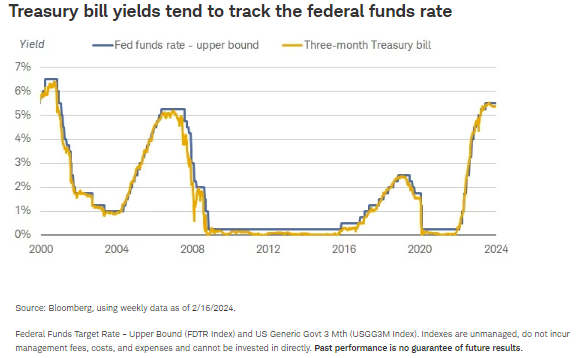

Short-term bond yields, and the funds that hold them, are admittedly attractive today. Three- and six-month Treasury bill yields are above 5%, at levels not seen since before the global financial crisis of 2008-2009. Those high yields come with relatively low volatility and generally lower price declines versus securities with longer-term maturities when yields rise. If you own a three-month Treasury bill and other Treasury bill yields rise, the price of your three-month bill might not fall much because it matures so soon, and when it matures you can reinvest at a higher interest rate.

However, if you hold a five-year Treasury note and yields rise, you'll have to wait a long time for it to mature before you can take advantage of those higher yields. If you wanted to sell that note in the secondary market, it would likely be sold at a discount because the buyer would need the additional price appreciation to make up for that income gap. That's why intermediate- and long-term bond prices tend to be more volatile than short-term bond prices.

Treasury bill yields are highly sensitive to changes in the Federal Reserve's benchmark federal funds rate, which is set by the Federal Open Market Committee and is the rate at which U.S. banks lend money to each other overnight. When the federal funds rate rises, Treasury bill yields tend to follow. On the flip side, when the Fed is lowering rates, Treasury bill yields tend to fall. That opens up investors to reinvestment risk, or the risk that interest rates decline and maturing bond proceeds are re-invested at lower yields.

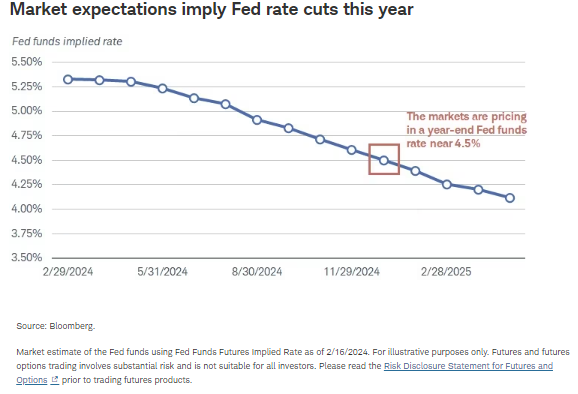

The Fed has held rates steady since it raised rates to the 5.25% to 5.5% range in July 2023, but projections from the Fed as well as market expectations suggest that rate cuts are likely on the horizon. The median projection from Fed officials suggests that the Fed could cut rates to the 4.5% to 4.75% area this year. Market expectations, implied from the federal funds futures market, are just a bit more aggressive and are pricing in a year-end rate just below 4.5%.

With rate cuts likely coming soon, reinvestment risk is becoming much more real. Investors who have been holding short-term bond investments would likely be faced with lower yields when reinvesting their proceeds from maturing bonds.

Waiting for the Fed to cut rates before considering longer term bonds isn't our preferred approach. The bond market is forward-looking and long-term Treasury yields typically decline once investors believe that rate cuts are coming.

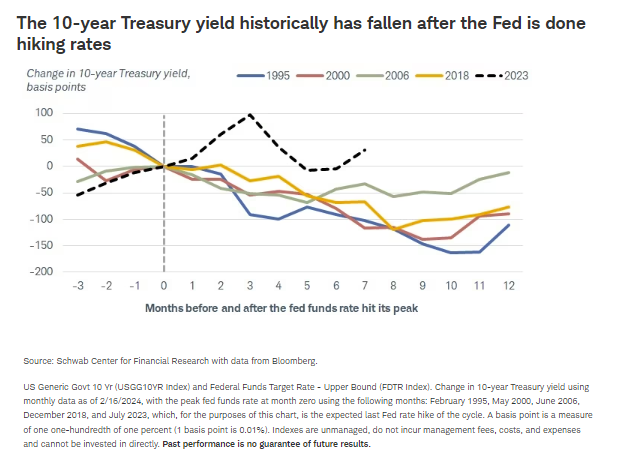

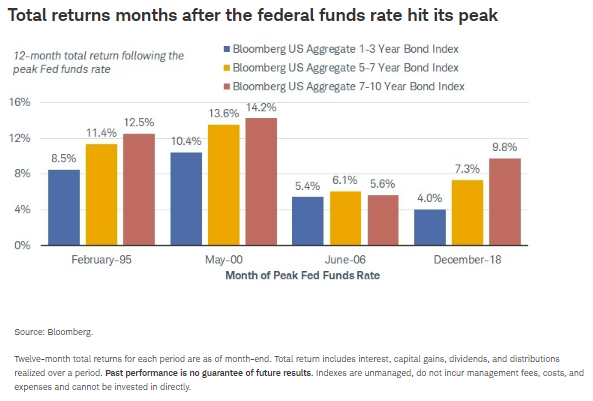

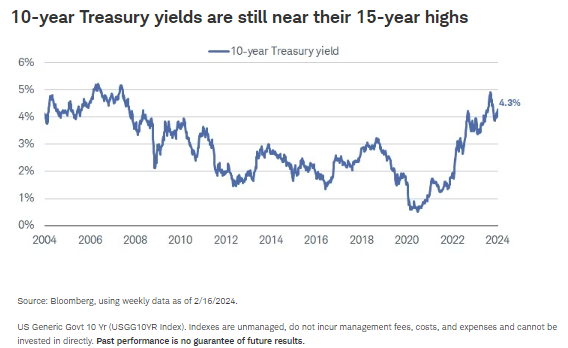

The chart below highlights this relationship—and highlights how different this cycle has been. Over the previous four rate hike cycles, the 10-year Treasury yield has tended to peak before the Fed hits its peak rate. Over the next 12 months, the 10-year Treasury yield declined.

This time has been different: The 10-year Treasury yield has been hovering in a range above where it was when the Fed last hiked in July 2023. We believe the historical relationship should hold and we expect the 10-year Treasury ultimately to decline modestly from current levels as growth and inflation slow. Investors who wait too long to consider locking in long-term yields may end up investing in lower yields than what are available today.

A quick look at short-term total returns supports the case for investing in longer-term bonds once the federal funds rate hits its peak. Over the last four rate hike cycles, intermediate-term bonds outperformed short-term bonds in the 12 months following the last Fed hike of each cycle.

The chart below focuses on 12-month total returns, which includes interest payments and price appreciation or depreciation. A total return is different from a yield—when you invest in a bond and hold it to maturity, your average annualized return will be pretty close to the starting yield of that bond. But in the short run, the price of bonds (or bond funds) can fluctuate depending on market conditions, as bond prices and yields generally move in opposite directions. The magnitude of those price fluctuations is generally tied to the bonds' time to maturity, with short-term bond prices generally having less interest rate sensitivity than bonds with longer maturities.

We compared the total returns of the 1-3 year subset of the Bloomberg U.S. Aggregate Index (short-term bonds) to those of the 5-7 and 7-10 year subsets to represent intermediate-term bonds. In each of the four previous rate-hike cycles, the intermediate-term indexes outperformed the short-term index, and often by a wide margin.

These total returns might not matter for investors who are holding a portfolio of bonds to maturity or hold bond funds for long periods of time. But even if bond total returns are unrealized they can provide more of a boost to a portfolio compared to a portfolio that holds just short-term bonds.

Yields are still high for intermediate-term, high-quality bond investments. Focusing just on yield or income earned, investing in intermediate-term Treasuries hasn't been this attractive in more than 15 years.

Yes, the 10-year Treasury yield is off its recent peak of 5% from last October, but we don't expect it to get back to that level as inflation continues to trend lower. Hope is not an investment strategy. Rather than hope that the 10-year Treasury yield rises back to 5%, keep in mind that a yield over 4% hadn't been seen in years prior to that.

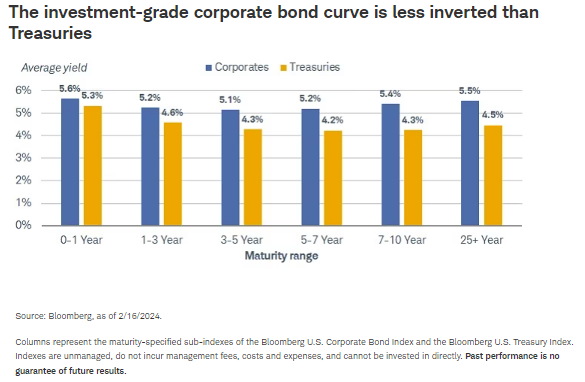

Investors who are still concerned about the inverted yield curve and the idea of earning lower yields by investing in long-term bonds might want to consider investment-grade corporate bonds. Just like Treasuries, very short-term corporate bonds, like those maturing in less than a year, generally offer the highest yields. But beyond one year to maturity, the corporate bond yield curve is much flatter. By considering corporate bonds in the 7- to 10-year maturity range, the average yield is just 0.2% lower than very short-term corporates. With Treasuries, investors generally earn a full percentage point less by considering 7- to 10-year Treasuries rather than Treasury bills.

What to consider now

We suggest investors consider high-quality, intermediate- or long-term bond investments rather than sitting in cash or other short-term bond investments. With the Fed likely to cut rates soon, we don't want investors caught off guard when the yields on short-term investments likely decline as well. We'd rather lock in high yields now than risk earning lower yields down the road.

For investors in or near retirement, locking in these high yields with high quality investments means that you likely don't need to invest as heavily in riskier investments to meet your goals.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

2 Bloomberg US Corporate Bond Index average yield-to-worst of 5.4% as of 2/20/2024.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Money Market Funds-An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in a declining market.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Some of the statements in this document may be forward looking and contain certain risks and uncertainties.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab