Family Affair: A Look at Sector Trends

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThis year is slightly more than four months old, and despite a seemingly calm ride for the market (at least at the index level), there has been considerable churn under the surface. We've written about the weakness seen at the individual member level, but in this report, we'll look a couple levels up at the 11 S&P 500 sectors. The story of subsurface churn is still the same, but there have been key leadership shifts over the past few months, many of which have occurred in a somewhat stealthy way.

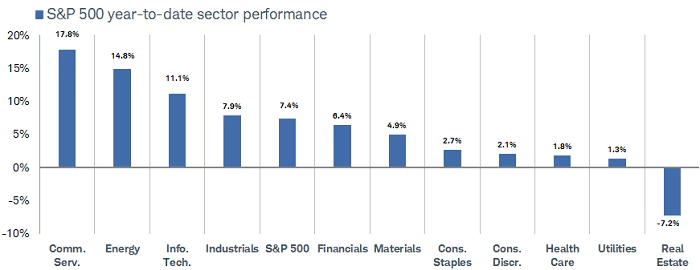

The chart below shows a year-to-date performance derby for all 11 sectors. You can see that Communication Services is maintaining a healthy lead at nearly 18%, while Real Estate is the only laggard and down by more than 7%.

Real Estate lags

Source: Charles Schwab, Bloomberg, as of 4/12/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested indirectly. Past performance is no guarantee of future results.

For the most part, Communication Services has not lost its top spot this year, thanks to considerable performance from a few mega-cap members; the two largest in the sector are Alphabet and Meta, which are the fourth- and sixth-largest companies in the S&P 500, respectively.

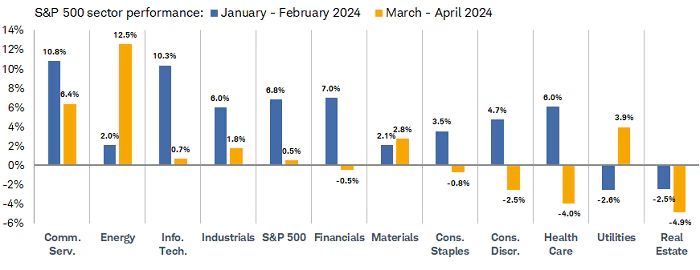

Perhaps more interesting is the jump Energy has made over a rather short timeframe. As you can see in the chart below, from January through February (shown via the blue bars), Energy was one of the weaker performers with just a 2% gain (outpacing only Utilities and Real Estate). The two dominant performers in those months were Communication Services and Tech. However, since March, Energy has asserted its dominance and is outperforming all other sectors by a wide degree. Not only has its 12.5% gain trounced Tech's 0.7% gain, but it's nearly double the gain for Communication Services.

Energy jumps the line

Source: Charles Schwab, Bloomberg, as of 4/12/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested indirectly. Past performance is no guarantee of future results.

It's understandable that Energy's swift comeback might be associated with (or due to) the recent jump we've seen in inflation pressures and energy prices. The consumer price index (CPI) reading in March was hotter than expected, confirming that the relatively hot prints in January and February were not blips. Additionally, oil prices (using Brent crude as the proxy) are up by nearly 18% year-to-date.

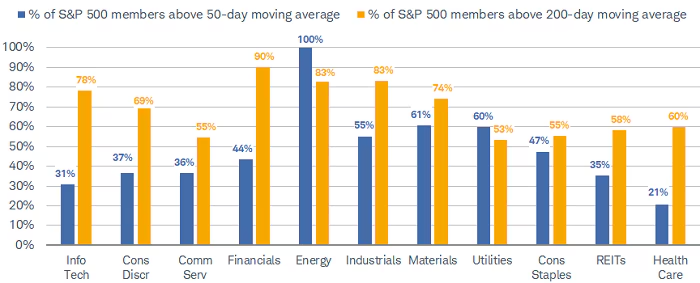

Not only have those factors helped boost Energy's performance, but the sector's underlying breadth also looks quite strong. As shown in the chart below, as of last Friday's (April 12th) close, every member in the Energy sector is trading above its 50-day moving average. For the percentage trading above their 200-day moving average, the share drops to 83%. Even though Financials scores better on the latter metric, you can see the sector is suffering more from a momentum drop of late, given only 44% of its members are trading above their 50-day moving average.

Energy's fresh breadth

Source: Charles Schwab, Bloomberg, as of 4/12/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested indirectly. Past performance is no guarantee of future results.

Our Sector Views

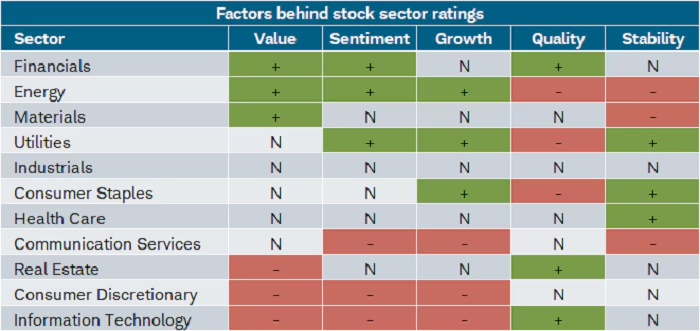

The relatively strong performance and (long-term) breadth in sectors like Energy and Financials are consistent with what our sector ratings show. For those who might not be as familiar, we recently revamped our Sector Views model and process after a two-year hiatus. As shown in the table below, you can see that Energy, Financials, and Materials are rated as "outperform" while Real Estate and Consumer Discretionary are rated "underperform" (the rest are marketperform").

Source: Schwab Center for Financial Research, as of 3/18/2024.

The ratings Outperform, Marketperform, and Underperform reflect SCFR's opinions about the likelihood that the sector will perform better (outperform), about the same (marketperform), or worse (underperform) than the broader S&P 500® index during the next six to 12 months. Sectors are based on the Global Industry Classification Standard (GICS®), an industry analysis framework developed by MSCI and S&P Dow Jones Indices to provide investors with consistent industry definitions. Sectors are listed in the above chart in order of their performance in five factors that are shown in the chart below. Sectors are part of the Global Industry Classification Standard (GICS) grouping. The classification includes four levels or groupings of companies that make up the U.S. stock market. These groupings (as well as the number of constituents in each category as of April 2023) are as follows: • Sectors (11) • Industry Groups (25) • Industries (74) • Sub Industries (163). The information here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Investing involves risk, including loss of principal.

Thanks to our colleagues in the Schwab Equity Ratings (SER) department, we're able to look at a variety of factors to help construct our ratings. You can see them laid out in the following table, along with how each sector scores for each factor. This is the quantitative-driven part of the model, which we marry with our qualitative, top-down analysis to arrive at each rating. For context, we don't look solely at the number of negative and positive factor scores for each sector to construct a rating. For example, the Tech sector scores quite poorly in areas like valuation, but we think the sector's higher-quality characteristics (like strong cash positions, among others) should keep it as a "marketperform."

Source: Schwab Center for Financial Research, S&P Dow Jones Indices, as of 3/18/2024.

Sectors are ranked as positive (+), neutral (N) or negative (—) for each of the five factors based on the sector's relative ranking (from 1-11) in each factor: 1-3 is positive, 4-8 is neutral, and 9-11 is negative. See Important Disclosures for an explanation of the Value, Growth, Quality, Sentiment and Stability factors and their inputs. The Schwab Center for Financial Research reserves the right to override the Schwab Sector Views Model.

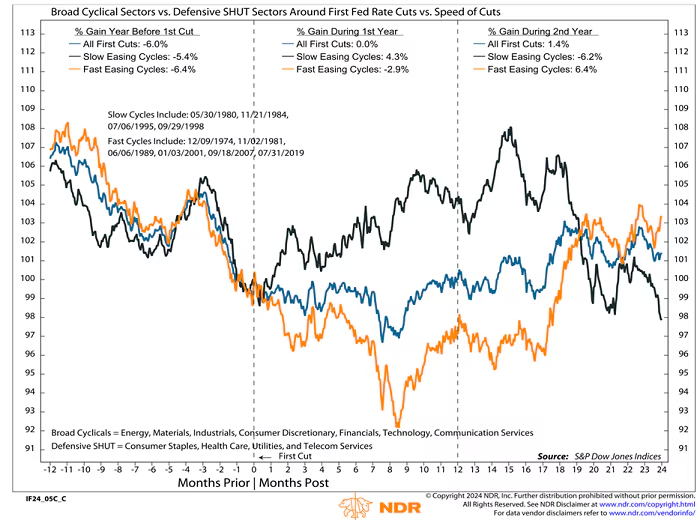

Paper cuts preferred for cyclicals

We think that cyclically oriented segments of the market can continue to do well as long as our thesis of rolling recessions turning into rolling recoveries remains intact. So far, that continues to be the case, evidenced by the fact that manufacturing sentiment, housing, and capital spending have started to turn a corner after being mired in a slowdown for a couple years.

Additionally, we think that once the Federal Reserve starts embarking on its rate-cutting cycle, it is likely to opt for a slow cycle (defined as cutting less than five times in a 12-month period). As shown via our friends at Ned Davis Research (NDR) in the chart below, slow cutting cycles tend to benefit cyclical sectors relative to defensives. In the case of what NDR shows, the cyclical group includes Energy, Materials, Industrials, Consumer Discretionary, Financials, Tech, and Communication Services.

Speed of easing cycles important for sector leadership

Source: ©Copyright 2024 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. 1974-4/15/2024. The chart and embedded tables show broad cyclical and defensive sector performance around first Fed rate cuts. Y-axis is indexed to 100 at start of first rate cut. An index number is a figure reflecting price or quantity compared with a base value. The base value always has an index number of 100. The index number is then expressed as 100 times the ratio to the base value. A fast easing cycle (orange line) is one in which the Fed cuts rates at least five times a year. A slow easing cycle (black line) has less than five cuts within a year. Blue line represents all first cuts. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

Deep rate cuts would likely be consistent with the Fed responding to unwanted and unexpected weakness in the economy—likely in the labor market. Also shown in the chart above via the orange line is that fast-cutting cycles have historically been consistent with significant relative underperformance for cyclical sectors. That isn't too surprising since a recession-induced bear market would likely send investors piling into traditional defensives (like Consumer Staples and Utilities).

In sum

Investors should be mindful of the large and swift leaderships shifts that have happened under the surface of the major indexes. Our sector ratings continue to favor segments of the market that benefit when the economy is entering a recovery and moving into expansion. Importantly, though, we put an equal amount (if not more) emphasis on the factors mentioned above. Investors should continue to keep an up-in-quality bias when it comes to looking for characteristics like free cash flow yield, profitability, and strong cash positions. We think those factors are among several in the high-quality arena that will do well in a slow Fed cutting cycle.

About the Authors

Liz Ann Sonders, Managing Director, Chief Investment Strategist

Liz Ann Sonders has a range of investment strategy responsibilities, from market and economic analysis to investor education, all focused on the individual investor.

A keynote speaker at numerous company and industry conferences, Liz Ann is regularly quoted in financial publications including The Wall Street Journal, The New York Times, Barron's, and the Financial Times, and she appears as a regular guest on CNBC, Bloomberg, CNN, CBS News, Yahoo! Finance, and Fox Business News programs. Liz Ann has been named "Best Market Strategist" by Kiplinger's Personal Finance and one of SmartMoney magazine's "Power 30." Barron's has named her to its "100 Most Influential Women in Finance" every year since the list's inception, and Investment Advisor has included her on the "IA 25," its list of the 25 most important people in and around the financial advisory profession. Liz Ann has also been named to Forbes' 50 Over 50.

In 1999, Liz Ann joined U.S. Trust—which was acquired by Schwab in 2000—as a managing director and member of its Investment Policy Committee. Previously, Liz Ann was a managing director and senior portfolio manager at Avatar Associates, an original division of the Zweig/Avatar Group. She holds an MBA in Finance from the Gabelli School of Business at Fordham University and a B.A. in Economics and Political Science from the University of Delaware.

Kevin Gordon, Director, Senior Investment Strategist

Kevin Gordon serves as the research associate for Schwab's Chief Investment Strategist Liz Ann Sonders. In addition to providing analysis on the U.S. economy and stock market for Schwab's clients, he helps develop deep-dive projects as well as content for Schwab's public website, internal business partners, and social media outlets. Kevin is a frequent guest on CNBC, Yahoo! Finance, Bloomberg TV, and CBS News, and has been quoted in The New York Times, Forbes, MarketWatch, CNN, The Wall Street Journal, and Bloomberg.

Prior to joining Schwab in 2019, Kevin gained experience in asset allocation research at an investment advisory firm, and worked for a U.S. senator in Washington, D.C. He graduated magna cum laude from Pepperdine University, where he co-managed a student-run investment fund and co-authored academic publications on politics and the economy. Kevin is currently an MBA candidate at New York University's Stern School of Business. He holds a B.A. in Economics and Political Science from Pepperdine University.

Kevin is a member of the President’s Advisory Council for Almost Home Kids affiliated with Ann & Robert H. Lurie Children's Hospital of Chicago.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

Factors used in this report:

The Growth factor is based upon several historical (and forward-looking) growth rates of accounting variables and analyst-estimates. Stocks with high profitability growth, high expected dividend growth, and/or lower expected sales growth tend to have better Growth scores.

The Quality factor is built using various operating performance measures derived from financial statement data. Stocks with attributes such as high profitability, high earnings quality, conservative investment spending and/or better operating efficiency will likely have better Quality scores.

The Sentiment factor is calculated using measures of both long-term and short-term changes in investors' expectations. Stocks with recently improving analysts' outlooks, strong and consistent price performance, and/or optimistic trading positions and trends tend to score better within Sentiment.

The Stability factor is based on performance variability measures derived from both financial statements and trading data. Stocks with low sales volatility and low trading volume turnover tend to have better Stability scores.

The Value factor uses multiple value-oriented investment criteria. In general, stocks with attributes such as relatively high levels of free cash flow, operating income and expected future earnings tend to have better Valuation scores.

Sector definitions:

Communication Services sector: The Communication Services Sector includes telecom and media & entertainment companies including producers of interactive gaming products and companies engaged in content and information creation or distribution through proprietary platforms.

Consumer Discretionary sector: The Consumer Discretionary sector's manufacturing segment includes automobiles & components, household durable goods, leisure products and textiles & apparel. The services segment includes hotels, restaurants, and other leisure facilities. It also includes distributors and retailers of consumer discretionary products.

Consumer Staples sector: The Consumer Staples sector includes manufacturers and distributors of food, beverages and tobacco and producers of non-durable household goods and personal products. It also includes distributors and retailers of consumer staples products including food & drug retailing companies.

Energy sector: The Energy sector includes companies that operate in the areas of exploration & production, refining & marketing, and storage & transportation of oil & gas and coal & consumable fuels. It also includes companies that offer oil & gas equipment and services.

Financials sector: The Financials sector includes banking, financial services, consumer finance, capital markets and insurance activities. It also includes Financial Exchanges & Data and Mortgage REITs.

Health Care sector: The Health Care sector includes health care providers & services, health care equipment & supplies, and health care technology companies. It also includes companies involved in the research, development, production and marketing of pharmaceuticals and biotechnology products.

Industrials sector: The Industrials sector includes aerospace & defense, building products, electrical equipment and machinery and companies that offer construction & engineering services. It also includes providers of commercial & professional services including printing, environmental and facilities services, office services & supplies, security & alarm services, human resource & employment services, research & consulting services. It also includes companies that provide transportation services.

Information Technology sector: The Information Technology sector includes software and information technology services, manufacturers and distributors of technology hardware & equipment such as communications equipment, cellular phones, computers & peripherals, electronic equipment and related instruments, and semiconductors and related equipment & materials.

Materials sector: The Materials sector includes chemicals, construction materials, forest products, glass, paper and related packaging products, and metals, minerals and mining companies, including producers of steel.

Real Estate sector: The Real Estate sector includes companies engaged in real estate development and operation. It also includes companies offering real estate related services and Equity Real Estate Investment Trusts (REITs).

Utilities sector: The Utilities sector covers utility companies such as electric, gas and water utilities. It also includes independent power producers, energy traders and renewable sources.

Schwab Equity Ratings® and Schwab Equity Ratings International®, Schwab's proprietary stock research, are produced by the Schwab Center for Financial Research (SCFR). SCFR is a division of Charles Schwab & Co., Inc. (Schwab).

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

0424-X6TC

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All