Callable Bonds: Understanding How They Work

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCallable bonds make up a large share of the bond market—and introduce one more variable into the bond-investing process.

Callable bonds are a type of bond that can be redeemed by the issuer before the stated maturity date. There are different types of callable bonds, and different reasons why a bond might be "called" early by the issuer. It's important to understand the basics of callable bonds so you're not caught off guard if your bond investment is returned to you before the stated maturity date.

Traditional calls vs. make-whole calls

The two most common call features are traditional calls and make-whole calls.

Traditional calls:

There are three characteristics that investors should be aware of when considering bonds with traditional call features:

- Call protection. This is the amount of time before a bond can first be called. Call protection can vary considerably, with some bonds able to be called immediately after issuance, while other bonds might not be callable for many years. Most callable bonds tend have at least three months of call protection when they are issued, however.

- Call frequency. Once a bond becomes callable, how often the bond can be called varies as well. Some bonds may be callable monthly, quarterly, or semiannually, for example, or they may be "continuously callable," which would allow the issuer to call in the bond at any time once that first call date arrives.

- Call price. Bonds are usually callable at a specific price. Most agency and investment-grade corporate bonds are usually callable at their par price of $1,000. Many high-yield corporate bonds have some sort of call price schedule, where the call price starts at a high premium to its par value, and then declines each year thereafter.

Traditional call features generally work to the advantage of the issuer, not to the lender or investor. If interest rates fall, issuers would be more likely to "call in" a bond if they were able to refinance it with a new bond with a lower interest rate. Bonds without traditional call features are called "bullet" bonds.

Think of it like a homeowner—if mortgage rates fall, homeowners may refinance their mortgages to lock in a lower rate. It works the same way with many bond issuers, and call features allow them to take advantage of a drop in interest rates.

There are a number of types of bond issuers that issue bonds with traditional call options, including investment-grade corporate bonds and agency bonds, or bonds issued by government-sponsored enterprises like Fannie Mae or Freddie Mac. Many municipal bonds have call features, as well, but they have many unique call features that are beyond the scope of this article.

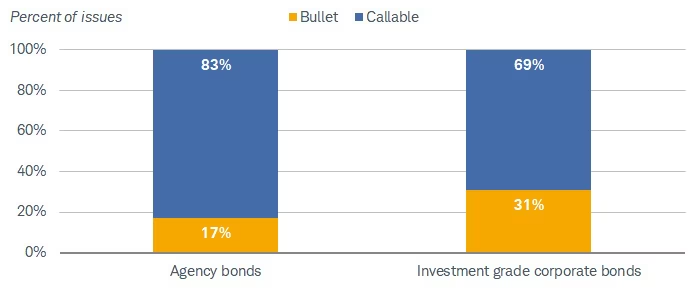

Callable bonds make up a large share of both the agency and corporate bond markets

Source: Bloomberg, as of 4/16/2024.

Chart uses the following criteria: Agency bonds include all outstanding agency bonds issued by the Federal National Mortgage Association (Fannie Mae), Federal Home Loan Mortgage Corporation (Freddie Mac), Federal Home Loan Bank (FHLB) and the Tennessee Valley Authority (TVA). Investment-grade corporate bonds include all US dollar-denominated corporate bonds with investment-grade ratings by Standard & Poor's and Moody's, respectively, and with $250 million or more outstanding. A bullet bond is a debt investment whose entire principal value is paid in one lump sum on its maturity date, rather than amortized over its lifetime. For illustrative purposes only.

There are disadvantages to the callable bond holder because the bond proceeds likely would be reinvested in lower-yielding options. Investors are generally rewarded with slightly higher yields relative to a noncallable bond to compensate for the risk of an early call; the amount of extra yield varies, however.

A call feature generally limits the upside of a bond's price in the secondary market, as well. Bond prices and yields move in opposite directions, so a drop in yields generally pulls up the price of bonds. But if a bond can be "called" at its $1,000 par value, it's unlikely to rise much above that $1,000 par value should interest rates fall.

Traditional callable bonds also have a yield measure known as the "yield to call", or the YTC. The yield-to-call is the annualized rate of return if the bond were to be called at its first or next call date, whereas the yield-to-maturity is the annualized rate of return if a bond is held to maturity. (The yield-to-worst is the lower of the two measures.)

If a bond is priced at a premium above its par value, it may have a lower yield-to-call than the yield-to-maturity and could be an indication that the bond might get called soon. When considering individual bonds, always pay attention to the various yield measures to get an idea of what your return could be, and more importantly, if the yield-to-call is lower than the yield-to-maturity.

Make-whole calls

A make-whole call is very different from a traditional call. Rather than being called at a predetermined price, like the bond's $1,000 par value, the call price for a make-whole call is based on market conditions and generally favors the bond investor. A make-whole call generally is based on the yield and price of bond in the secondary market (plus a premium), so if yields fall, the call price would rise. Make-whole call features are usually found in corporate bonds rather than municipal or agency bonds.

To understand make-whole calls, it's important to start with how corporate bonds are issued. The yield at which a given corporate bond is issued is related to a Treasury bond with a similar maturity, but the corporate bond will have a higher yield. That extra yield is called a "spread" and is meant to compensate investors for the additional risks of investing in a non-Treasury bond (Treasuries are considered "risk free" because they're backed by the full faith and credit of the U.S. government). For example, if a five-year Treasury bond offered a yield of 4%, a given corporate bond might offer a yield of 5%, or a spread of one percentage point.

The make-whole call price is usually dictated by the Treasury security that the corporate bond is referenced to, but with a premium. For example, if a company wanted to exercise the make-whole call, we'd first start with the price of the Treasury security in the secondary market, plus a specified premium amount as dictated in the bond's prospectus.

The "make-whole" descriptor comes from the idea that investors are generally made whole if the make-whole call is exercised because the minimum price for it to be called is $1,000.

If yields fall, however, investors would be rewarded with a premium price because bond prices and yields move in opposite directions. Unlike bonds with traditional calls whose prices might not rise much above par value, bonds with make-whole calls tend to act just like noncallable bonds if yields fall.

Make-whole calls are rarely exercised because it's usually cost-prohibitive to do so for the issuer. If yields fall and the issuer wants to refinance, it would need to pay a large premium to call in the bonds, potentially more than would be saved by issuing a lower-yielding bond. Make-whole calls are usually exercised if a company is going through an acquisition or is simply trying to reduce its debt, not because a drop in yields.

What to consider now

The presence of a call feature isn't necessarily an advantage or disadvantage in a vacuum. Here are a few key considerations for callable bonds:

- For investors who use bond ladders to hold individual bonds, we suggest holding bullet bonds or bonds that have make-whole call features rather than bonds with traditional call features. A bond ladder is a good way to spread out interest rate risk and spread out maturities, which can be a good planning tool. Holding callable bonds in a bond ladder would throw a wrench in both of those plans if interest rates fall.

- For bonds with traditional call features, understand how an early call might impact your long-term investing plan. Investors looking to lock in a specific yield for a specific period of time might want to consider a noncallable bond so they don't risk an early return of their investment and the likelihood of reinvesting at lower yields. Likewise, investors shouldn't expect a callable bond to be called at its first call date. In other words, if you have a shorter-term investing horizon, pay more attention to the maturity date rather than the call date.

- Pay attention to the call protection of bonds with traditional call features. A bond with just six months of call protection is very different from a bond with nine years of call protection. Lately many corporate bonds have been issued with very long calls—like just six or 12 months before the scheduled maturity date. For example, a corporation might issue a 10-year bond, with a first call in nine years. Companies generally do this for flexibility. For bond investors, long calls don't throw much of a wrench in the investment planning process because near-term fluctuations in interest rates don't matter much. If an issuer issues a 10-year bond that's not callable for nine years, a drop in yields after the bond is issued doesn't matter much because the issuer can't redeem it for a long time. As a result, bonds with lots of call protection can still see price appreciation in the secondary market should interest rates fall.

- Make-whole calls rarely occur and generally work in the investor's favor. Bonds with a make-whole call (but not a traditional call) tend to act like noncallable bonds, so they generally don't provide the same disadvantages to investors as traditional callable bonds. While falling yields is a risk for bonds with traditional call features, that's generally not the case with make-whole call features.

Investing in individual bonds can often be a time-consuming and confusing process, and callable bonds add an extra layer of complexity to the investing process.

Make sure you understand the ins and outs of a call feature of a given bond, as not all callable bonds will behave the same way and not all callable bonds are necessarily at risk of an early call should interest rates fall.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and the Schwab Center for Financial Research does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. As compared to other fixed income products and strategies, engaging in a bond ladder strategy may potentially result in future reinvestment at lower interest rates and may necessitate higher minimum investments to maintain cost-effectiveness. Evaluate whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

0424-XR2N

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All