Loan Me a Dime

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPut on your wonky hats for this one. The second quarter Senior Loan Officer Opinion Survey (SLOOS) was released by the Federal Reserve last week. It addressed changes in the standards and terms on—and demand for—bank loans to businesses and households over the prior three months (generally corresponding to the first quarter of 2024). The top-line takeaway is that more than a year after the "mini" banking crisis—during which three of the four largest U.S. banks failed—there's been an easing in the percentage of banks tightening lending standards.

Survey respondents generally reported tighter standards and weaker demand for commercial and industrial (C&I) loans, as well as commercial real estate (CRE) loans to companies of all sizes. For loans to households, banks reported that lending standards tightened across some categories of residential real estate (RRE) loans, while remaining unchanged for others on balance. Not surprising was a weakening in demand for all RRE loan categories as well as for home equity lines of credit (HELOCs). Tighter standards and weaker demand were also evident for credit card, auto and other consumer loans.

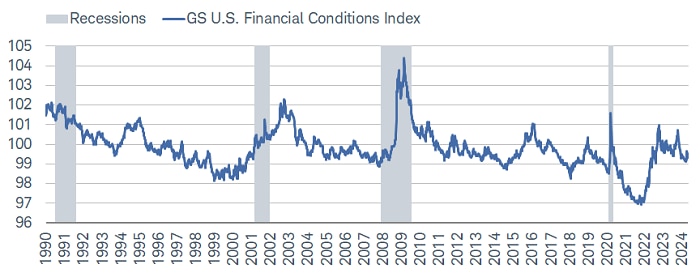

What's notable about the recent period of tight lending standards was the absence of a recession. In addition, since late 2022, the tightening has been largely driven by Treasury yields and bank credit, rather than risk assets like credit spreads or equity market volatility (VIX). This adds color to why the Fed continues to view monetary policy as remaining fairly restrictive, even though market-based financial conditions measures, like the index shown below, suggest looser conditions.

Easing in financial conditions

Source: Charles Schwab, Bloomberg, as of 5/10/2024.

The GS (Goldman Sachs) U.S. Financial Conditions Index is defined as a weighted average of riskless interest rates, the exchange rate, equity valuations, and credit spreads, with weights that correspond to the direct impact of each variable on GDP.

It's an important distinction to make, especially since there has been some confusion among investors, analysts, and strategists lately as to why members of the Federal Open Market Committee (FOMC)—and notably, Chair Jerome Powell himself—have continued to claim that conditions are tight when measures of financial conditions have seemingly eased (or loosened).

Key to keep in mind is that Fed officials are not solely looking at asset prices to determine the level of restrictiveness in the real economy. Instead, they have focused (and still focus) on the fact that bank lending has slowed considerably, the housing market has weakened over the past couple years, and labor demand has come down swiftly, among other things. As such, there are times during which market-based financial conditions indexes (like the one shown above) can tell a different story from what real economy metrics say. The Fed is not targeting asset prices, though, which means that an improving stock market (and/or falling bond yields) in and of itself does not put rate cuts on hold (and vice-versa).

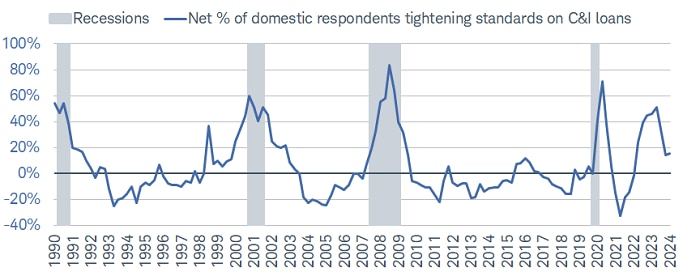

C&I trends

Of the banks that reported having tightened standards or terms on C&I loans, a significant share cited a less favorable or more uncertain economic outlook, a reduced tolerance for risk, and a worsening of industry-specific problems as important reasons for doing so.

Supply-side for C&I loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

C&I (commercial and industrial) data covers large and middle-market firms defined as firms with annual sales of $50 million or more.

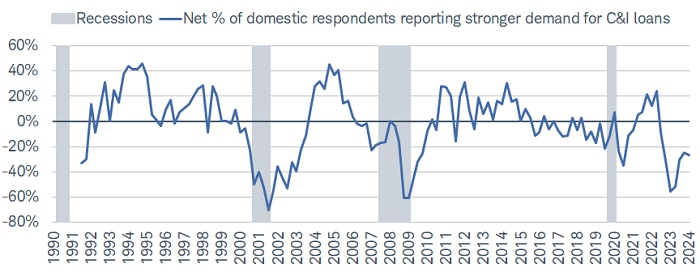

Of the banks reporting weaker demand for C&I loans, among the most cited reasons for weakening demand, a significant share reported: decreased customer financing needs for merger or acquisition and inventory, as well as decreased customer investment in plants or equipment.

Demand-side for C&I loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

C&I (commercial and industrial) data covers large and middle-market firms defined as firms with annual sales of $50 million or more.

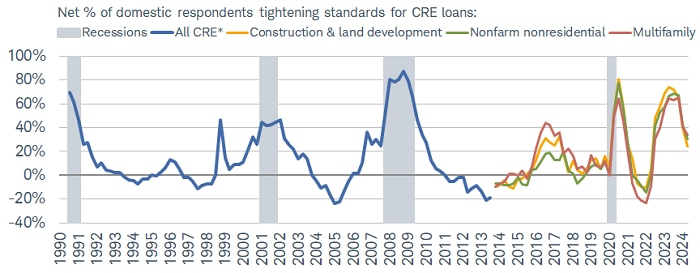

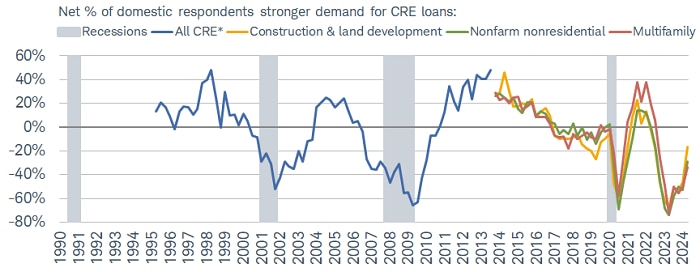

CRE trends

The most-cited reasons for tightening credit policies on CRE loans over the past year, cited by nearly all banks, were less favorable or more uncertain outlooks for CRE market rents, vacancy rates, and property prices. Additionally, a major share of banks cited a reduced tolerance for risk, increased concerns about the effects of regulatory changes or supervisory actions, and a less favorable/more uncertain outlook for delinquency rates on mortgages backed by CRE properties.

Supply-side for CRE loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

CRE=commercial real estate. *Data discontinued 3Q2013.

In terms of reasons for still-weak demand, the most cited included the increase in the general level of interest rates, a decrease in customer acquisition or development of properties, and a more uncertain/less favorable customer outlook for rental demand. Of the smaller (but sizable) share of banks reporting stronger demand, reasons included an increase in customer acquisition or development of properties, a shift in customer borrowing to respondent banks from other banks/non-bank sources, and a decrease in internally generated funds by customers.

Demand-side for CRE loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

CRE=commercial real estate. *Data discontinued 3Q2013.

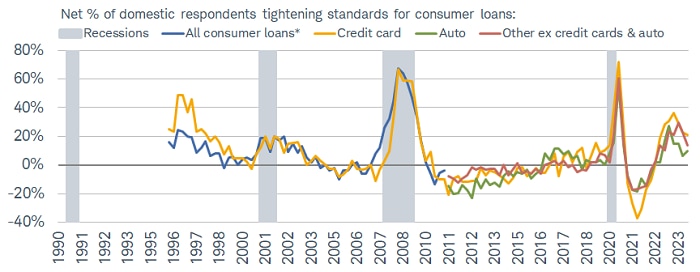

Consumer trends

A significant net share of banks reported tightening standards for credit card loans, while a more modest net share reported tighter conditions for other consumer and auto loans, respectively. A large net share of banks also reported increasing minimum credit-score requirements for credit card loans, while a moderate (compared to this time last year) net share of banks reported doing so for auto and other consumer loans.

Supply-side for consumer loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

*Data discontinued 1Q2011.

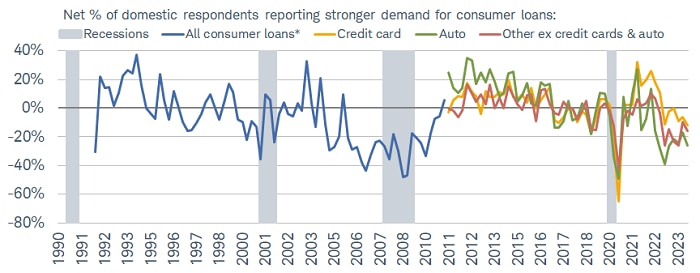

Regarding demand for consumer loans, a significant net share of banks reported weaker demand for auto loans, with a more moderate net share reporting weaker demand for credit card and other consumer loans.

Demand-side for consumer loans

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

*Data discontinued 1Q2011.

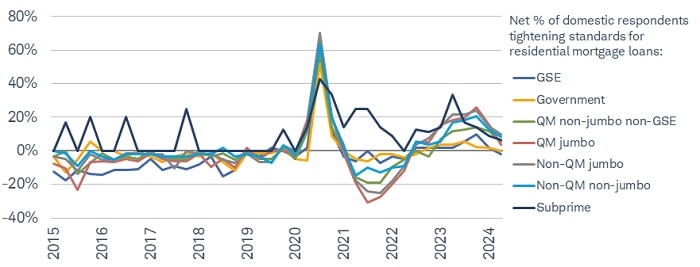

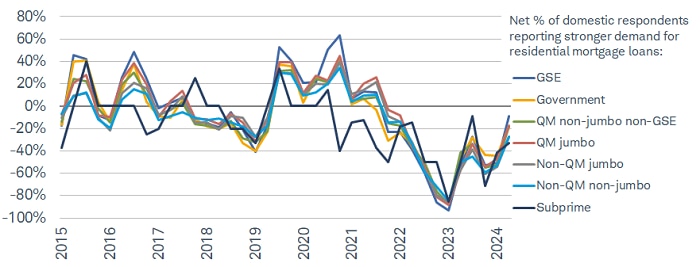

Mortgage trends

Per the charts below, the SLOOS only started breaking out mortgages into the current seven categories in 2015, hence the shorter time frame. A modest net share of banks reported tightening standards for non-qualified mortgage (QM) jumbo, non-QM non-jumbo, subprime, and QM non-jumbo non-government-sponsored enterprise (GSE)-eligible mortgage loans. Lending standards were essentially unchanged for GSE-eligible, government, and QM jumbo mortgages.

Supply-side for mortgages

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

GSE=government sponsored enterprise. QM=qualified mortgage.

On the demand side, banks reported net weaker demand, on balance, for all RRE loans and HELOCs; however, demand is well up from the lows during 2023.

Demand-side for mortgages

Source: Charles Schwab, Bloomberg, Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices, as of 2Q2024.

GSE=government sponsored enterprise. QM=qualified mortgage.

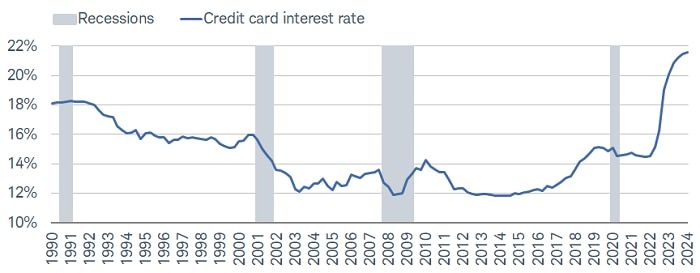

Credit card story

Credit cards continue to show the most significant tightening on the consumer side; perhaps not surprising in light of the surge in credit card interest rates, shown below.

Credit card rates on fire

Source: Charles Schwab, Bloomberg, Federal Reserve, as of 1Q2024.

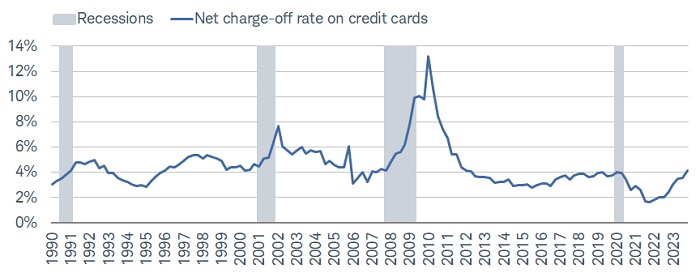

Also not surprising has been the acceleration in net charge-offs on credit cards, shown below. The relative tightening is unsurprising given the credit score migrations and credit extensions provided during the pandemic period, when rising incomes and stimulus boosted household income. We're arguably now in the payback period.

Credit card charge-offs accelerating

Source: Charles Schwab, Bloomberg, as of 4Q2023.

Net charge-off rate tracks credit cards that are in default or close to being in default.

In sum

The U.S. economy remains relatively strong; with surprising resilience in the face of the Fed's most aggressive tightening cycle in more than 40 years. Of all lending categories, the CRE sector has been most beleaguered for obvious pandemic-related reasons. In general, both the supply and demand sides of bank loans to corporations and households/consumers has become less tight—particularly relative to the peak tightness that occurred around the mini banking crisis last year. With loan supply (and cost) remaining somewhat restricted, any resultant slower economic growth could help turn the light for Fed rate cuts from yellow to green.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

0524-29Z8

A message from Advisor Perspectives and VettaFi: Dive into alternative investment opportunities at our upcoming Alternatives Symposium on May 30th, and gain insights into diversifying portfolios beyond traditional equities and fixed income.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All