Just a Job to Do: Assessing the Labor Market

Membership required

Membership is now required to use this feature. To learn more:

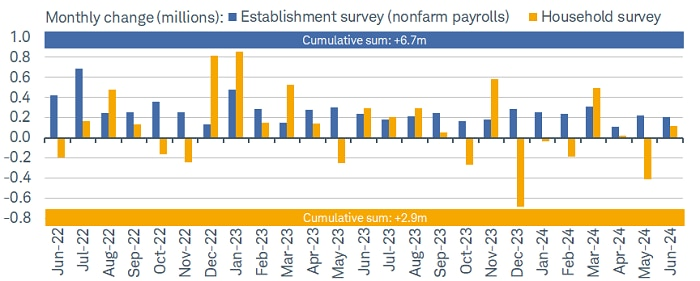

View Membership BenefitsOn a day when many were still enjoying the revelry of the Fourth of July holiday, the Bureau of Labor Statistics (BLS) released the June jobs report. In keeping with recent releases, it provided a mixed-to-weakening picture of the labor market. The BLS' establishment survey showed payroll growth of 206K relative to the 190K that was expected; however, downward revisions to the prior two months were a hefty 111K. The BLS' household survey—from which the unemployment rate is calculated—did show a gain in jobs to the tune of 116K, which is an improvement from May's decline of 408K. Yet, as shown below, there continues to be a yawning 3.8 million gap between the establishment and household surveys' tally of job growth over the past two years.

Household still lags establishment

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

The establishment survey tends to overstate job growth during economic slowdowns, in part due to overly optimistic estimates of new business births. In addition, the annual benchmark revisions coming in the first quarter of 2025 will likely bring downward revisions to the prior year's payrolls of an estimated 70-80K per month. This is based on what can be gleaned from the latest quarterly census survey. It's also the case that household employment may be understated in part due to immigrations' impact. Combined, it leads to our conclusion that the real employment story may be somewhere in between the two BLS surveys' findings.

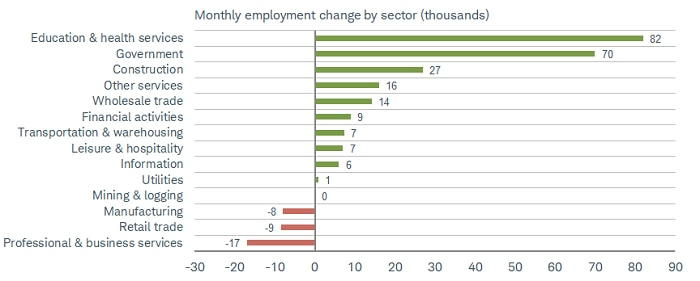

Payroll gains were concentrated in education/health services and government, while losses were concentrated in professional and business services, as shown below. The gains in non-education state and local government seem to contradict anecdotal evidence of many states' increasing budget shortfalls and spending restraint. Leaning weaker: a significant decline of nearly 49K in temporary help employment, a 28K drop in full-time employment, and a 50K jump in part-time employment.

Concentrated payroll gains

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

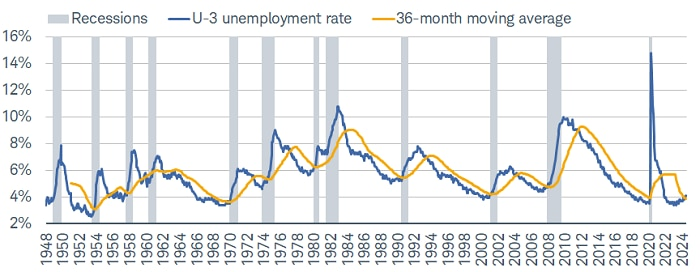

There was yet another tick higher in the unemployment rate to 4.1%. As shown below, it is up from this cycle's low of 3.4%, while it's also continued to climb above the 36-month moving average. As you can see, every time that cross has occurred historically, it's been a clear recession indicator. That said, this cycle has bucked so many historical trends with regard to recession signals, so the jury remains out on this one. Worth watching is also long-term unemployment (defined as more than 27 weeks), which continues its trek higher. At 22.2% of total unemployment, it's a new post-pandemic cycle high.

Unemployment drifting higher

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

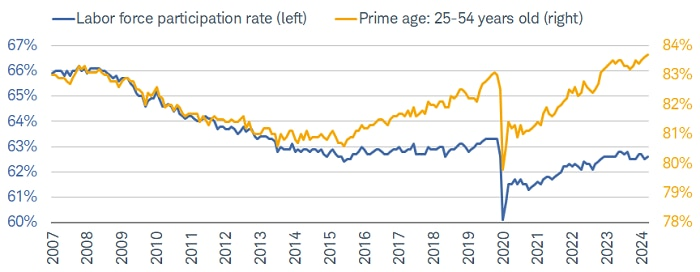

The labor force participation rate (LFPR) ticked up slightly, with a larger gain for prime-age, as shown below. In particular, the LFPR for women continues to enjoy a stronger rebound in this cycle relative to the LFPR for men. The aforementioned tick higher in the unemployment rate was for a "good" reason in that it reflects higher labor force participation, not a decrease in employment.

Participation still expanding

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

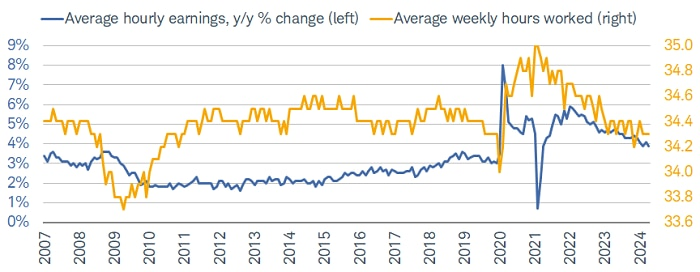

Average hourly earnings (AHE) ticked down to 3.9% year-over-year, which was in line with the consensus estimate and down from May's 4.1% reading. On the margin, this is good news from the perspective of inflation and Federal Reserve policy; but AHE growth remains well above the 2.5%-3.0% pre-pandemic range.

Earnings growth easing

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

Normalization or something worse?

The dominant question with all things labor data is whether the recent soft patch is indicative of a continued normalization from pandemic distortions, or something more sinister (and indicative of a recession). One way to see confirmation that we are experiencing the former is via the monthly job openings data that come from the Job Opening and Labor Turnover Survey (JOLTS).

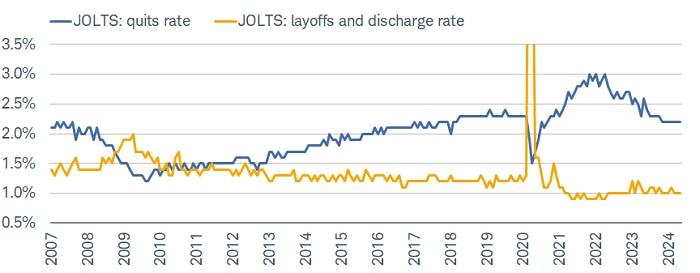

As shown in the chart below, when the labor market was experiencing a strong recovery as the global economy was reopening, the quits rate—which measures workers' confidence in leaving their job and easily finding a new one—soared to an all-time high, underscoring immense labor tightness. It has since come down to pre-pandemic levels; and given the layoffs and discharge rate hasn't surged, it supports the notion that the market is normalizing. A continued convergence between both series would be more worrisome, however.

Quits down, layoffs subdued

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, JOLTS (Job Openings and Labor Turnover Survey), as of 5/31/2024.

Y-axis is truncated for visual purposes.

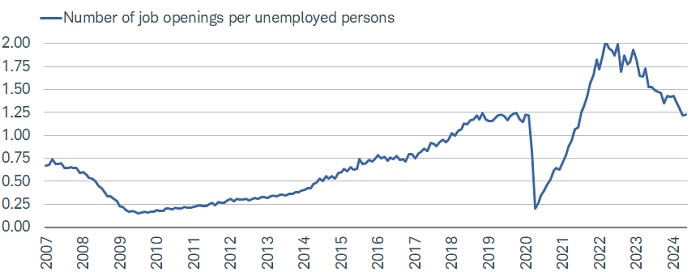

Corroborating the normalization story is the roundtrip done by the ratio of job openings per unemployed individuals. As shown in the chart below, the ratio climbed rapidly in 2021 and 2022 (again, to an all-time high) as companies' demand for labor soared, helping put immense upward pressure on wages and inflation—thus pushing the Fed to aggressively raise rates. We've previously discussed that this indicator arguably overstates the tightness in the labor market, but given it remains a favorite among Fed officials, we think it's important to monitor.

Labor tightness fading

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as 5/31/2024.

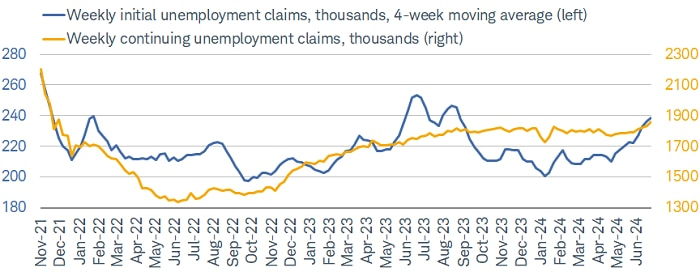

The unfortunate aspect of the JOLTS data is the lagged nature of it (for example, we won't get June job openings data for another month). As such, we think one of the best leading labor market indicators to watch is jobless claims—both initial and continuing. As shown in the chart below, claims have been moving higher this year, with the pace really picking up in May. Worth noting is that the current trend is consistent with what we saw in 2023, 2019, and 2018; so, the uptick isn't yet a surefire recession signal.

That said, though, continuing jobless claims—which measure the number of individuals continuing to file for unemployment benefits—have risen to their highest since November 2021. This likely underscores the reduction in firms' demand for labor and subsequent difficulty individuals are having in finding other jobs; the so-called "rehiring rate" is moving lower.

Claims trending higher

Source: Charles Schwab, Bloomberg. Initial claims as of 6/28/2024.

Continuing claims as of 6/21/2024.

Fed reaction function

We've been of the view that labor market trends have become at least as important as inflation trends in guiding the Fed in terms of when to start easing monetary policy. There was an interesting knee-jerk reaction in the fed funds futures market immediately after the jobs report release: Given better-than-expected payrolls, expectations for a start to rate cuts at the September Federal Open Market Committee (FOMC) meeting actually moved lower relative to before the release of the jobs report. However, after the details of the report were assessed, expectations jumped higher and as of this writing, are up to about a 72% probability per the CME Fed Watch Tool.

The net is that the Fed is likely to remain "patient" (their new favorite descriptor) for now; but any further weakening in the labor market could provide the green light for the Fed to begin easing policy in advance of inflation hitting their 2% target.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

0724-BY2X

About the Authors

Liz Ann Sonders, Managing Director, Chief Investment Strategist

Liz Ann Sonders has a range of investment strategy responsibilities, from market and economic analysis to investor education, all focused on the individual investor.

A keynote speaker at numerous company and industry conferences, Liz Ann is regularly quoted in financial publications including The Wall Street Journal, The New York Times, Barron's, and the Financial Times, and she appears as a regular guest on CNBC, Bloomberg, CNN, CBS News, Yahoo! Finance, and Fox Business News programs. Liz Ann has been named "Best Market Strategist" by Kiplinger's Personal Finance and one of SmartMoney magazine's "Power 30." Barron's has named her to its "100 Most Influential Women in Finance" every year since the list's inception, and Investment Advisor has included her on the "IA 25," its list of the 25 most important people in and around the financial advisory profession. Liz Ann has also been named to Forbes' 50 Over 50.

In 1999, Liz Ann joined U.S. Trust—which was acquired by Schwab in 2000—as a managing director and member of its Investment Policy Committee. Previously, Liz Ann was a managing director and senior portfolio manager at Avatar Associates, an original division of the Zweig/Avatar Group. She holds an MBA in Finance from the Gabelli School of Business at Fordham University and a B.A. in Economics and Political Science from the University of Delaware.

Kevin Gordon, Director, Senior Investment Strategist

Kevin Gordon serves as the research associate for Schwab's Chief Investment Strategist Liz Ann Sonders. In addition to providing analysis on the U.S. economy and stock market for Schwab's clients, he helps develop deep-dive projects as well as content for Schwab's public website, internal business partners, and social media outlets. Kevin is a frequent guest on CNBC, Yahoo! Finance, Bloomberg TV, and CBS News, and has been quoted in The New York Times, Forbes, MarketWatch, CNN, The Wall Street Journal, and Bloomberg.

Prior to joining Schwab in 2019, Kevin gained experience in asset allocation research at an investment advisory firm, and worked for a U.S. senator in Washington, D.C. He graduated magna cum laude from Pepperdine University, where he co-managed a student-run investment fund and co-authored academic publications on politics and the economy. Kevin is currently an MBA candidate at New York University's Stern School of Business. He holds a B.A. in Economics and Political Science from Pepperdine University.

Kevin is a member of the President’s Advisory Council for Almost Home Kids affiliated with Ann & Robert H. Lurie Children's Hospital of Chicago.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All