U.S. Agency Bonds: What You Should Know

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsU.S. agency bonds are a type of highly rated bond investment that may help investors earn slightly higher yields than U.S. Treasury bonds without taking on too much additional risk. We continue to suggest investors focus on high-quality investments today, and agencies fall under that guidance.

Agency bonds are issued by government-sponsored enterprises (GSEs). Some of the most common issuers of agency bonds include, but are not limited to, the following:

- Federal National Mortgage Association, or Fannie Mae (FNMA)

- Federal Home Loan Mortgage Corporation, or Freddie Mac (FHLMC)

- Federal Home Loan Bank (FHLB)

- Federal Farm Credit Bank (FFCB)

- Tennessee Valley Authority (TVA)1

For this article, we are focusing solely on bonds issued by the agencies, and not mortgage-backed securities. Fannie Mae, Freddie Mac, and the Government National Mortgage Association, or Ginnie Mae (not mentioned in this article), issue and back mortgage-backed securities, but those are different from the traditional bonds discussed in this article.

Government-sponsored enterprises do not have the explicit backing of the U.S. government. Although GSEs are considered to have the implicit backing of the government, they are not backed by the full faith and credit of the U.S. government. Because agency bonds have more credit risk (that is, the risk that they will fail to make timely interest payments or even, in a worst-case scenario, fail to repay principal) than Treasuries, they would generally have a greater risk of default should one of the issuers face financial hardship.

The idea of a U.S. default tends to come up when a debt ceiling debate arises, but that shouldn’t necessarily have an impact on agency bonds. They are not considered direct obligations of the U.S. government, as the agencies and GSEs that issue them are generally self-funded. However, should one of the agencies need U.S. assistance while the U.S. were in default—which we don't believe is likely—then that could pose a risk to agency bond investors, as the government would not likely be able to help in a timely manner.

Given that implicit backing, agency bonds generally carry the same credit ratings as the U.S. government, which is currently rated Aaa/AA+/AA+ by Moody's Investors Service, Standard & Poor's, and Fitch Ratings, respectively.2 If one or more of the rating agencies downgraded the rating of the U.S. government as a result of the political wrangling around the debt ceiling, that would likely result in a downgrade of the agencies, as well.

Agency bonds have continued to make timely interest and principal payments despite a number of concerns over the years. Fannie Mae and Freddie Mac, for example, were placed under conservatorship by the U.S. government back in 2008. Both GSEs are public companies, and the conservatorship means that the Federal Housing Finance Agency (its regulator) "has the powers of the management, boards, and shareholders of Fannie Mae and Freddie Mac. Fannie Mae and Freddie Mac continue to operate as business corporations."3

Here are a handful of things to know before considering agency bonds.

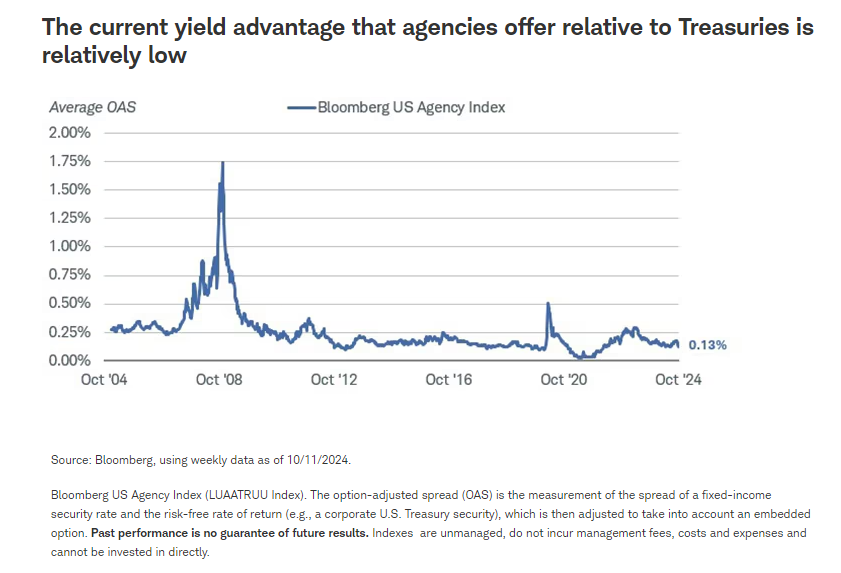

1. The current yield advantage over Treasuries is relatively low

Because agencies aren't explicitly backed by the U.S. government, they tend to offer a yield advantage over U.S. Treasuries. That extra yield is called a "spread" and fluctuates based on market conditions.

Spreads rose sharply during the 2008-2009 financial crisis, especially as Fannie Mae and Freddie Mac were placed into conservatorship. While the agencies have continued to make on-time principal and interest payments, that wasn't known back in 2008 and investors understandably got nervous, sending spreads up to 1.75%, on average. Spreads rose again in March 2020, albeit not by the same magnitude of the financial crisis surge, but fell quickly given the swift government intervention.

The Bloomberg US Agency Index has an average spread of just 13 basis points, or 0.13%, meaning investors aren't earning much additional yield over Treasuries relative to history. The chart below highlights that the average spread of the index has generally hovered near 25 basis points or less since the end of the financial crisis.

Low spreads don’t mean investors should ignore agencies, however. It just might make more sense to focus on specific maturities where there is a more attractive yield advantage, as we discuss next.

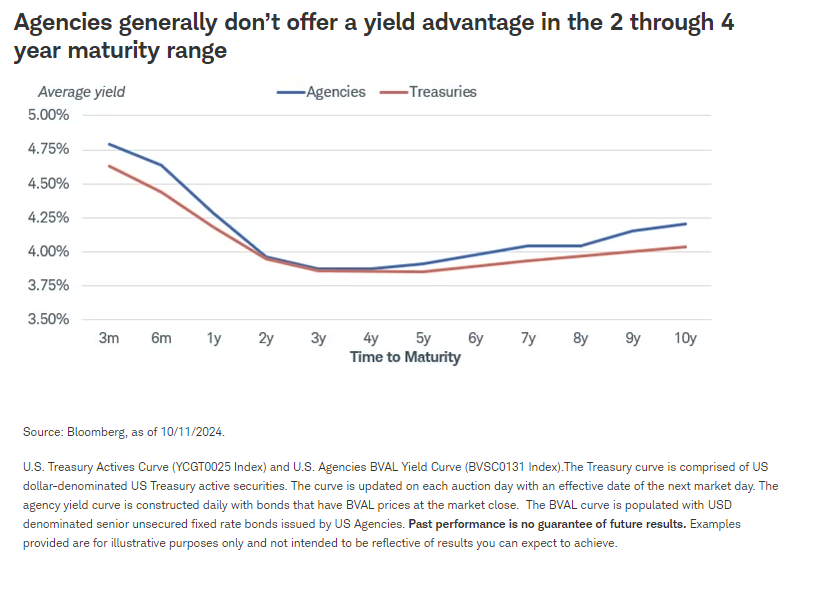

2. The relative attractiveness of agency bonds varies based on maturity

Agencies tend to offer higher yields than Treasuries for very short-term maturities, like one year or less, or for longer-term maturities like five years or more. On average, there isn’t a yield advantage at all for maturities of two through four years, as the yield curve chart below illustrates.

Keep in mind that the agency yields shown below are averages. There are a lot of different agency issuers and they may each have maturities around the same date—in other words, there isn't necessarily a "benchmark" two- or five-year agency note. On average, though, there doesn't appear to be much value with agencies of maturities of two through four years as of October 11, 2024, but that yield advantage (or lack thereof) can change over time.

For investors considering very short-term investments, take a look at what various alternatives offer. The yields on certificates of deposit (CDs), Treasuries, and agencies are all pretty similar for maturities of two years or less, and what offers a higher yield one day might offer a lower yield the next. Although agencies are government-sponsored enterprises, they are not backed by the full faith and credit of the U.S. government. CDs are issued by banks but are backed by FDIC insurance (up to a limit, of course) and are therefore considered to be of high quality.4

3. "Callable" agencies generally offer higher yields but come with call risk

A bond with a call feature allows the issuer to "call" it, or redeem it, before the stated maturity date. The call date and price are generally known in advance but can vary.

Issuers often include call features for flexibility. If yields fall after the bond was issued, this may allow the issuer to issue a new, lower-yielding bond and use those proceeds to "call" the higher-yielding bond.

Investors generally face reinvestment risk if their callable bond gets called, as they'll likely need to invest those funds into a lower-yielding bond. Callable agency bonds tend to be issued with slightly higher yields than noncallable bonds to compensate for call and reinvestment risk.

Callable agencies tend to be issued in smaller deal sizes than noncallable agencies, usually resulting in less liquidity. That may be a risk if an investor needs to sell a callable agency before maturity, as there might not be as many potential buyers than a larger, noncallable bond may have.

There can be advantages with callable bonds, like the higher yields they tend to offer. If yields don't fall after investing, you may end up earning a higher yield than you may have otherwise earned if you invested in a noncallable bond. Also, even if a bond gets called early due to a drop in rates, the yield earned over that time period may be higher than what was available for other investments with that same short-term time horizon.

When considering callable bonds, be prepared for any outcome. In other words, there's a possibility that it gets called and you'll then need to replace that called bond with a new investment. Just as important is to be prepared to hold the callable bond to maturity, because it's not known in advance if or when the issuer may call it.

4. Consider taxes

There may be tax benefits of investing in some—but not all—agency bonds. The income from agency bonds is subject to federal income taxes when held in taxable accounts, but income from some of the agencies is exempt from state and local income taxes:

- Not exempt from state and local income taxes: Fannie Mae and Freddie Mac

- Exempt from state and local income taxes: FHLB, FFCB, and TVA

Keep in mind that interest from U.S. Treasuries is exempt from state and local taxes, so when considering agencies relative to Treasuries, a U.S. Treasury may offer a higher after-tax yield depending on the agency issue and state and local tax rates. As always, we suggest investors consult with a tax specialist when considering the tax consequences of a given investment.

What to consider now

U.S. agency bonds can be considered by investors looking to earn slightly higher yields without taking too much additional credit risk. While agencies are government-sponsored enterprises, they are not backed by the full faith and credit of the U.S. government.

Callable agencies may make sense for investors looking for even higher yields, but investors should always be cognizant of the risk of a call before maturity, likely resulting in reinvestment risk. Likewise, investors shouldn't assume that an issue will be called at its first call date—always consider the maturity date of a callable issue and be prepared to hold it for the entirety of its maturity.

Finally, consider the tax consequences of agency bonds, as some may be more attractive than others on an after-tax basis, especially for investors in high-tax states.

1 The Tennessee Valley Authority is a federal agency, not a government sponsored enterprise. However, their debt securities are not considered obligations of the U.S. government and do not carry a government guarantee. Source: Tennessee Valley Authority.

2 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

3 Source: Federal Housing Finance Agency, "History of Fannie Mae and Freddie Mac Conservatorships," October 17, 2022.

4 The Federal Deposit Insurance Corporation (FDIC) is an independent agency that maintains the Deposit Insurance Fund, which is backed by the full faith and credit of the United States government. Its purpose is to protect depositors' funds placed in banks and savings associations. The FDIC insures accounts held at member banks up to $250,000 per depositor, per insured bank, based on ownership category. However, all deposits held at the same FDIC-insured bank in the same ownership capacity are added together to determine the depositor's total amount of FDIC insurance coverage at that bank.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Bloomberg US Agency Index includes US dollar-denominated, fixed-rate, debentures (securities issued by US government owned or government sponsored entities, and debt explicitly guaranteed by the US government). The US Agency Index is a component of the US Government and US Aggregate Indices, and eligible securities also contribute to the multi-currency Global Aggregate Index. The US Agency Index has an inception date of January 1, 1976.

1024-04KJ

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All