As the US economy veered toward the biggest inflation shock in four decades, investors flocked to the one corner of Wall Street that seemed a sure-fire refuge: Treasuries that provide extra compensation to keep up with rising consumer prices.

Ahead of this week’s Federal Reserve meeting — and in a year when many didn’t make the right calls — professional investors and do-it-yourselfers are sharply divided over the best way to position ahead of the central bank’s rate decision on Dec. 14.

Mixed news on US inflation reinforced the precariousness of the bond market’s recent gains ahead of next week’s consumer prices gauge and the Federal Reserve’s last rate decision of the year.

Slowly but surely, bond haters are vanishing across Wall Street — even as fresh market havoc remains a distinct possibility next year if still-raging inflation forces the Federal Reserve to ramp up policy tightening anew.

Wall Street is finding a reason to keep plowing into the bond market, even with a Federal Reserve that’s still far from declaring victory in its war against inflation.

All bets appear to be off on how high yields can rise in the world’s biggest bond market.

Wall Street money managers looking to pile back into Treasuries after months of losses will have to contend with a Federal Reserve that stands ready to raise the stakes every step of the way.

The optimism that has crept into the US bond market is about to be put to the test.

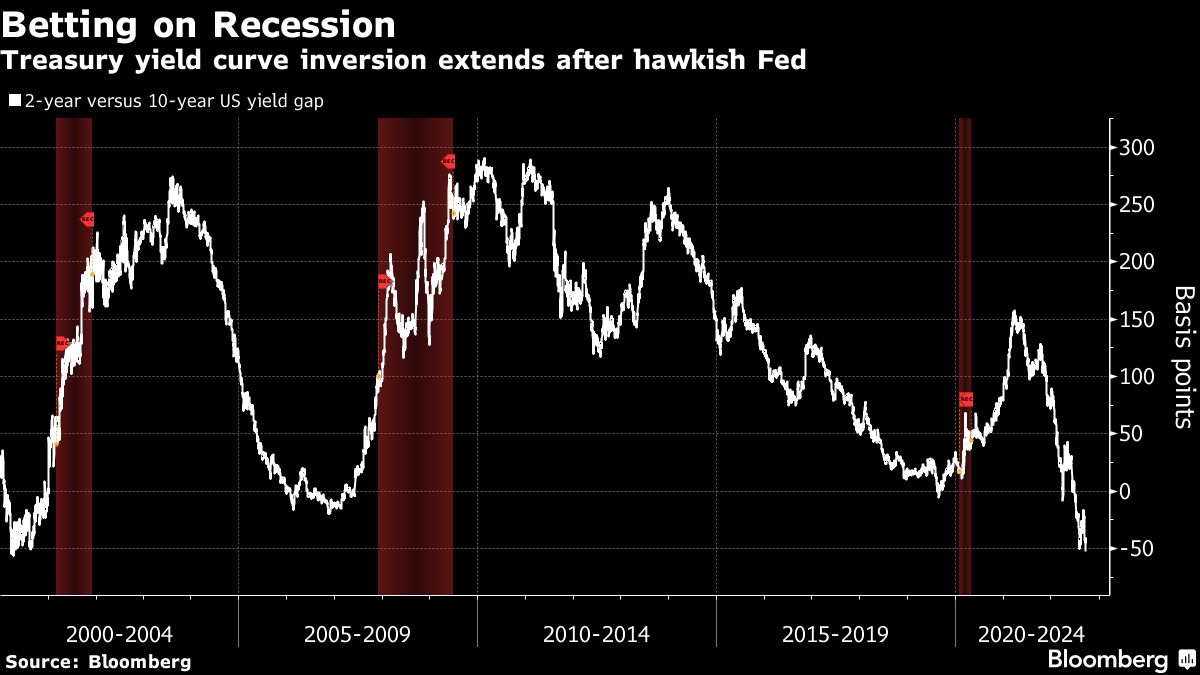

A classic recession warning is flashing in the US Treasury market, where the 10-year note’s yield fell below the three-month bill’s, a rare occurrence that signals investors anticipate dire economic consequences of the Federal Reserve’s campaign against inflation.

The Treasury market was upended Friday by a surge in wagers that circumstances will allow Federal Reserve to slow its pace of rate increases as early as year-end.

Everywhere you turn, the biggest players in the $23.7 trillion US Treasuries market are in retreat.

Week by week, the bond-market crash just keeps getting worse and there’s no clear end in sight.

Bond traders are girding for the risk that Federal Reserve Chair Jerome Powell is ready, willing and able to plunge the US into recession to get the inflation bogey under control.

The 10-year Treasury yield briefly rose above 3.50% for the first time since 2011 on Monday, with the bond market extending its bearish run ahead of another jumbo rate hike expected this week by the Federal Reserve to bring down inflation.

The specter of US interest rates at 4% or even higher is bringing into sharper focus the question of when and how investors should really get back into bonds after Treasury markets suffered one of their worst beatings in decades.

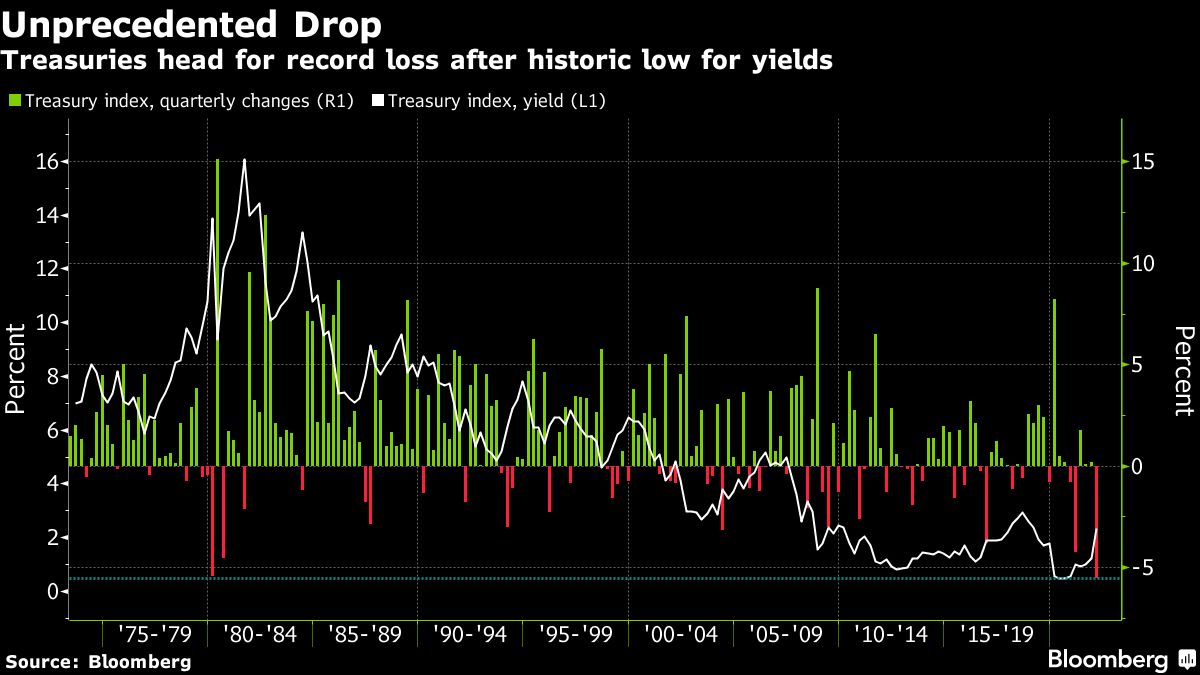

Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

Treasury yields surged on stronger-than-expected US employment data that shore up the case for additional hefty central bank interest-rate increases.

For all the volatility whipsawing the US bond market, traders are showing increasing confidence that the alarm bells warning of a recession will only get louder.

Treasuries began the second half of the year on the front foot Friday as concerns continued to mount that Federal Reserve rate hikes will lead to a recession.

It’s too soon to call an end to America’s worst bond-market collapse in at least half a century.

A wild year on Wall Street has traders fretting one of two extreme scenarios will engulf the $23 trillion Treasury market ahead: Either a fresh bond selloff thanks to red-hot inflation -- or a sustained rally on mounting recession risk that sends yields back toward historic lows.

Treasuries extended their slump in New York, driving the yield on the benchmark 10-year note up by the most in more than three weeks, as renewed inflation concerns and economic data supported expectations for multiple Federal Reserve rate hikes in coming months.

While all Treasury yields have climbed this year as the Fed began what’s expected to be an aggressive series of rate increases aimed throttling high inflation, in the past two weeks the baton has been passed to inflation-protected notes and bonds. Their yields are termed “real” because they represent the rates investors will accept as long as they are paired with extra payments to offset inflation.

The U.S. bond market reeled further on Tuesday, extending Monday’s declines after Federal Reserve Chair Jerome Powell’s aggressive rate hike comments drove yields on short-dated Treasuries to one of their biggest daily jumps of the past decade.

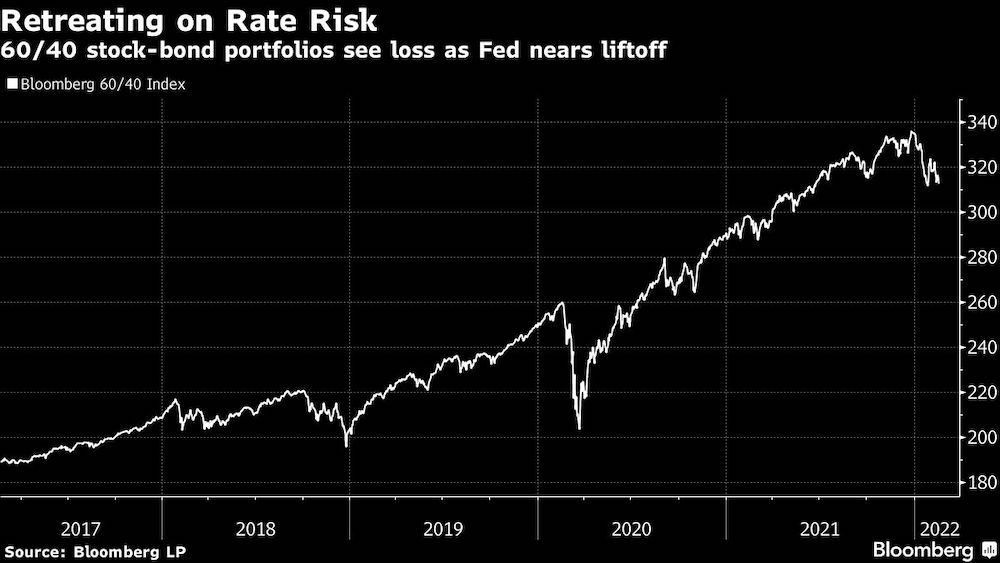

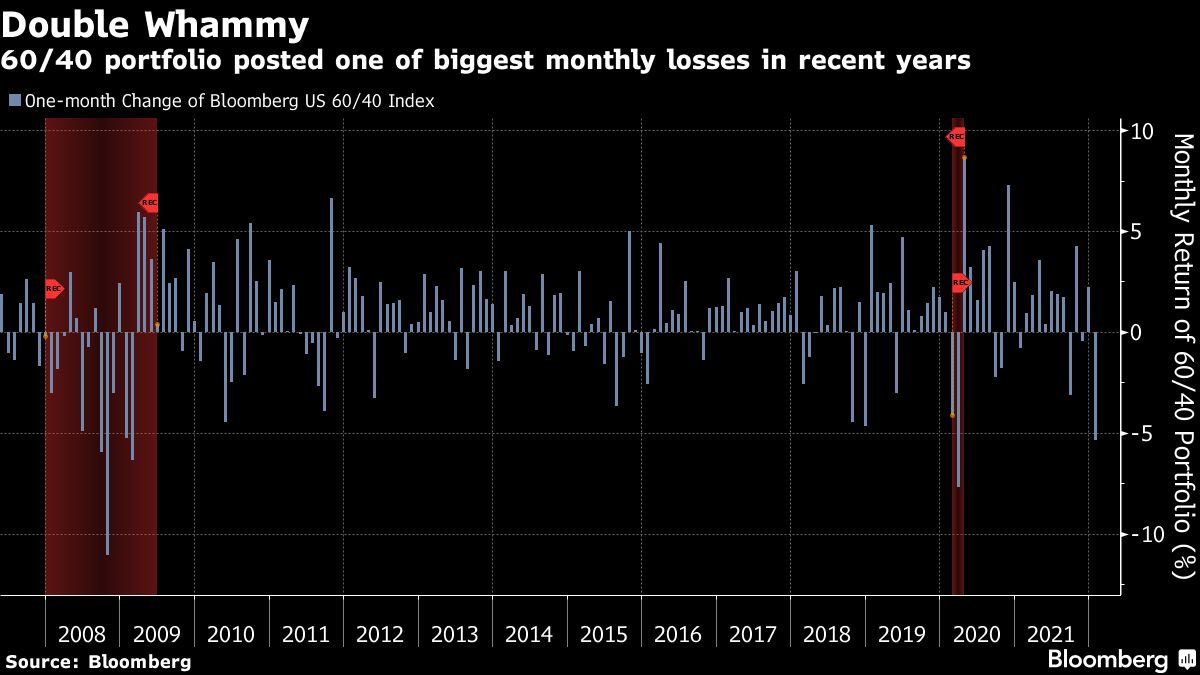

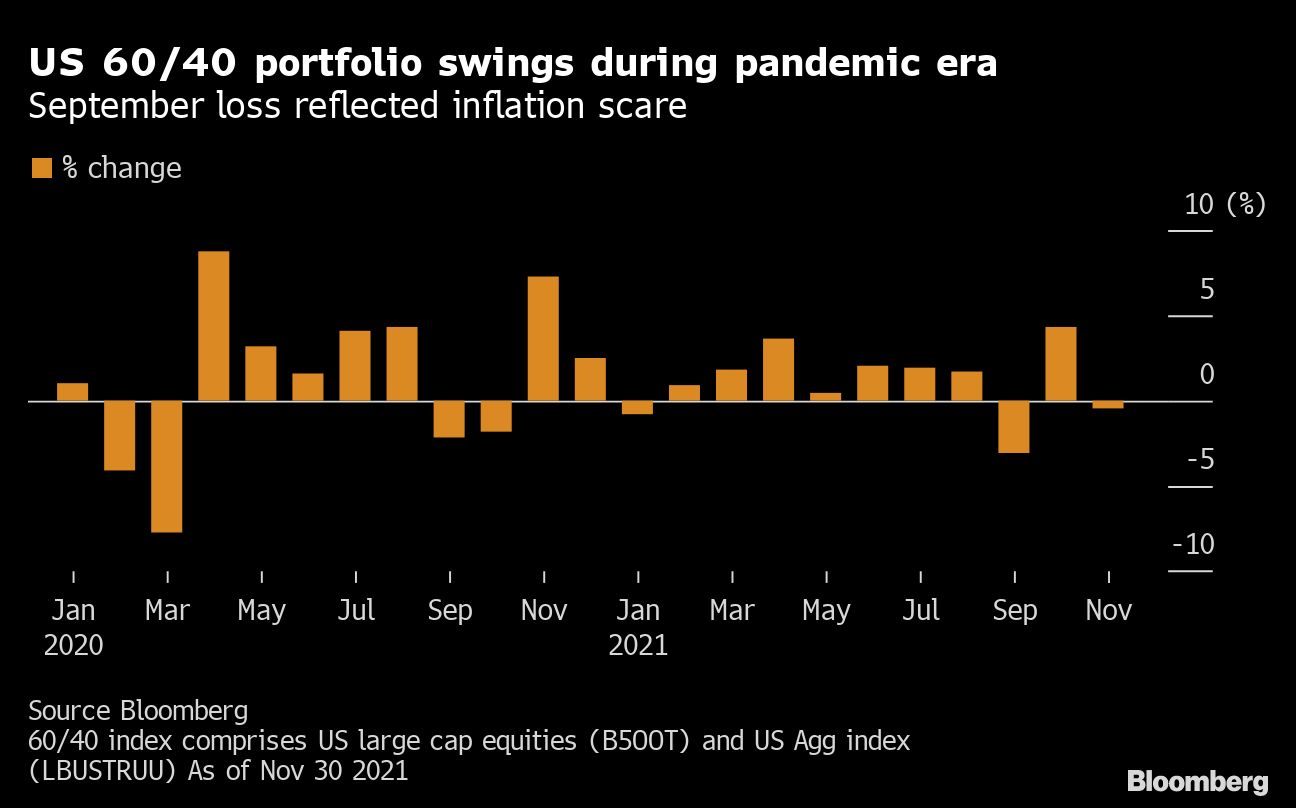

The classic 60/40 portfolio -- a strategy named for the share allocated to equities and high-grade debt, respectively -- is down more than 10% this year, leaving it on pace for the worst drubbing since the financial crisis of 2008.

The surging volatility in the world’s biggest bond market is challenging traders trying to play both tighter global monetary policy and a war-induced commodity price shock that’s raising the specter of 1970s-style stagflation.

The spreading global bond rout is spurring a Wall Street debate on whether investors will demand to be paid for lending to the American government like they used to.

A bedrock of long-term investing, a portfolio split 60/40 between equities and high-quality bonds, is set for its worst monthly slide since the market meltdown in the early days of the pandemic.

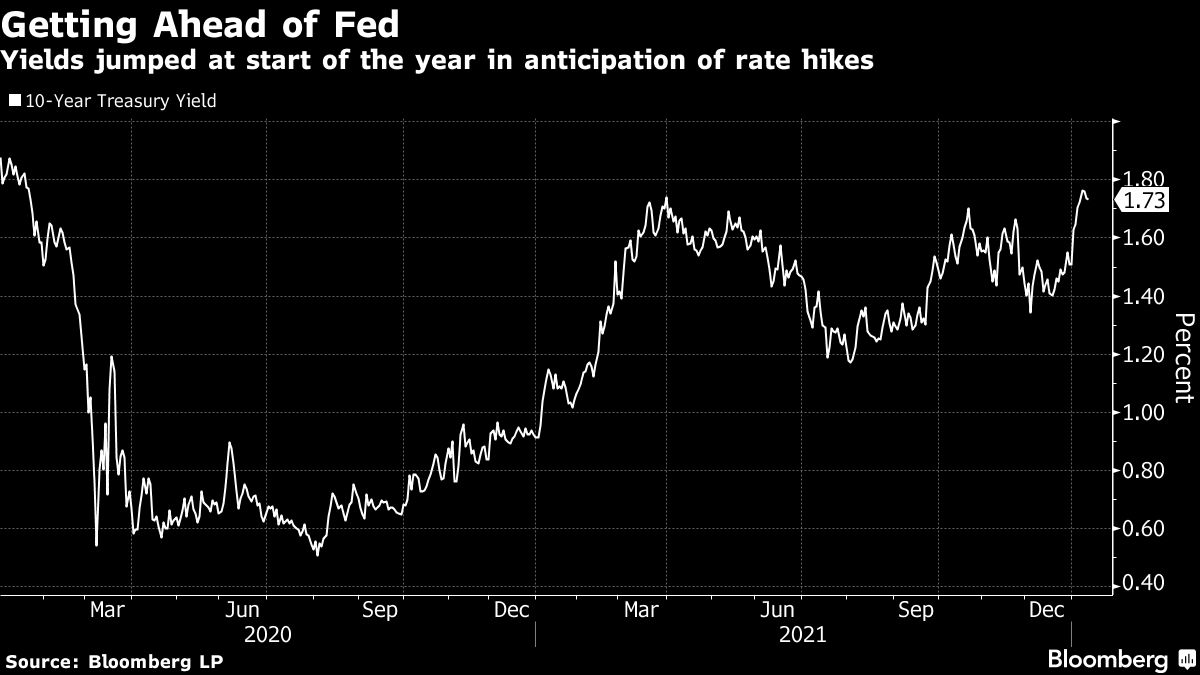

U.S. Treasuries shook off the steepest jump to consumer-price inflation in four decades and absorbed a 10-year note sale, with the figures reinforcing already widespread anticipation that the Federal Reserve will start raising interest rates in March.

Anyone gearing up for bond yields to surge in 2022 should think again. A global glut of saved cash has the potential to restrain an increase in rates, even as central banks dial back their pandemic stimulus.

Bond traders suspect the Federal Reserve will quickly discover it’s being too ambitious with its newly hawkish stance.

Wall Street likes to warn that past performance doesn’t guarantee future results, but when it comes to the traditional 60/40 mix of stocks and bonds, it kind of has. Persistent inflation could bring that to an end.