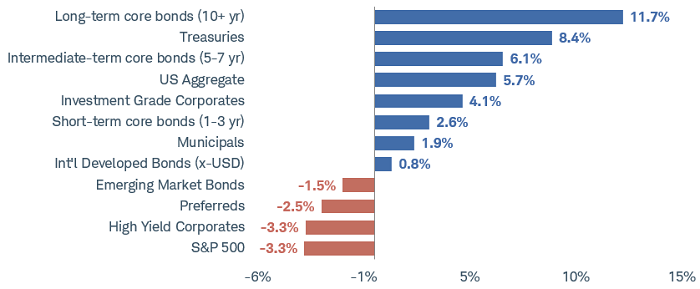

Returns for most fixed income asset classes are positive so far this year, but the numbers mask the rocky road markets have traveled since January.

Thanks in large part to the Federal Reserve’s decision to slash interest rates in response to the economic lockdown as the COVID-19 crisis spread, bonds with the least risk, like Treasuries, have posted the strongest returns, while returns for riskier segments of the market are slightly negative.

Fixed income asset class total returns, year-to-date

Source: Bloomberg. Returns from 12/31/2018 through 6/15/2020. Indexes representing the investment types are: Long-term core = Bloomberg Barclays U.S. Aggregate 10+ Years Bond Index; Treasuries = Bloomberg Barclays U.S. Treasury Index; Intermediate-term core = Bloomberg Barclays U.S. Aggregate 5-7 Years Bond Index; US Aggregate = Bloomberg Barclays U.S. Aggregate Index; Investment Grade Corporates = Bloomberg Barclays U.S. Corporate Bond Index; Short-term core = Bloomberg Barclays U.S. Aggregate 1-3 Years Bond Index; Municipals = Bloomberg Barclays US Municipal Bond Index; Int. developed (x-USD) = Bloomberg Barclays Global Aggregate ex-USD Bond Index; Emerging Market = Bloomberg Barclays Emerging Markets USD Aggregate Bond Index; Preferreds = ICE BofA Merrill Lynch Fixed Rate Preferred Securities Index; S&P 500 = S&P 500 Total Return Index (SPXT); HY Corporates = Bloomberg Barclays US High Yield Very Liquid (VLI) Index. Returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Bridging the economic gap to the new normal

Although returns have been generally positive, yields have swung widely as markets reacted to the sudden halt in economic growth, the Fed’s rapid rate cuts and fiscal stimulus, followed by nascent signs of recovery. For a few brief days in March, short-term Treasury yields were even negative, while high-yield (or “junk”) bond yields soared by more than 600 basis points (or six percentage points) relative to Treasury yields.1

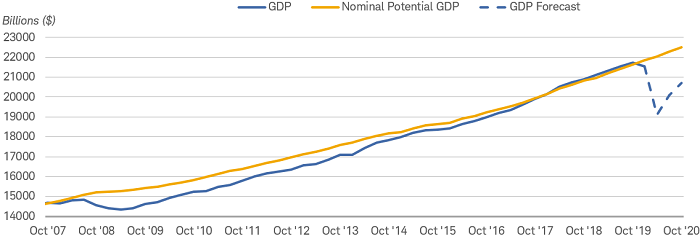

All of this volatility reflects the markets’ efforts to find a path through the economic downturn to the new normal. An enormous gap has opened up between the potential growth rate in the economy and actual growth rate. The gap represents the lost output of goods and services. It signals excess capacity in the economy and tends to put downward pressure on inflation. The Federal Reserve and Congress have tried to fill the gap with direct funds to households and loans to businesses.

Gross domestic product is running below potential, suggesting inflation is not a near-term threat

Source: U.S. Bureau of Economic Analysis and U.S. Congressional Budget Office. Nominal Potential Gross Domestic Product (NGDPPOT), Gross Domestic Product, and the Gross Domestic Product Forecast. Quarterly data as of Q1-2020 with forecast through Q4-2020.

The sum total of the programs put in place to date is approximately the equivalent of about a quarter’s worth of gross domestic product (GDP) growth. Despite the massive relief provided, the outlook still suggests that the economy will take time to recover. Consequently, inflation will likely remain low, and the Fed will maintain an easy policy stance. We expect that short-term interest rates will stay near zero for the next two years or perhaps longer.

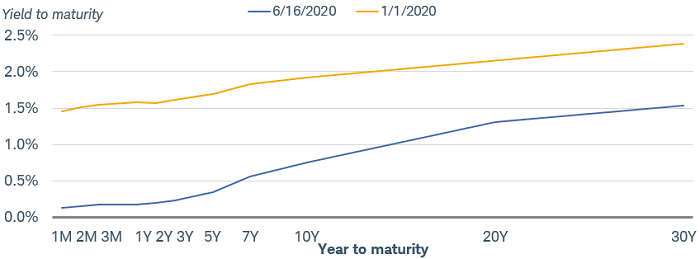

A steeper curve ahead

Assuming the economy rebounds in the second half of the year, longer-term yields could move higher. Signs of improving growth combined with an ever-increasing supply of Treasuries will likely result in moderately higher bond yields and a steeper yield curve. With a rising budget deficit, Treasury issuance is increasingly shifting toward longer-dated bonds, adding to the upward pressure on yields and steepening the curve. For the second half of the year, we believe 10-year Treasury yields could drift up to the 1% level.

Treasury yield curve has steepened since January

Source: Bloomberg as of 6/12/2020 and 1/1/2020. Past performance is no guarantee of future results.

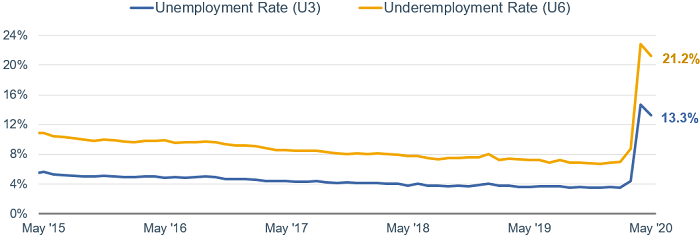

However, the upside is likely to be limited by ongoing low inflation and the Fed’s determination to hold short term rates lower for longer. Recent inflation data indicate consumer prices have fallen for three consecutive months and wholesale prices are falling on a year-over-year basis. High unemployment will also likely weigh on inflation. The rebound in hiring in May was welcome, but the overall unemployment rates are still very high.

Despite incremental progress in May, unemployment is very high

Source: Bureau of Labor Statistics. Civilian Unemployment Rate and Underemployment Rate, Total unemployed, plus all marginally attached workers plus total employed part time for economic reasons (U6 Rate), Percent, Monthly, Seasonally Adjusted. Shaded areas indicate past recession. Monthly data as of May 2020.

While many investors are concerned that the mix of easy monetary policy and loose fiscal policy will produce inflation, our view is that the fiscal relief is only partially filling the gap of lost wages and income for households and businesses. The Fed’s balance sheet expansion will likely boost asset prices rather than prices of goods and services, because the excess money will find its way into financial assets. That was the pattern after the 2008-09 financial crisis.

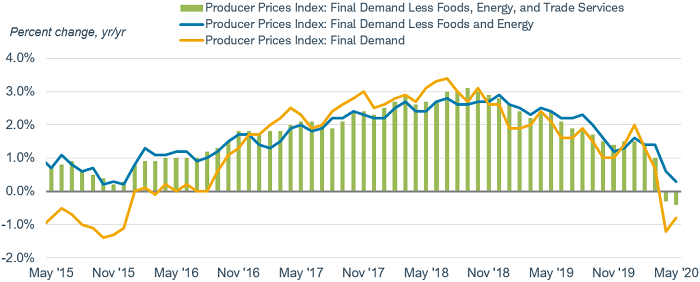

Deflationary pressures at the wholesale level reflect demand shock from COVID-19

Source: U.S. Bureau of Labor Statistics, U.S. Producer Price Index Final Demand, U.S. Producer Price Index Final Demand Less Foods Energy and Trade Services, Percent Change from Year Ago, Monthly, Seasonally Adjusted. Data as of May 2020.

Federal Reserve policy is working, so expect more of the same

With the unemployment rate high and inflation low, the Federal Reserve has indicated it is likely to stay on an easing path for the next few years. It is holding the fed funds rate near zero and continuing to increase its balance sheet at a gradual pace of about $120 billion per month in Treasuries and mortgage-backed securities. In addition, the Fed’s unconventional lending programs should continue to hold down yields in the riskier segments of the market.

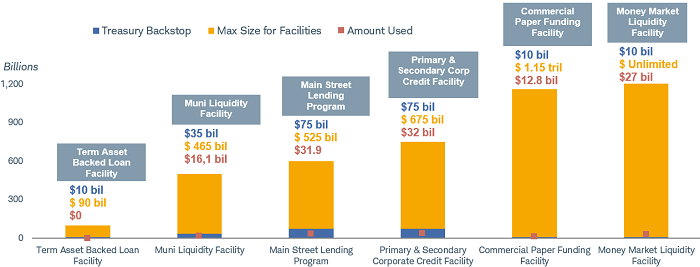

To date, these facilities haven’t been used very heavily. They are meant to be a last resort for borrowers, so terms can be stringent. Nonetheless, the Fed has had success with these facilities. It appears that just by signaling its support for markets, the Fed has succeeded in increasing the liquidity in markets and bringing yields down. It also means the Fed still has plenty of ammunition left to combat the risks of renewed weakening in the economy or deflationary pressures.

The Federal Reserve's relief programs still have plenty of ammunition left

Sources: Federal Reserve. H.4.1 Release showing the Treasury backstop, the maximum size, and amount shown on the Federal Reserve's balance sheet for the muni liquidity facility, the main street lending facility, the term asset backed loan facility, the primary and secondary credit facilities, the muni market liquidity facility, and the commercial paper funding facility. As of 06/10/2020.

The Fed’s lending facilities for businesses should support the corporate bond market, keeping yields low relative to Treasury yields. However, these programs are mostly targeted at investment-grade bonds—those with ratings of BBB or above—with only a small amount allocated to high-yield bonds. More downgrades and defaults are likely as companies struggle with an overhang of debt and soft demand. Similarly, there will likely be downgrades in the municipal bond market as state and local governments deal with reduced revenues and increased costs.

Although the Fed has plenty of ammunition left, there are other steps it could take. It could use yield curve control—that is, targeting its purchases of bonds to keep intermediate- or even long-term yields at a set level. We don’t see this as something that is needed now, but it could be used down the road if long-term yields begin to move up faster. The Fed could also use its “forward guidance” to limit a rise in bond yields by signaling that it won’t raise short-term rates or stop its easing programs until the unemployment rate falls to a certain level.

The policy options the Fed chooses will depend to a large extent on the pace of economic recovery. The Fed’s goals, full employment and inflation near 2%, appear to be a long way off. However, a “new normal” of declining unemployment and inflation edging higher is likely over the next few years.

Strategy for the second half

With the Federal Reserve keeping short-term interest rates near zero, yields on cash or short-term investments like Treasury bills, money market funds, and bank certificates of deposit are likely to remain quite low. Consequently, we would suggest limiting the allocation to cash to the amount that is needed for the next few years.

For higher yields, investors will need to take some kind of risk—either duration risk or credit risk or both. We favor limiting duration to reduce the risk of rising long-term rates, and suggest keeping the bulk of fixed income investments in bonds with higher than average credit ratings.

We continue to suggest investors keep the average durations in their portfolios somewhat below their benchmarks, as interest rates are so low. For example, if you typically invest in a fund that tracks a benchmark like the Bloomberg Barclays Aggregate Bond Index which has a duration of about 6, we would consider keeping the duration lower—perhaps in the 4-5 region—to reduce interest rate risk. However, as mentioned previously, we wouldn’t suggest moving all of a fixed income allocation to very short-term maturities, as we expect the Fed to keep short-term rates near zero until at least the end of 2021.

For investors concerned about inflation, an allocation to Treasury Inflation Protected Securities (TIPS) is an option. Since these bonds track overall CPI, they are designed to hedge inflation risk. However, yields are quite low or even negative. Consequently, if inflation rises an investor will have a higher real yield than in a nominal treasury but still quite low.

In the corporate bond market, we still expect to see more credit rating downgrades to highly leveraged companies in the investment-grade market and a wave of defaults in the high yield market. After the sharp rally, there is less compensation in the form of extra yield in the market for those risks than just a few weeks ago. We suggest investors avoid too much exposure to lower-rated corporate bonds and focus on issuers with stronger balance sheets that can weather the ups and downs of the recovery.

The Fed’s influence in the municipal bond market has been helpful in providing liquidity, but less in terms of supporting prices in the market. The interest rates available to issuers using the Municipal Lending Facility are relatively high, making it a lender of last resort. While most of the municipal bond market is still high quality, we do anticipate downgrades in the months ahead. The lockdowns put in place to fight the pandemic have put a strain on municipal budgets by reducing tax revenues and increasing costs. We suggest taking a close look at holdings to assess potential changes in the risk profiles of some bonds.

1 One basis point is equivalent to 0.01% (1/100th of a percent) or 0.0001 in decimal form.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0620-0Z7V)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab