The “wisdom of the crowd” isn’t always wise to follow. A recent article by Scott Nations via MarketWatch made an excellent point.

“It’s easy to become anxious as an investor. It’s particularly easy to become anxious when war is erupting in Europe, stock markets are gyrating, inflation is spiking, and the Federal Reserve is raising interest rates to snuff out that inflation.

So what do many investors do in times like this? While we like to think that we’ll be rugged individualists and go our own way, too often we reflexively look around to see what everyone else, the great lowing herd of investors, is doing. And then many of us will join that herd.”

What is herding?

“The term herd instinct refers to a phenomenon where people join groups and follow the actions of others under the assumption that others already did their research. Herd instincts are common in all aspects of society, but particularly within the financial sector. Investors tend to follow what they perceive other investors are doing, rather than relying on their own analysis.” – Investopedia

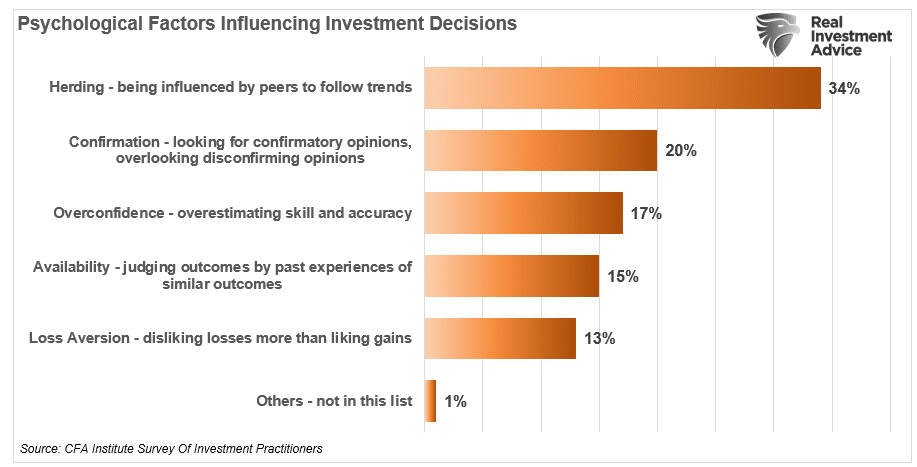

According to a C.F.A. Institute survey of investment practitioners globally, 34% stated that the “wisdom of crowds” or “herding” was the most significant contributor to investment decision-making.

The top rank for herding is a reminder of the lemming suicide myth in which lemmings end their lives by following one another off a cliff. However, before they can see the cliff’s edge, they believe the “wisdom of the crowd” in front of them knows where it’s going.

Right In The Middle, Wrong On Both Ends

Over the last few years, we have seen many examples of crowd wisdom. The rise of the terms such as “F.O.M.O.” (Fear of Missing Out,} to “Y.O.L.O” (You Only Live Once) and even “T.I.N.A” (There Is No Alternative) are clear examples of herding.

As others are “seemingly” making money, investors who are not participating follow the crowd because they feel their economic status will fall relative to those participating. That behavior causes even more of the same behavior, and bubbles eventually form.

Important Note:

In the very short term, political, fundamental, and economic data has very little influence over the market. Such is especially the case in a late-stage bull market advance where “crowd wisdom” exceeds the grasp of the risk undertaken by investors.

In other words, “price is the only thing that matters” in the short term.

Price measures the current “psychology” of the “herd” and is the clearest representation of the behavioral dynamics of the living organism we call “the market.”

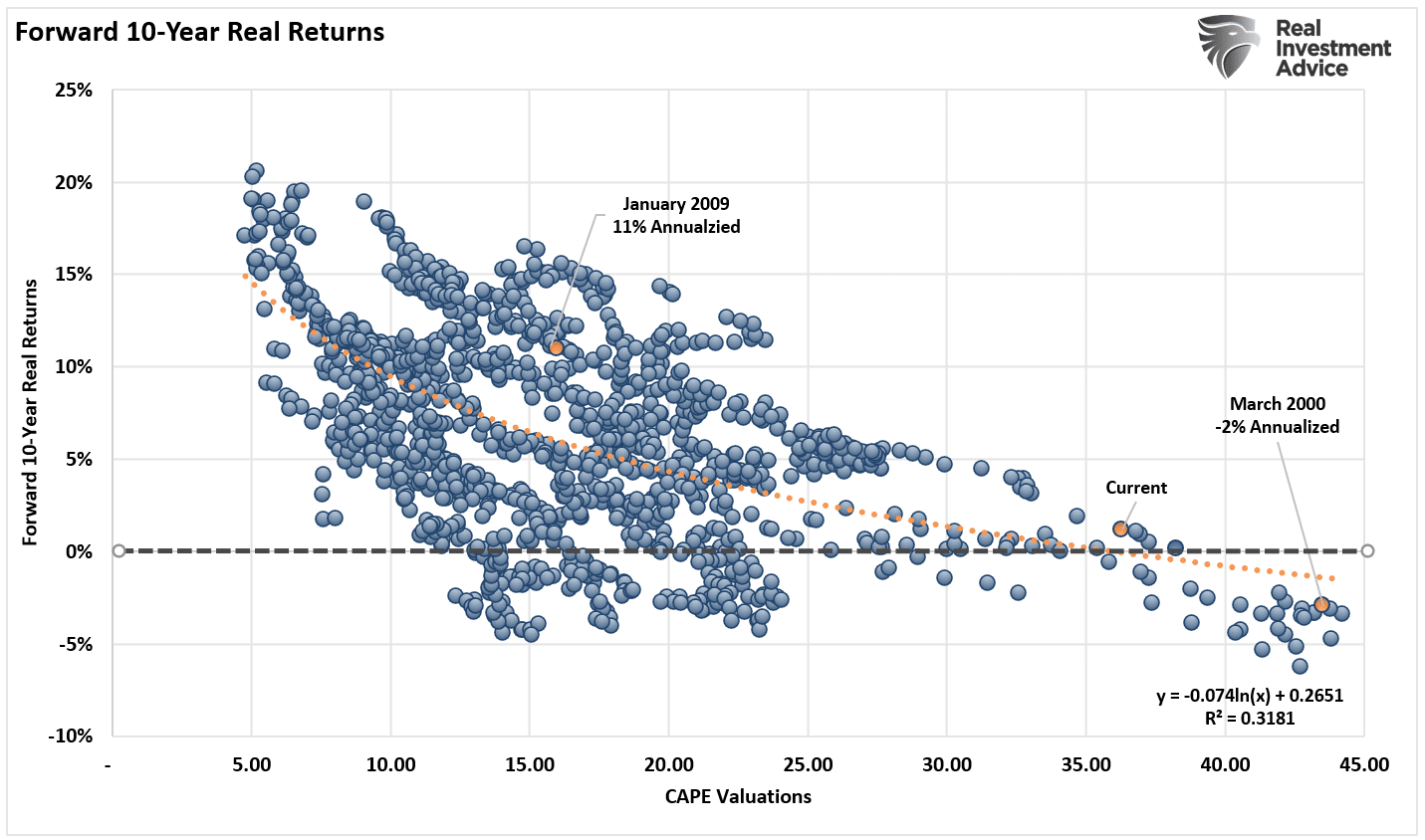

But in the long-term, fundamentals are the only thing that matters. As the chart below shows, 10-year forward total real returns from current margin-adjusted valuations are not promising.

Source: Dr. Robert Shiller Data Chart by Real Investment Advice

We Now Return To Our Message

The “herding” effect worked very well for a while as investors chased surging prices supported by government and Federal Reserve interventions.

Investors armed with a fresh stimulus check, a “Robinhood” app, and membership to #WallStreetBets piled into many investment options to “get rich quick.”

Meme stocks such as Peleton, Zoom, and others.

Thematic stocks such as “Space” related stocks.

SPACs (Special Purpose Acquisition Companies) took money HOPING to find an investment.

Speculative investments funds such as ARKK Innovation (ARKK).

Leveraged funds

Record levels of speculative option buying

Not surprisingly, it all ended rather poorly.

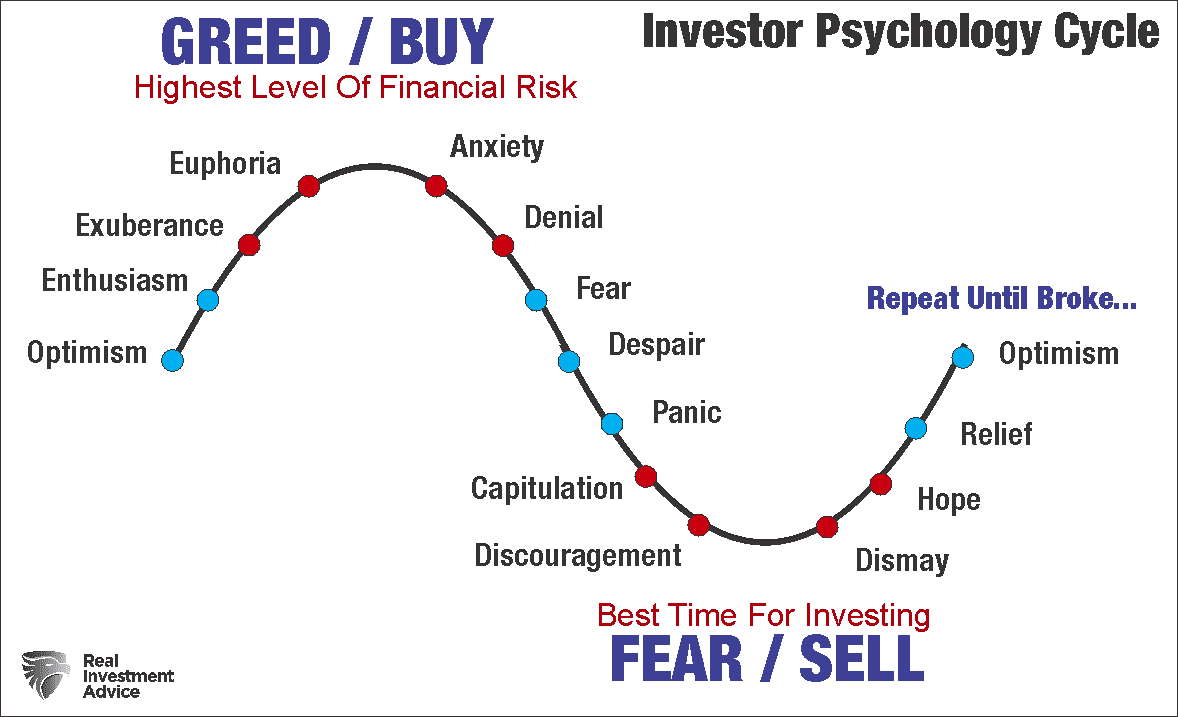

Historically, following the herd always works in the middle of a market rise or fall. However, “crowd wisdom” is ALWAYS wrong at the extremes.

Source: FX Street Chart Reconstructed By: Real Investment Advice

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham.

But can we do better as investors?

Rothchild’s Elegant Solution

While it is easy to get swept up by the herd as prices are rising or falling, we can manage the risk in our portfolio.

You can not effectively and repetitively get “in” and “out” of the market in a timely fashion. Such is neither portfolio nor risk management. However, you can manage risk by adjusting market exposure when “risk” outweighs the potential for further “reward.”

Every investment strategy has a consequence and will lose money from time to time. The only difference is the amount of the loss, what causes it, and the amount of time lost in reaching your investing goals.

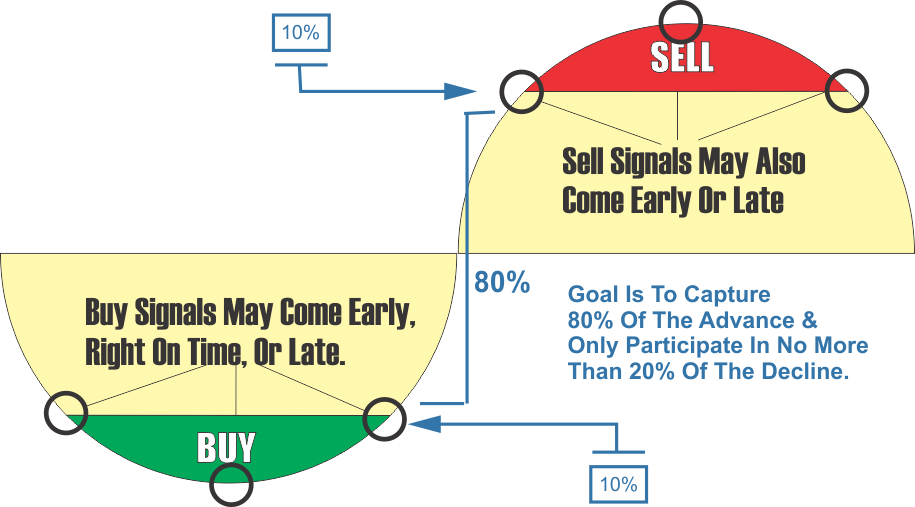

Baron Nathan Rothschild had an elegant solution to solve the “herding” problem. If the “herd” is correct in the middle but wrong at the extremes, avoid the extremes.

“You can have the top 20% and the bottom 20%, I will take the 80% in the middle.”

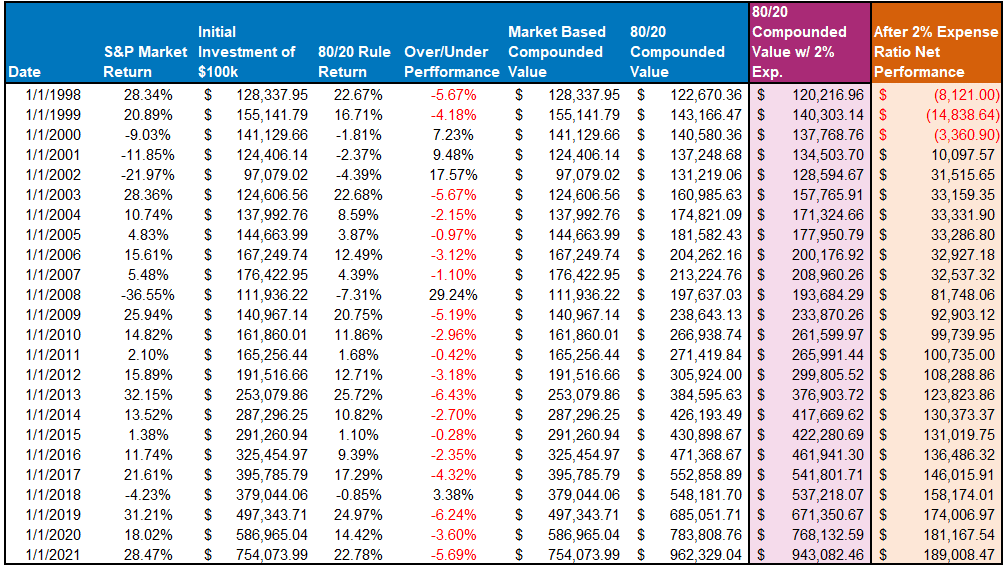

The following is a graphical example of the 80/20 investment philosophy.

Putting It To The Test

The 80/20 rule is the basis of our investment management process. Importantly, you will NOT beat the market from one year to the next. However, you will avoid the “time loss” required to “get back to even.” Such gets shown in the example below.

($100,000 investment in the S&P 500 returns a far lower value than the “Rothschild 80/20 Rule” model. Even if I include a 2% management fee.)

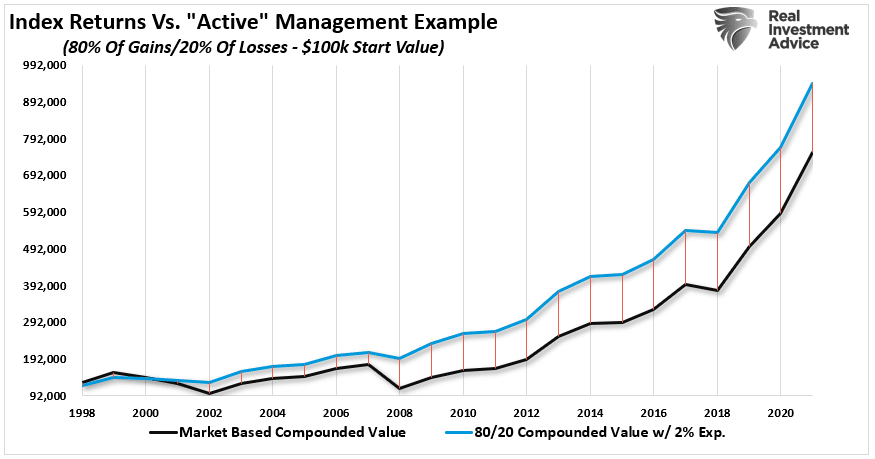

Here is a chart to illustrate the deviation more effectively. (Capital appreciation only.)

Notably, even though the model underperforms MOST years, the reduced levels of volatility allowed investors to emotionally “stick” to their discipline over time. Furthermore, assets can “compound” over the long term by minimizing the drawdowns.

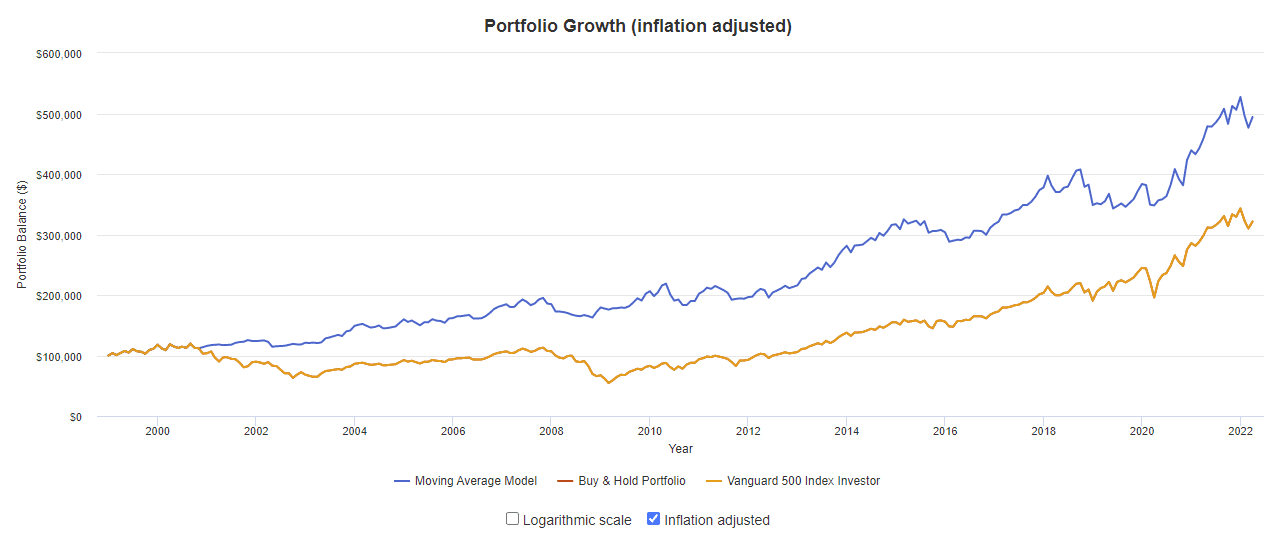

An easy way to apply this principle is to use a simple moving average crossover. In the chart below, an investor is long the S&P 500 index when it is above the 12-month moving average. They would then switch to bonds when the index falls below the 12-month average. (You can run this backtest yourself at Portfolio Visualizer)

No, it’s not perfect every time. But no measure of risk management is.

But having a discipline to manage risk is better than not having one at all.