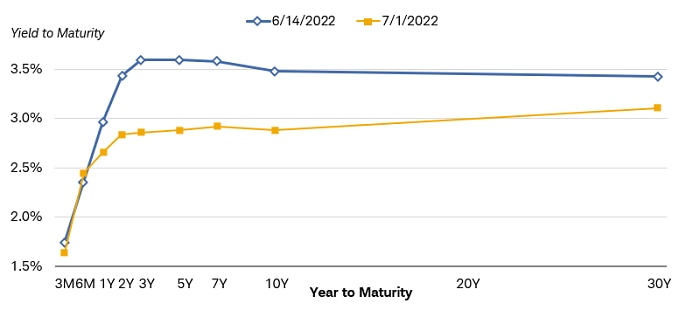

The Federal Reserve's pledge to curb inflation appears to have resonated with the market. If the central bank raises rates as much as recent projections indicate, the risk of recession rises. Consequently, bond yields have been pulling back from recent highs and the yield curve has flattened.

It's fair to say that earlier this year, central bankers were struggling to communicate their intentions clearly to the markets. However, that doesn't appear to be the case any longer. In the United States. Federal Reserve Chair Jerome Powell and the members of the Federal Reserve's policy-making Open Market Committee (FOMC) have been steadfast in signaling their commitment to fighting inflation. If there is a communication problem, it's mostly that central bankers don't want to admit out loud that getting inflation down raises the risk of recession.

European Central Bank (ECB) President Christine Lagarde is facing an even more difficult problem. The ECB wants to raise rates due to rising inflation stemming from the spike in energy prices. However, the data suggest that Europe's economy is weakening—largely due to the rise in energy prices. Meanwhile the ECB also wants to limit the widening in bond spreads between core and peripheral countries as markets focus on recession risks in countries with high debt levels. Talk about a policy dilemma.

Not to be left out, Bank of Japan (BOJ) President Haruhiko Kuroda has had to apologize repeatedly over the past few weeks for saying that Japanese consumers don't mind rising inflation stemming from the yen's steep drop. The problem is that the BOJ is trying to have it all ways. It wants to maintain its zero-interest-rate policy and yield-curve control, while also preventing the yen from falling to a new multi-decade low.

Not surprisingly, markets have been roiled by these confusing and sometimes circular arguments coming from central bankers. But in my view, the bond market has it figured out. Since the Fed's last meeting, Treasury yields have fallen across all maturities. In fact, short-term yields peaked on the first day of the Fed's last meeting, when the federal funds rate was raised by 75 basis points (or three-quarters of a percentage point).

The yield curve has flattened since the last FOMC meeting

Source: Bloomberg, data as of 6/14/2022 and 6/30/2022.

Past performance is no guarantee of future results.

It looks like the Fed's actions and pledge to bring inflation down have resonated with the market. If the Fed follows through in hiking rates as much as the recent projections indicate, the risk of recession rises. Consequently, bond yields have been pulling back from recent highs and the yield curve has flattened.

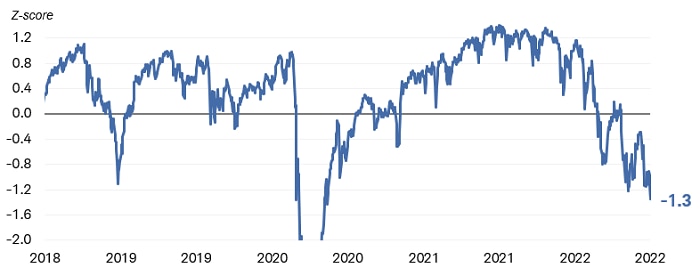

Bloomberg Financial Conditions Index

Source: Bloomberg. Bloomberg U.S. Financial Conditions Index (BFCIUS Index), daily data as of 6/30/2022.

Note: The Bloomberg U.S. Financial Conditions Index tracks the overall level of financial stress in the U.S. money, bond, and equity markets to help assess the availability and cost of credit. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions relative to pre-crisis norms. Y-axis is truncated at -2.0 for scaling purposes. For reference, the low occurred on 3/24/2020 and was -6.33. The Z-Score indicates the number of standard deviations by which current financial conditions deviate from the average. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions.

The case for lower bond yields in the second half of the year

Economic growth is slowing

Gross domestic product (GDP) growth contracted in the first quarter, driven primarily by a drop in consumption. Since consumer spending comprises about 70% of GDP growth, a slowdown in spending is concerning. Early indications point to a risk that Q2 GDP growth was also likely weak. Two negative quarters of GDP growth isn't the official definition of recession, but it signals that the indicators are pointing in that direction.

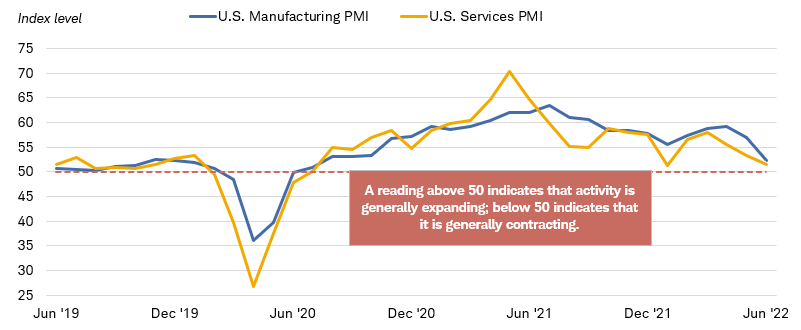

In addition to weaker consumer spending, housing and manufacturing activity have slowed in recent months. Notably, the softening in demand is coinciding with increasing supply. Housing inventories are increasing, and houses are sitting on the market longer as affordability drops. Purchasing manager index (PMI) data points to slowing momentum in both manufacturing and services.

PMI for both manufacturing and services activity has softened

Source: Bloomberg.

U.S. Manufacturing PMI SA (MPMIUSMA Index) and U.S. Services PMI Business Activity SA (MPMIUSSA Index). Monthly data as of 6/30/2022.

In the manufacturing sector, the difference between new orders and inventories is negative—something that usually coincides with a drop in GDP growth. Rising inventories relative to slowing demand suggest that inflation pressure stemming from shortages of goods should ease.

The difference between new orders and inventories is negative

Source: Bloomberg.

GDP US Chained 2012 Dollars YoY SA (GDP CYOY Index). Quarterly data as of Q2 2022. Institute for Supply Management (ISM) Manufacturing New Orders (NAPMNEWO Index) - ISM Manufacturing Inventories (NAPMINV Index). Monthly as of 5/31/2022.

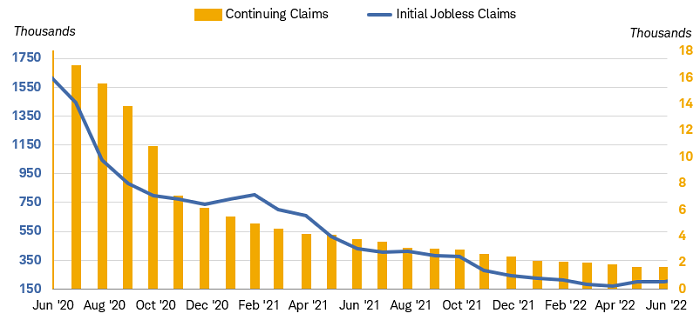

The labor market, which is a lagging indicator for the economy, is also showing signs that hiring momentum is slipping. Initial jobless claims have been rising since the second quarter, and the four-week moving average reached its highest level since January. Despite the repeated concern expressed by Fed officials that the labor market is strong—even "too strong"—the high-frequency data suggest it is softening.

The four-week moving average of jobless claims has ticked upward

Source: Bloomberg.

US. Employment and Training Administration. Weekly Initial Jobless Claims (INJCJC Index) and Continuing Claims (INJCSP Index). Data as of 6/30/2022.

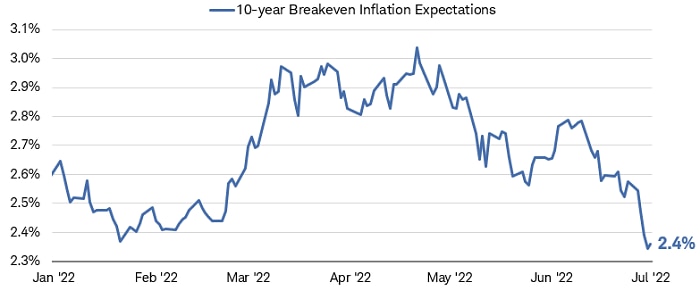

Inflation expectations have declined

One reason the Fed has given for an aggressive pace of tightening is the fear that inflation expectations will become "unanchored" and therefore self-fulfilling. If consumers and businesses believe prices will be higher in the future, they may pull forward consumption and drive demand even higher relative to supply. Moreover, workers may demand higher wages to keep up with inflation, causing a "wage-price spiral." It was the reason cited by Powell for the 75-basis-point rate hike at the last FOMC meeting.

However, market-based readings of inflation expectations peaked at just over 3% in April and have fallen back since then. The implied 10-year average inflation derived from the TIPS market fell to as low as 2.3% in early July (July 5, 2022) despite current inflation of more than 8%. It’s estimated that the Fed’s “comfort zone” is for inflation expectations in the 2.0% to 2.5% range.

Inflation expectations discounted in TIPS market have fallen

Source: Bloomberg.

U.S. Breakeven 10 Year (USGGBE10 Index). Daily data as of 6/30/2022.

Falling commodity prices

Over the past few months, prices in many commodity groups have dropped—from copper and other industrial metals to grains and even oil. After a surge in prices as the global economy emerged from the pandemic, prices have begun to drop back, signaling slower goods inflation going forward.

Copper prices have declined

Source: Bloomberg. Copper Future Sep22 (HGU2 Comdty). Daily data as of 6/30/2022.

For illustrative purposes only. Past performance is no guarantee of future results.

Since much of the increase in inflation over the last year can be attributed to the shortage of the supply of goods relative to demand, the recent drop in prices suggests less inflation in the pipeline.

Quantitative tightening will drain liquidity from the financial system

It hasn't been front and center in the news lately, but the Fed has begun to allow its balance sheet to decline. This will contribute to the tightening in financial conditions. As the Fed allows bonds to mature and "roll off" its balance sheet, it tends to shrink the amount of money available in the financial system. As a result, the monetary base—the total amount of money in circulation—declines. In that way, a declining balance sheet has the same effect as rate increases. Economists estimate that quantitative tightening (QT) probably will be equivalent to 100 basis points1 in tightening or more, depending on how far it extends.

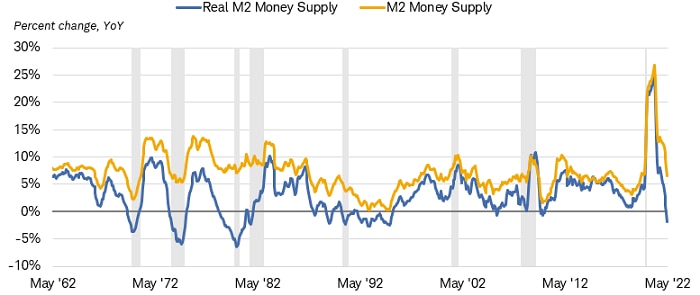

Recently, the growth rate in money supply has begun dropping sharply after rising sharply from the pandemic lows. The current year/year growth rate in M2 money supply2 is 6.6%, near the average of the 2014-2019 period. In real terms—that is, adjusted for inflation—money supply growth is negative—consistent with tight monetary policy.

Real money supply growth is negative

Source: Federal Reserve Bank of St. Louis.

Real M2 Money Stock and M2, Percent Change from Year Ago, Monthly, Seasonally Adjusted. Monthly data as of 5/31/2022. Shading represents past recessions.

Note: M2 is a measure of the money supply that includes cash, checking deposits, and easily-convertible near money. M2 is closely watched as an indicator of money supply and future inflation, and as a target of central bank monetary policy. Real M2 Money Stock Series deflates M2 money stock with CPI.

How low can they go?

With headline inflation still high, it may be hard for bond yields to fall much below 2.75% in the near term. However, it also appears that the 3.5% level reached in June could mark the high for the year. If recent economic trends continue, it would not be surprising to see 10-year Treasury yields fall further in the second half of the year, perhaps as low as 2.5%. That may prompt the Fed to slow its pace of rate hikes and/or alter its tightening plan later in the year. However, it may seem counterintuitive, but the more the Fed "front loads" its rate hikes and runs the risk of triggering a recession, the lower bond yields can fall.

We suggest investors looking to add more yield to their portfolios consider adding more duration—exposure to interest rate risk—to their portfolios with bonds that have low credit risk, such as Treasuries and investment-grade corporate and municipal bonds. A bond ladder strategy can be an effective way to average into the market.

10-year Treasury yields may have peaked in June

Source: Bloomberg.

U.S. Generic 10-year Treasury Yield (USGG10YR INDEX). Daily data as of 6/30/2022. Past performance is no guarantee of future results.

1 One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001.

2 M2 is a measure of the money supply that includes cash, checking deposits, and easily-convertible near money.

© Charles Schwab

Read more commentaries by Charles Schwab