Since the beginning of October, the market has performed better as a “Fed Pivot” bull case pushed investors into the market. We previously laid out the case for a strong “short squeeze” around the lows of September, stating:

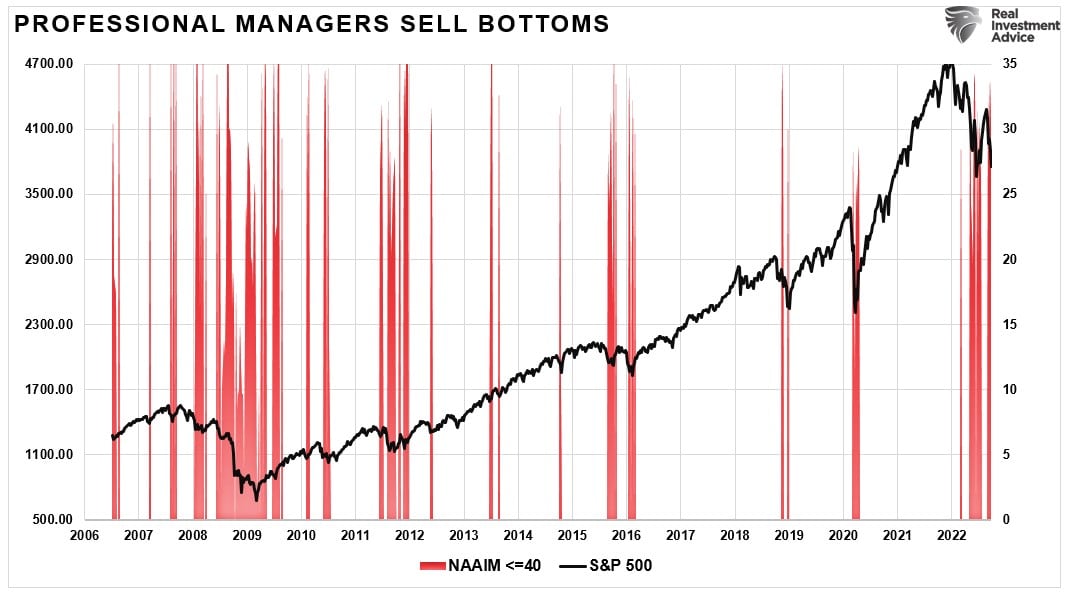

“Currently, everybody is bearish. Not just in terms of ‘investor sentiment’ but also in ‘positioning.’ As shown, professional investors (as represented by the NAAIM index) are currently back to more bearish levels of exposure. Notably, when the level of exposure by professionals falls below 40, such typically denotes short-term market bottoms.

As a contrarian investor, excesses get built when everyone is on the same side of the trade.

Everyone is so bearish that the reflexive trade will be rapid when sentiment shifts."

The ensuing short squeeze ultimately produced one of the most significant gains on record, with the S&P 500 surging over 5% single day. As we noted, such gains have two primary features. First, they are generally only seen during bear markets. Secondly, while they tend to come in the latter stages of bear markets, they don’t historically denote THE bottom.

As noted, we expected the rally from the September lows, as discussed in that previous post. However, what was critical was our concluding statement.

“There are plenty of reasons to be very concerned about the market over the next few months. We will use rallies to reduce equity exposure and hedge risks accordingly.

A ‘short squeeze’ is coming, but we aren’t out of the woods yet.”

That remains our positioning currently, as there are two primary issues plaguing the “bull case.”

The Fed…And The Fed

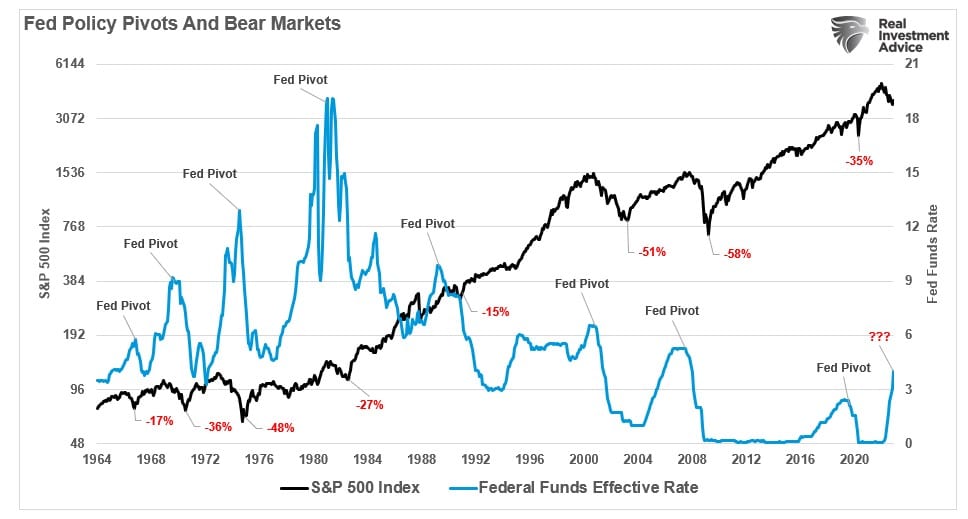

While investors chased the market, hoping the Federal Reserve will “pivot” concerning its monetary policy, the reality is likely substantially different. Such was a point we discussed in “The Policy Pivot May Not Be Bullish.”

“The bullish expectation is that when the Fed finally makes a ‘policy pivot,’ such will end the bear market. While that expectation is not wrong, it may not occur as quickly as the bulls expect.

Historically, when the Fed cuts interest rates, such is not the end of equity ‘bear markets,’ but rather the beginning.

The reason is that the policy pivot comes with the recognition that something has broken either economically (aka ‘recession’) or financially (aka ‘credit event’). When that event occurs, and the Fed initially takes action, the market reprices for lower economic and earnings growth rates.”

Notably, the bull case for a pivot is built on the idea of the Fed ceasing its rate hikes. However, a “pivot” that would support higher asset prices would require two primary monetary policy changes.

Dropping the Fed Funds rate toward the zero bound; and,

Reversing “Quantitative Tightening” to “Easing” provides market liquidity.

As the chart shows, these periods of zero rates and monetary accommodation fuel asset prices higher. Periods of balance sheet contraction and higher rates lead to market sell-offs.

Currently, even if the Fed does slow or stops hiking rates, there is NO indication they are about to reverse course from a “tightening” policy regime to an “accommodative” one.

In fact, just yesterday, Nick Timiraos from the Wall Street Journal confirmed the same. To wit:

“Federal Reserve officials have signaled plans to raise their benchmark interest rate by 0.5 percentage point at their meeting next week, but elevated wage pressures could lead them to continue lifting it to higher levels than investors currently expect. Brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors."

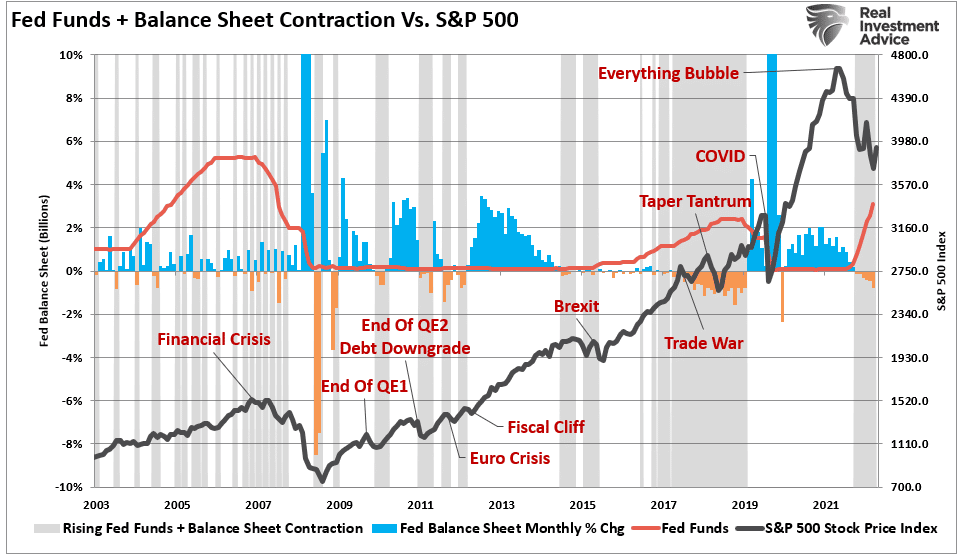

In other words, the most significant challenges to the bull case remain the Fed not cutting interest rates and the Fed not engaging in “Quantitative Easing.”

Playing The Probabilities

While the history of financial interventions and market performance is quite evident, there is always a possibility “this time could be different.”

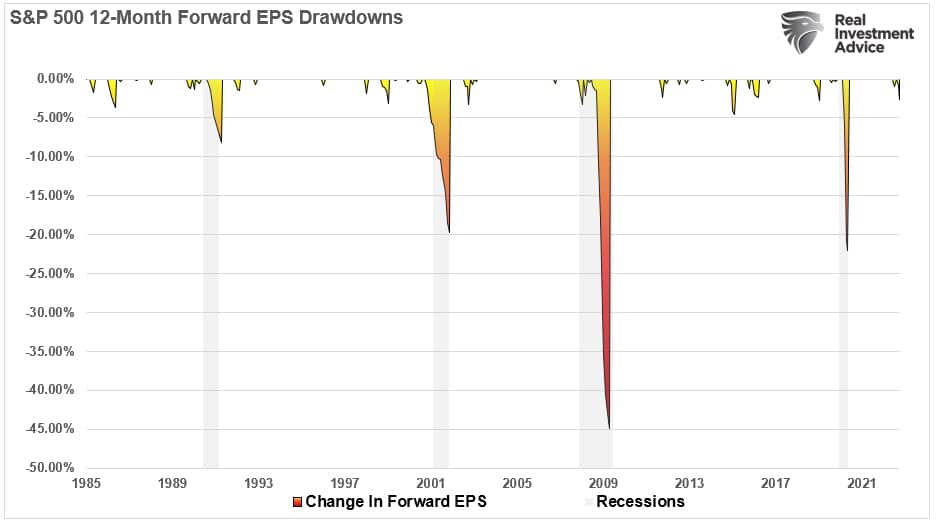

Yes, it is possible the bull case could mature if the economy avoids a recession, earnings stabilize, and inflation falls. However, given the lag effect of restrictive monetary policy (i.e., higher rates) and demand destruction, the risk of a recession is elevated. As such, earnings have not adjusted nearly enough to account for the reduction in consumer demand.

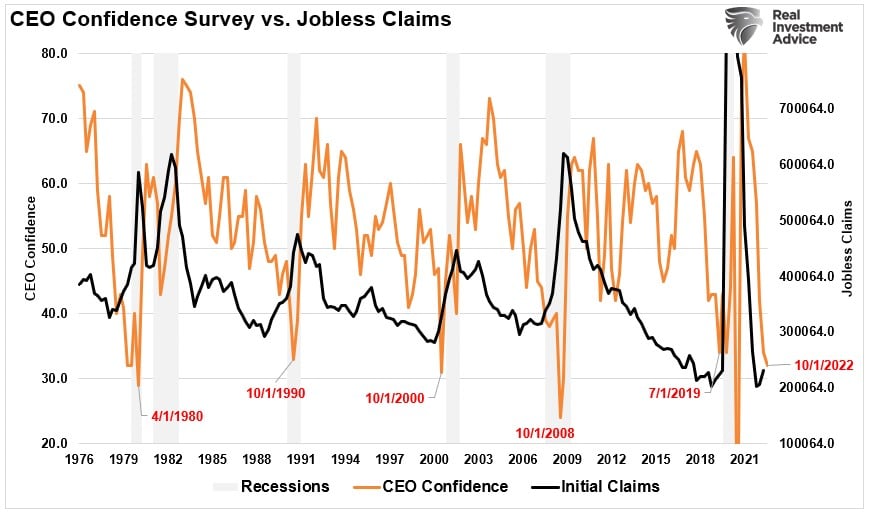

More importantly, the “lag effect” of monetary tightening has yet to reflect in the economic data. While the economy is slowing somewhat, employment has yet to contract. Already, we are seeing a sharp decline in CEO confidence as more companies lay off workers and institute hiring freezes. As shown, such eventually translates into higher unemployment, slower economic growth, and reduced expectations for future earnings.

As noted, anything is possible. However, as investors, we must “play the probabilities” for the current economic environment. The Fed hikes rates to quell inflation by creating “demand destruction” in the economy. Such will lead to higher unemployment, slower economic growth, and reduced earnings. All of which are not supportive of higher asset prices or elevated valuations.

Yes, the market could defy fundamental realities and front-run the Federal Reserve to the next round of monetary accommodation. However, given that strong market rallies curtail the Fed’s efforts, the bull case may keep the Fed in a restrictive mode longer than anticipated.

It seems to us that the bull case may be too far ahead of reality. If that is true, being a little more cautious and selling rallies may hedge the risk one final leg lower in 2023.