Treasury Yields: The Long and Winding Road to 5%

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBack in 2012 I wrote an article entitled, "The long and winding road back to 5% Treasury yields." At the time, I estimated that it would take at least another three years for yields to climb that high after the economic damage done by the great financial crisis of 2008. But a few years turned into a decade, as inflation and economic growth remained tame, and the global pandemic sent yields plunging back to near zero.

Now that yields have recovered from that lost decade and look poised to move even higher, it seems like a good time to re-assess the outlook for rates and portfolio positioning.

Five takeaways on reaching 5%

All indications are that the Federal Reserve is likely to raise its target range for the federal funds rate by another 25 basis points, to 5.25% to 5.50%, at its July 25-26 meeting and leave the door open to another increase in the fall. At a minimum, the Fed has signaled it plans to hold rates at these high levels at least through the end of the year—until it is confident that inflation is headed back to its 2% target.

For investors a "higher for longer" peak (or "terminal rate") for the federal funds rate in this cycle has several implications:

1. The downside potential in intermediate- to long-term yields for this year is likely higher than we previously expected. Intermediate- to long-term rates reflect expectations for the path of the fed funds rate plus a risk premium. Continued Fed tightening will likely pull rates higher across the yield curve. Rather than the 3.0% to 3.25% year-end target we had previously expected for 10-year Treasuries, a lower bound of about 3.5% is more likely and a re-test of the 2022 peak of 4.25%-4.35% is possible.

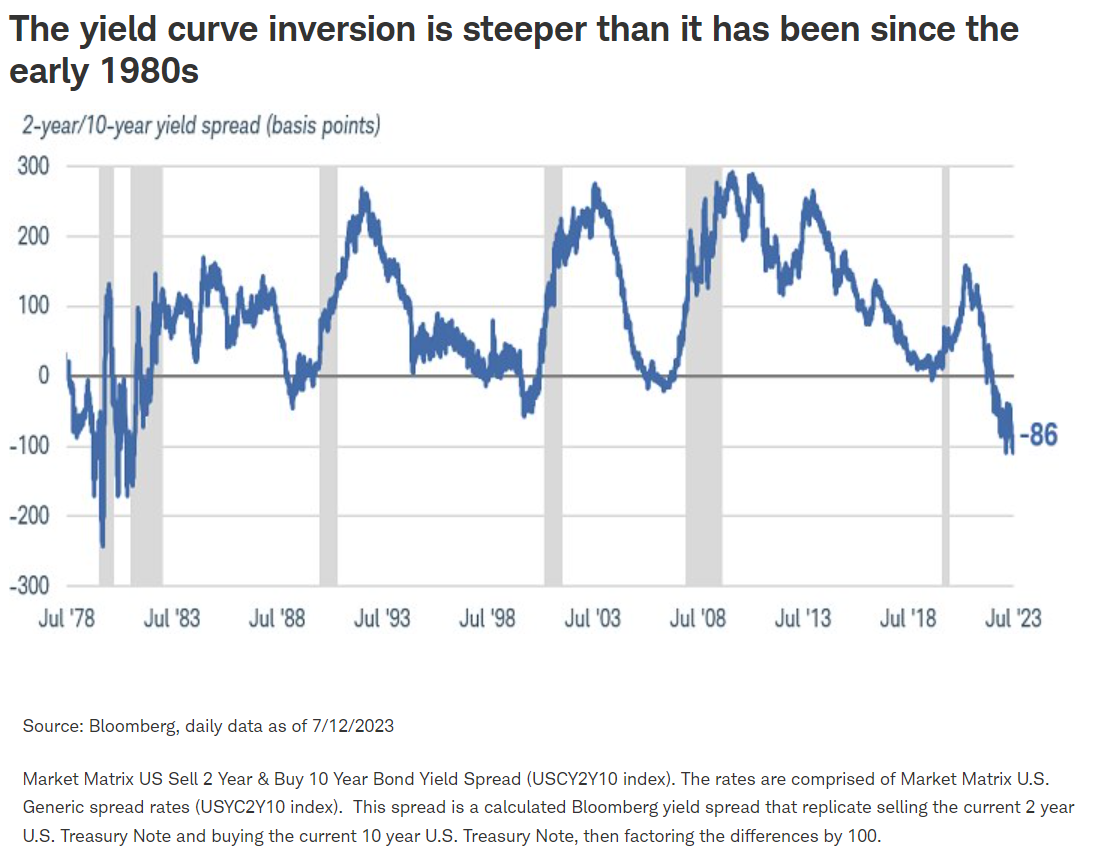

We expect the yield curve to remain inverted, but it is already near historically low levels last seen in the early 1980s. At a spread of about 100 basis points between two- and 10-year yields, more rate hikes are likelier to pull up yields across the curve than to deepen the inversion to new lows. Once a downturn in the economy begins, then 3% is still a reasonable downside target for 10-year yields—but that looks unlikely until 2024.

2. Volatility is likely to rise. In the bond market, volatility reflects uncertainty about the path of interest rates. With the Fed signaling the potential for more rate hikes and the market discounting the potential for rate cuts early next year, the tug-of-war between the market and the Fed will likely mean volatility stays elevated. It has retreated from the peak level reached in March but is well above the long-term average.

3. Credit spreads are more likely to rise than fall. So far in this cycle, credit spreads have stayed low, despite some volatility. The average spread of the Bloomberg U.S. Corporate High-Yield Bond Index is close to 4%, below its long-term average and well below previous peaks hit during periods of market stress or economic slowdowns. We expect spreads to rise, because further Fed tightening implies that economic growth will likely slow, resulting in more defaults from sub-investment-grade-rated issuers.

In general, we believe investment-grade corporate bond spreads are likely to remain relatively stable, but high yield bond spreads have the potential to widen, pulling down their prices.

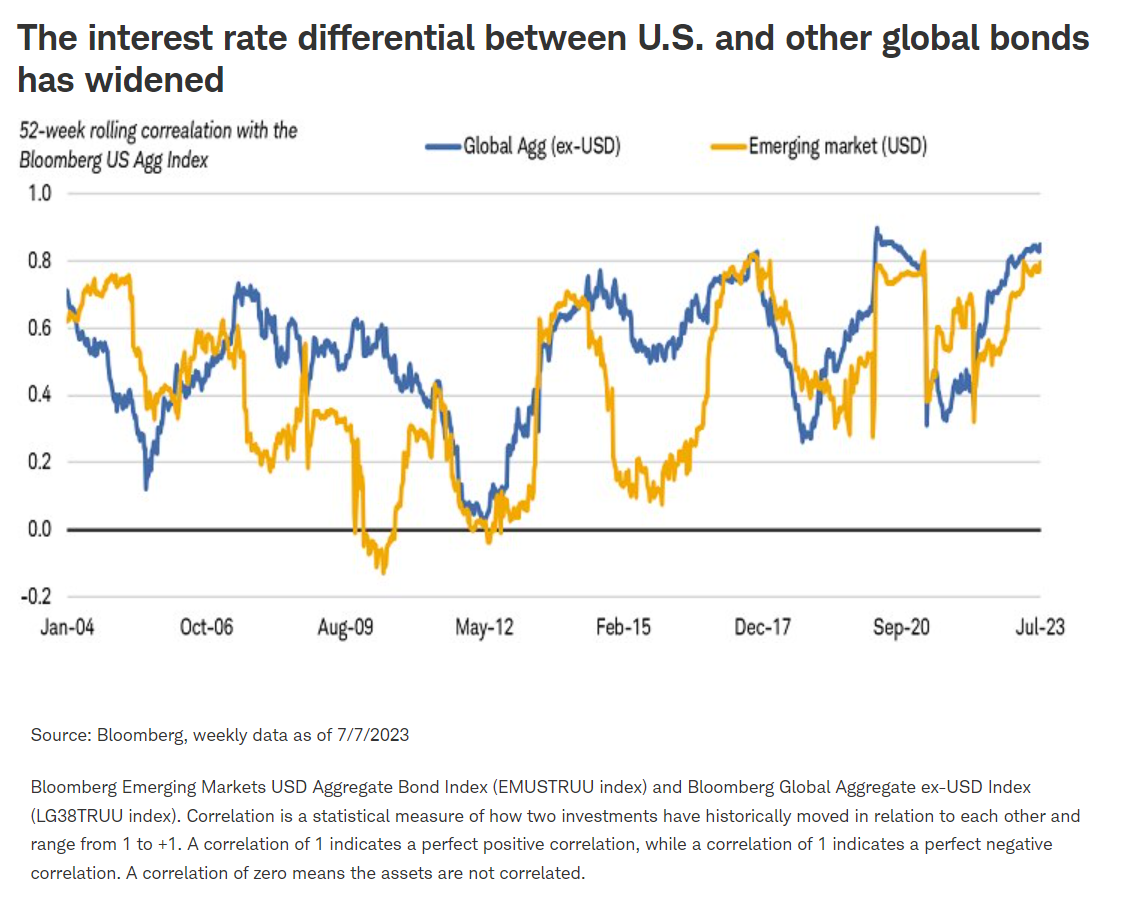

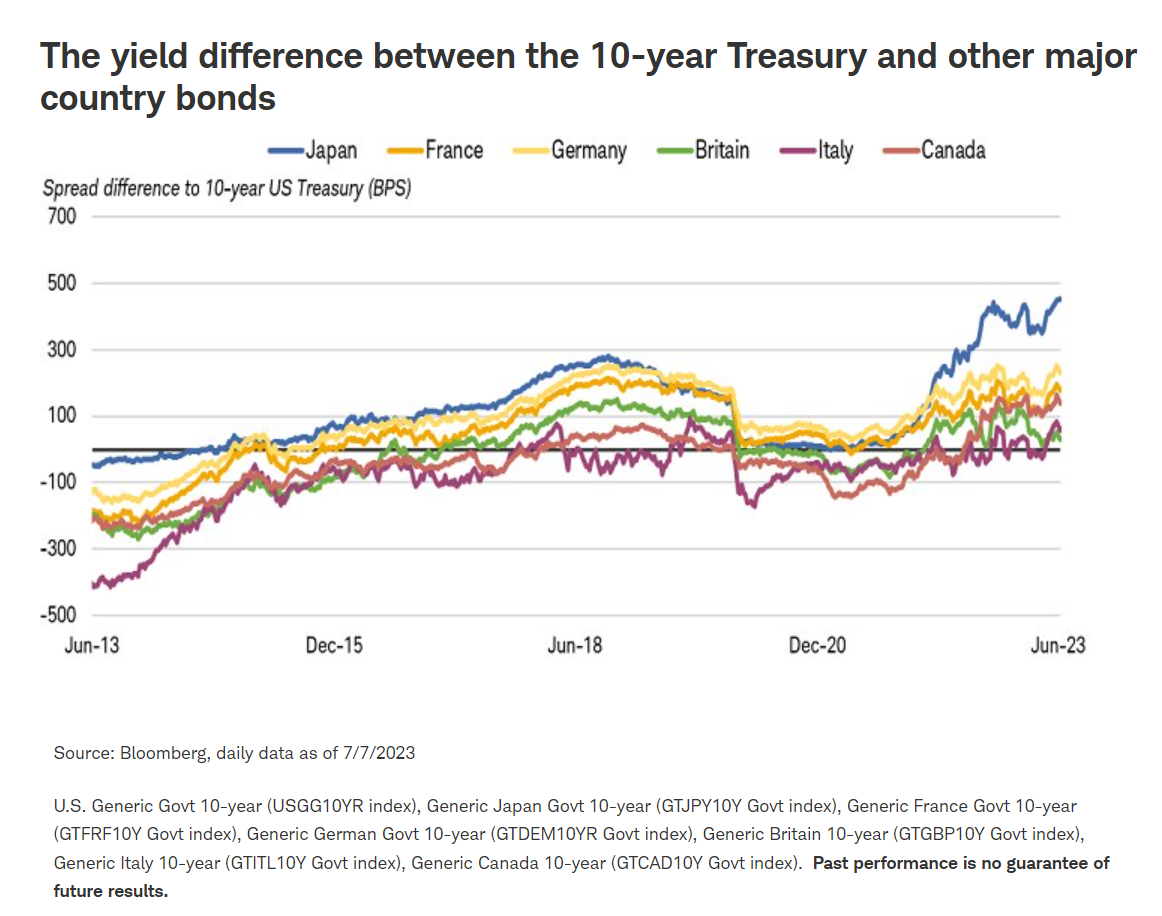

4. International bonds are not likely to provide much diversification. The Fed isn't the only central bank hiking rates, but it has been moving them up rapidly. Consequently, the interest rate differential between U.S. bond yields and those in other major developed countries has widened in favor of holding U.S. bonds, and the correlation in returns has increased.

Emerging-market (EM) bonds may outperform due to higher yields, but EM economies are more exposed to a potential downturn in global growth and tend to be much more volatile than developed market bonds.

5. Real interest rates are likely to rise further. As the Federal Reserve holds or increases interest rates, bond yields adjusted for inflation expectations are likely to continue to move higher. Treasury real yields for all maturities are already at the highest level since 2008, reflecting the Fed's tightening moves to date.

With inflation in a downtrend, real rates should remain high or potentially move higher. That is the Fed's main tool for cooling off the economy. It also raises the risk of a recession and could strain liquidity in the financial system.

Portfolio positioning in a higher-rate environment

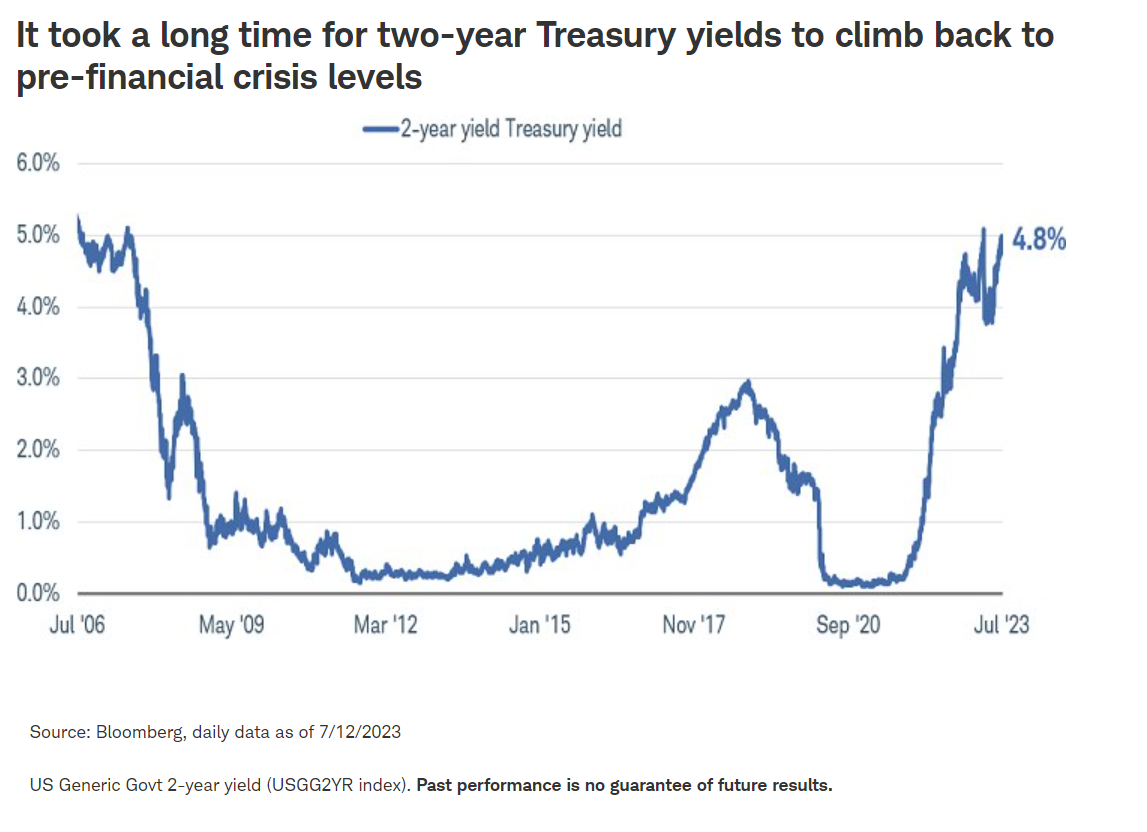

Now that short-term Treasury yields have reached 5%, further upside is likely to be limited. Although the economy has remained resilient in the face of the most rapid pace of rate increases since the late 1970s, inflation is cooling. Moreover, the Fed is likely near the end of its rate-hiking cycle, which would allow intermediate- to long-term yields to move lower over the next year. Ten-year Treasury yields have tended to peak within about six months of the peak in the fed funds rate in past cycles. If that pattern holds, then current yields may be near their highs.

For investors, current yields present an opportunity to extend the average duration in portfolios and lock in the highest yields in a decade for long-term cash flows. However, given the risk that the Fed overdoes its tightening and tips the economy into recession, higher-credit-quality bonds—like investment-grade corporate and municipal bonds—look more attractive than lower-rated bonds. In addition, Treasury Inflation Protected Securities (TIPS) provide an opportunity to lock in positive real yields and mitigate the impact of inflation.

Heightened volatility is likely to continue to be a feature of the higher-interest-rate environment. A laddered portfolio of high quality, diversified bonds that helps take some of the risk out of market timing can be a good way to manage through the rest of this interest-rate cycle.

1 A basis point is one-hundredth of 1 percentage point, or 0.01%, so 25 basis points would be equal to 0.25%.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions. Data herein is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

International investments are subject to additional risks such as currency fluctuation, geopolitical risk and the potential for illiquid markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. As compared to other fixed income products and strategies, engaging in a bond ladder strategy may potentially result in future reinvestment at lower interest rates and may necessitate higher minimum investments to maintain cost-effectiveness. Evaluate whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third-parties and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

This information does not constitute and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax advisor, CPA, financial planner, or investment manager.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All