In a unanimous decision, Federal Reserve policymakers raised the federal funds rate to 5.5%, the highest point since 2001.

As expected, the Federal Reserve raised the target range for the federal funds rate by 25 basis points, or a quarter percent, to 5.25% to 5.50%. It was a unanimous decision. The upper bound of the range now stands at the highest level since 2001. In addition, the Fed will continue to reduce its balance sheet (quantitative tightening) by allowing up to $95 billion per month in bonds to mature without reinvestment.

Statement was left nearly unchanged

The Federal Open Market Committee (FOMC) made few modifications to its statement, except to upgrade its description of growth to "moderate" from "modest." However, it did retain the language that indicated job gains remain "robust" and inflation "elevated," even though inflation has fallen substantially over the past few months.

More importantly, it dropped any allusion to pausing rate hikes in the near term, noting only that the committee will consider the cumulative tightening and the lag time between a change in policy and its effect on the economy and any new financial developments in setting policy.

Are we there yet?

The big question facing the markets is: Does this hike represent the peak in the fed funds rate for the cycle, or are there more rate hikes ahead? That question remains unanswered. After the last FOMC meeting in June, Federal Reserve Chair Jerome Powell indicated that the committee believed it was "near its destination." Based on his comments after this meeting, the Fed doesn't seem clear on how far away it is from reaching its goal but does believe policy is currently "restrictive," or tight enough to slow growth and inflation. Nonetheless, Powell indicated that the Fed was prepared to be "patient and resolute" in reaching its inflation goal.

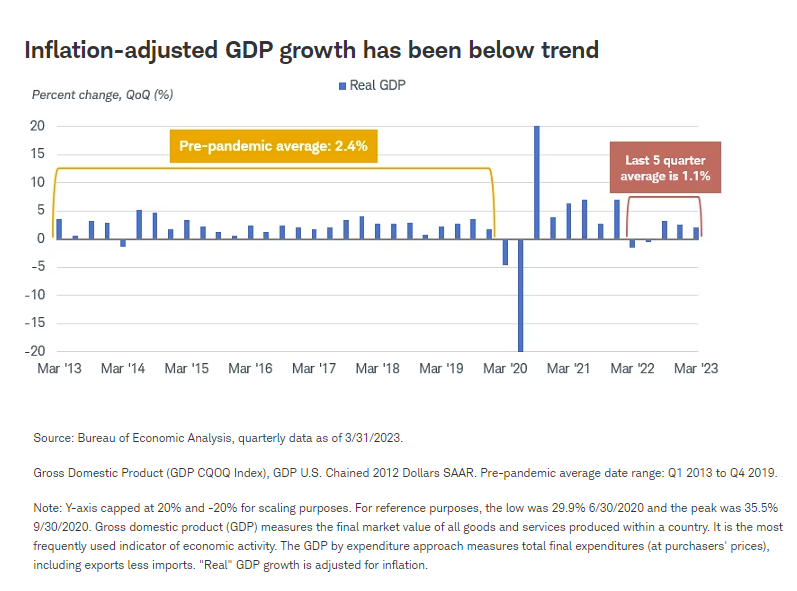

With the Fed data-dependent, we believe the key metrics to watch for signs that inflation is coming under control are economic growth and inflation. Powell repeated previous comments that the Fed is looking for a softer labor market and below-trend growth over a period of time. Notably, gross domestic product (GDP) growth since the Fed signaled policy tightening has averaged 1.1%, compared with a pre-pandemic average of 2.4%. However, GDP growth recently has rebounded after a few quarters of negative growth, which may have lowered the Fed's confidence about a further drop in inflation.

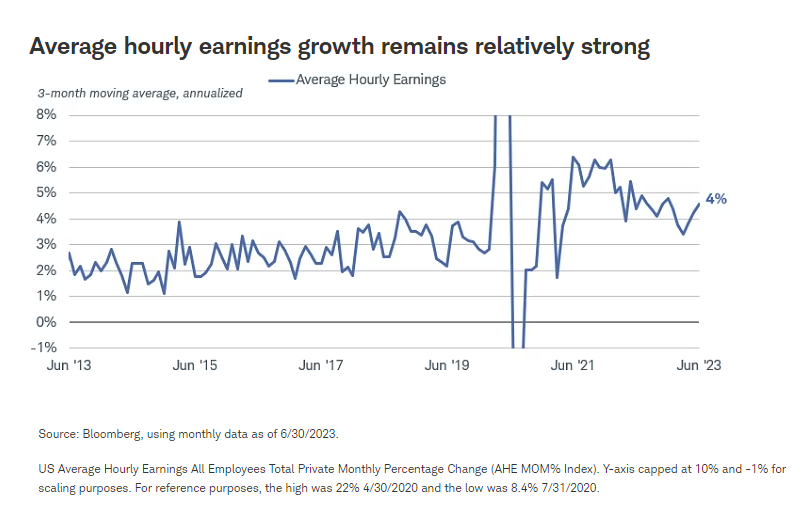

The labor market has shown signs of cooling, with job and wage growth decelerating, but apparently not enough for the Fed to be confident that policy is restrictive enough to get to 2% inflation down the road. Most likely the Fed would like to see those wage gains in the 3% region, rather than the current pace of more than 4%.

Yields fluctuated following the statement's release and into the press conference. The yield curve remains inverted, continuing the trend over the past year.

On to the September meeting

With an open-ended outlook from the Fed, the markets are likely to focus on the July employment report and the upcoming 2Q Employment Cost Index report (ECI), along with GDP growth as drivers of inflation until the September meeting. In the meantime, the annual Kansas City Federal Reserve meeting in Jackson Hole, Wyo., in August may provide some indications of which way the committee is leaning in setting policy.

For now, we look for the uncertainty about Fed policy to contribute to elevated volatility. Longer term, we continue to believe that the peak in the rate-hiking cycle is near and that yields will decline over the long run, but there is still a bumpy road ahead.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions. Data herein is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium was the biggest virtual event of the summer. Register here for the replay link to learn from the experts and thought leaders who participated in the event.

© Charles Schwab

Read more commentaries by Charles Schwab