The Federal Reserve left the target for its policy rate, the federal funds rate, in the 5.25% to 5.5% range at its latest meeting. However, it did revise up its projections for gross domestic product (GDP) growth and core inflation for this year, and reduced its projections for the pace of rate cuts over the next two years. The result is that the Fed is still expecting a cumulative 75 basis points (0.75%) in rate cuts in 2024, but a slower path of rate cuts in 2025 and 2026. In addition, it signaled that the federal funds rate may not fall to 2.5% in the longer run as previously expected.

The seemingly contradictory signals from the Fed reflect its effort to strike a balance between a relatively strong economy and inflation that is falling more slowly than last year, against a policy rate that is high and could potentially harm the economy. Fed Chair Jerome Powell indicated that the process of getting back to a "neutral rate," one that keeps the economy growing without generating inflation, is likely to be bumpy. To be consistent with the driving metaphor, our interpretation of the message from the Fed is that the direction of travel is lower for interest rates, but the pace and final destination are not clear.

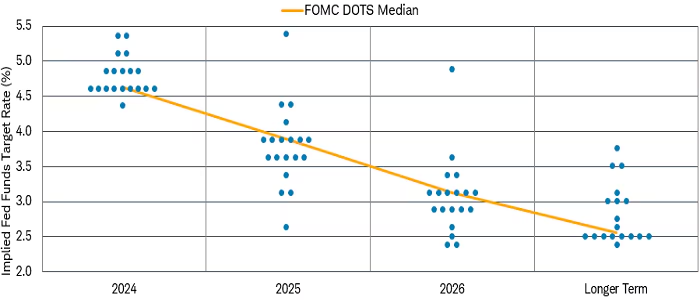

Dot plot signals a slower path of rate cuts

The Federal Open Market Committee's (FOMC) dot plot—which depicts each Fed member's estimate of where the federal funds rate will be in the next few years and the longer run—showed modest changes. The median estimate still shows an expectation of three rate cuts of 25 basis points each in 2024. However, the median estimate for the number of cuts in 2025 declined from 100 basis points to 75, suggesting the cycle could be slower over the next few years.

The FOMC's dot plot as of March 20, 2024

Source: Bloomberg, Federal Reserve, 3/20/2024

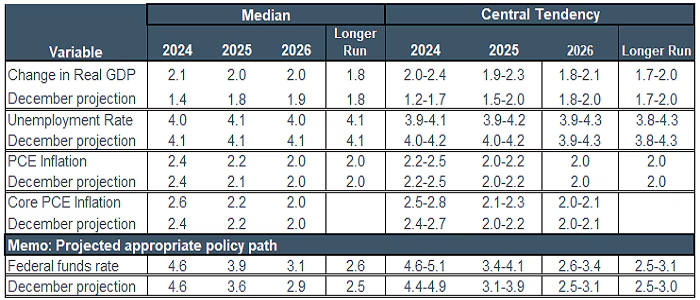

In the Summary of Economic Projections (SEP) the Fed revised its estimates higher for GDP growth and inflation in 2024. Those changes simply bring the estimates up to date with recent data. The more interesting change is that estimates for GDP growth were also revised higher for the next few years. While the degree of change was small, it suggests that the Fed is coming around to the view that the potential growth rate in the economy may be stronger than it was pre-pandemic. If the economy can grow at a stronger pace without generating inflation due to higher productivity, as has been the case recently, it would explain why some members of the committee upgraded their terminal rate estimates to 3% from the 2.75% area, raising the median "longer run" projection modestly to 2.6% from 2.5% in December. While the revision to the median projection was small, there were seven members indicating a 3% terminal rate compared to just four at the December 2023 meeting.

Economic projections of Federal Reserve board members and Federal Reserve bank presidents

Source: Federal Reserve Board, 3/20/2024.

For each period, the median is the middle projection when the projections are arranged from lowest to highest. When the number of projections is even, the median is the average of the two middle projections. The central tendency excludes the three highest and three lowest projections for each variable in each year. The range for a variable in a given year includes all participants' projections, from lowest to highest, for that variable in that year. Longer Run projections for Core PCE are not collected.

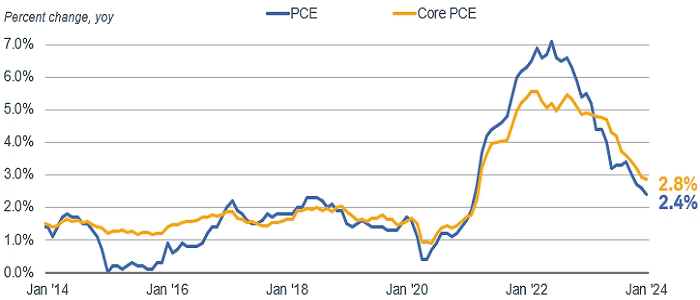

Overall, the message from the Fed suggests that the direction of travel for interest rates is lower as the committee still sees rate cuts ahead, but the pace may be somewhat slower than previously expected, and the final destination may be slightly higher. We still expect rate cuts to begin mid-year, most likely in June as long as the trend in inflation continues to move lower. Powell did emphasize that inflation has fallen significantly from its peak, which should warrant lower interest rates down the road. As long as that's the case, then there is plenty of room for the Fed to ease policy.

Inflation has fallen from its peak

Source: Bloomberg, monthly data as of 1/31/2024.

PCE: Personal Consumption Expenditures Price Index (PCE DEFY Index), Core PCE: Personal Consumption Expenditures: All Items Less Food & Energy (PCE CYOY Index), percent change, year over year. Personal Consumption Expenditures (PCE) is a measure of consumer spending. Core PCE excludes food and energy prices, which tend to be more volatile.

In the post-meeting press conference Powell indicated that the path of policy rates will likely be a "bumpy ride" given the uncertainties facing the economy. Nonetheless, markets reacted positively because the signal is still that the Fed is poised to cut interest rates this year and over the next few years.

For investors, we continue to suggest gradually extending duration in fixed income to avoid reinvestment risk while staying in higher-credit-quality bonds.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab