Emerging-Market Bonds: Are Returns Worth the Risk?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEmerging-market local-currency bonds have rallied sharply since last October, along with other risky segments of the global bond market. With global economic growth stable or improving, inflation pressures easing, and central banks cutting interest rates or approaching rate cuts, there is room for the trend to continue.

In a benign economic environment, investors are often willing to stretch into riskier segments of the bond market in search of higher yields. However, emerging-market (EM) local-currency bonds typically are more volatile and carry higher risks than developed market bonds. Navigating the market can be challenging, and many investors may prefer to use funds or other professional management strategies when investing.

What are local-currency EM bonds?

The EM local-currency bond universe is diverse and changes over time. It contains bonds issued by governments and government agencies, as well as corporations in their home currencies. There are two broad types: bonds denominated in U.S. dollars, euros, or currencies of other major developed countries—also known as "hard-currency" bonds—and "local-currency" bonds, which are denominated in the issuer's home currency. Yields on hard-currency EM bonds tend to be higher than on local-currency bonds because some lower-rated issuers aren't able to find buyers for their home-currency debt due to a history of depreciation and/or default. Local-currency bonds typically offer somewhat higher yields, offered by somewhat less-risky issuers. Yields reflect the rates set by the issuers' central banks. All else being equal, policy rates tend to be higher in emerging-market countries than in developed markets.

There are different indices that track these markets. If you are buying a fund or index-tracking exchange-traded fund (ETF), it's important to know what's in the underlying index because there can be large variations in yields, duration, and risks, and those differences can affect the return of the investment. In our view, the risk/reward in the hard-currency EM group doesn't look especially attractive. Yields are relatively low compared with developed market yields.

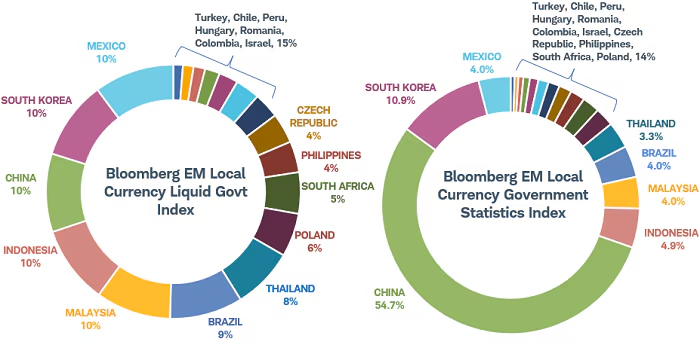

We see greater opportunity in the local-currency segment of the market. We are using the Bloomberg Emerging Markets Local Currency Liquid Government Index for this article. It represents government bonds issued by countries that are deemed EM by either the World Bank or International Monetary Fund. The index limits exposure to any one country to 10%. It does not include corporate debt, and is unhedged. The current makeup of the index represents bonds from 18 countries, with four countries near the 10% cap.

Note that we favor these types of indexes because they cap exposure to any one country's bonds. As the chart below illustrates, without those caps, it can be harder to get a diversified portfolio. For example, a country like China is a large issuer in this category and can end up dominating an index.

Source: Bloomberg EM Local Currency Liquid Govt Index Total Return Index Unhedged USD (BECLTRUU Index) and Bloomberg EM Local Currency Government Statistics Index (I20344 Index). Data as of 4/1/2024.

Total return includes interest, capital gains, dividends, and distributions realized over a period.

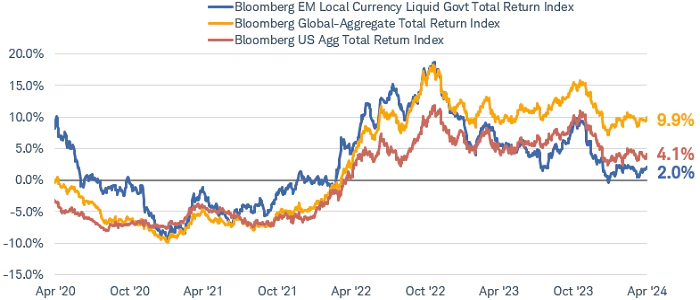

The cumulative total return of the EM local-currency index has outperformed both the Global Aggregate Bond Index and the US Aggregate Index since last fall.

Source: Bloomberg EM Local Currency Liquid Govt Index Total Return Index (BELTRUU Index), Bloomberg Global-Aggregate Total Return Index (LEGATRUU Index), Bloomberg US Agg Total Return Index (LBUSTRUU Index). Daily data as of 4/1/2024.

Total return includes interest, capital gains, dividends, and distributions realized over a period. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

As the chart illustrates, returns can be volatile due to fluctuations in interest rates, currency values, inflation expectations, and political developments. However, for investors with a higher risk tolerance, we believe local-currency EM bonds could deliver attractive returns over the next year. In the past, performance has been strongest during periods of positive global economic growth, easing monetary policies among major central banks, and falling inflation. Those conditions appear likely to materialize over the next year.

We expect most major central banks, led by the U.S. Federal Reserve, to begin cutting their policy rates later in the year as inflation pressures continue to ease. Meanwhile, global economic growth appears likely to improve from its relatively sluggish pace of the past year. EM countries, which are often major exporters that benefit most from an upturn in global economic activity and trade, have tended to benefit from those conditions in the past.

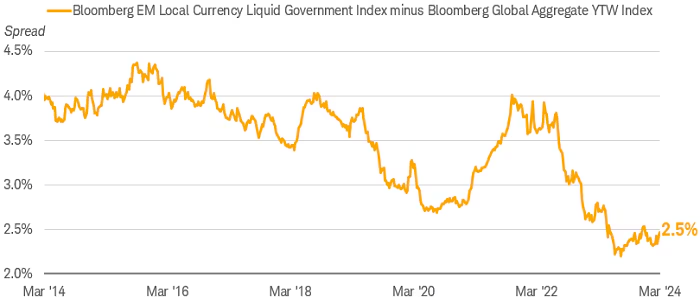

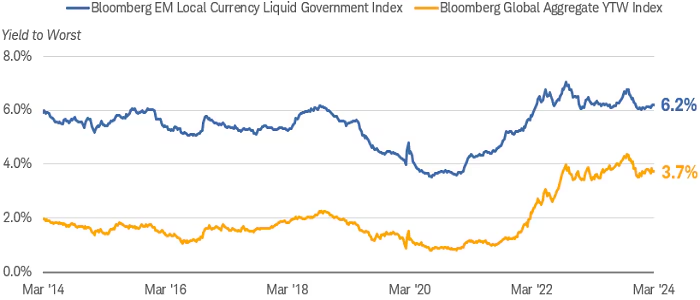

Moreover, several EM central banks have already started cutting interest rates, raising the prices of their bonds—which move inversely to yields—due to falling inflation after the supply-side shocks of the past few years. With a yield-to-worst of 6.2%, the index's average yield has fallen by about 60 basis points (or 0.6%) from its recent peak, but it's well above the 3.74% yield of the Bloomberg Global Aggregate Bond Index. Moreover, the average duration of the EM index is 5.4 years compared to the Global Agg's duration of 6.6 years, making it somewhat less sensitive to interest rate changes.

The spread between the EM local currency index and the global Agg has fallen

Source: Bloomberg.

Bloomberg EM Local Currency Liquid Government Index (I26751 Index) and Bloomberg Global Aggregate Yield to Worst (LEGAYW Index). Weekly data as of 3/29/2024. Yield to worst is a measure of the lowest possible yield that can be received on a bond with an early retirement provision. Past performance is no guarantee of future results.

Source: Bloomberg.

Bloomberg EM Local Currency Liquid Government Index (I26751 Index) and Bloomberg Global Aggregate Yield to Worst (LEGAYW Index). Weekly data as of 3/29/2024. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

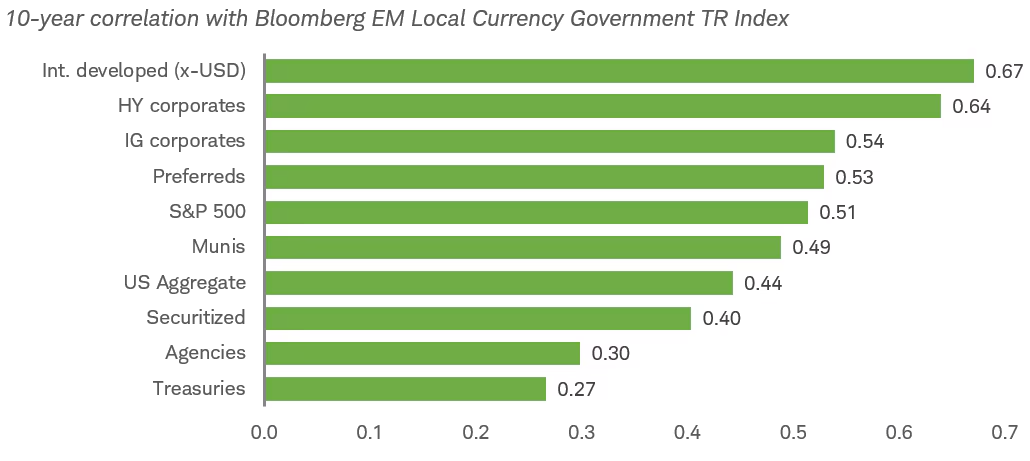

EM local-currency debt can be a good source of diversification within a fixed income portfolio. Returns tend to have a low correlation with U.S. Treasuries. However, they do have somewhat higher correlations with developed market bonds, corporate bonds, and U.S. equities. Default is also a risk and something that should be considered when investing in EM bonds. Consequently, it makes sense to limit exposure to a relatively small portion of a portfolio.

Correlations vary

Source: Bloomberg, 3/31/2014 to 3/29/2024.

Indexes representing the investment types are, Bloomberg Global Aggregate ex-USD Total Return Index Value Unhedged USD (LG38TRUU Index) = Int. developed (x-USD), Bloomberg VLI: High Yield Total Return Index Value Unhedged USD (LHVLTRUU Index) = HY corporates, Bloomberg US Corporate Total Return Value Unhedged USD (LUACTRUU Index) = IG corporates, ICE BofA Fixed Rate Preferred Securities Index (P0P1 Index) = Preferreds, S&P 500 Total Return Index (SPXT Index) = S&P 500, Bloomberg Municipal Bond Index Total Return Index Value Unhedged USD (LMBITR Index) = Munis, Bloomberg US Agg Total Return Value Unhedged USD (LBUSTRUU Index) = US Aggregate, Bloomberg U.S. Securitized: MBS/ABS/CMBS and Covered TR Index Value Unh (LD19TRUU Index) = Securitized, Bloomberg US Agg Agency Total Return Value Unhedged USD (LUAATRUU Index) = Agencies, Bloomberg US Treasury Total Return Unhedged USD (LUATTRUU Index) = Treasuries. Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated. Correlations shown represent the 10-year correlation of each asset class with the Bloomberg EM Local Currency Government TR Index (EMLCTRUU Index), using weekly data, between 3/31/2014 to 3/29/2024.

The role of currencies

One of the biggest drivers and risks for EM local-currency bonds is the movement in the dollar. After more than a decade of appreciation, the U.S. dollar's strength has entered a more stable phase. Ever since the Federal Reserve indicated its rate-hiking cycle has ended, the dollar has shown limited movement against most EM currencies. The prospect of a stable-to-weaker dollar makes holding EM currency bonds more attractive, as it reduces the potential for currency losses to offset the yield advantage. A strong dollar, especially if it's driven by a negative shock that causes a flight to safety, such as during the pandemic in 2020, would be a major negative factor for these bonds.

The dollar has been relatively stable in recent years

Source: Federal Reserve Bank of St. Louis.

Nominal Emerging Market Economies U.S. Dollar Index, Jan 2006=100, Daily, Not Seasonally Adjusted (DTWEXEMEGS). Daily data as of 3/29/2024.

The Nominal Emerging Market Economies U.S. Dollar Index is a weighted average of the foreign exchange value of the U.S. dollar against a subset of the broad index currencies that are emerging market economies. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly.

Consider EM bonds carefully

Among the opportunities in the fixed income markets in 2024, local-currency EM bonds may be one to consider for investors with a higher risk tolerance. The relatively high yields and likelihood of rate cuts by global central banks have created a tactical investment opportunity. In addition to high yields, EM local-currency bonds can provide diversification and the potential for capital gains. However, the risks in this asset class tend to be high, so the amount of money allocated should be limited.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

About the Author

Kathy Jones is responsible for interest rate and currency analysis as well as fixed income education for Schwab clients and the public.

Prior to joining Schwab in 2011, Kathy was a fixed income strategist at Morgan Stanley, where she specialized in global macro strategy covering domestic and international bonds and foreign exchange. She has also been a consultant in the alternative investment area and previously served as executive vice president of the Debt Capital Markets division of Prudential Securities.

Kathy has analyzed global bond, foreign currency, and commodity markets extensively throughout her career as an investment analyst and strategist, working with both institutional and retail clients. She makes regular broadcast appearances on Bloomberg TV, Yahoo Finance, and CNBC, and is often quoted by The Wall Street Journal, The New York Times, Financial Times, and Reuters. She holds an MBA in Finance from the Kellogg Graduate School of Management at Northwestern University, and a B.A. with honors in English Literature from Northwestern University.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in declining market.

Currencies are speculative, very volatile and are not suitable for all investors.

Supporting documentation for any claims or statistical information is available upon request.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0424-V6PK

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All