As expected, the Federal Reserve kept the target range for the federal funds rate at 5.25% to 5.50% at the May meeting of the Federal Open Market Committee (FOMC). Citing recent elevated inflation readings, the statement accompanying the announcement indicated that FOMC members consider it too early for rate cuts. Meanwhile, the Fed is planning to "taper" its quantitative tightening program in June by reducing the dollar amount of Treasuries it allows to mature without reinvestment.

Sticky inflation is a risk

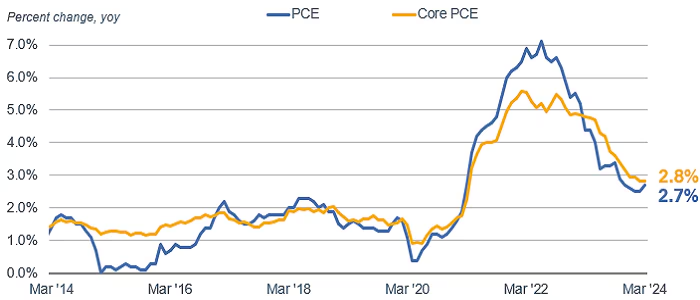

There were a few notable changes to the Fed's statement from the previous meeting. A sentence was added acknowledging "lack of progress" on inflation in "recent months." That stickiness in inflation in the first quarter of this year is likely to keep Fed policy on hold until later in the year. The committee needs to see a resumption in the decline in inflation to feel confident enough to cut rates.

Inflation has fallen from its peak

Source: Bloomberg, monthly data as of 3/31/2024.

PCE: Personal Consumption Expenditures Price Index (PCE DEFY Index), Core PCE: Personal Consumption Expenditures: All Items Less Food & Energy (PCE CYOY Index), percent change, year over year. Personal Consumption Expenditures (PCE) is a measure of consumer spending. Core PCE excludes food and energy prices, which tend to be more volatile.

The Fed's view of the economy is nearly unchanged, with the statement noting that the pace of economic growth is solid and job gains have been strong. However, Fed officials changed the wording describing progress toward balancing its two mandates—inflation and full employment—into the past tense. It noted that the risks to achieving its dual mandate of full employment and low inflation "have moved toward better balance over the past year" instead of "are moving." That might seem like a minor change, but it highlights how much the recent stalling in inflation's drop is seen as a risk for Fed policy.

Tapering quantitative tightening

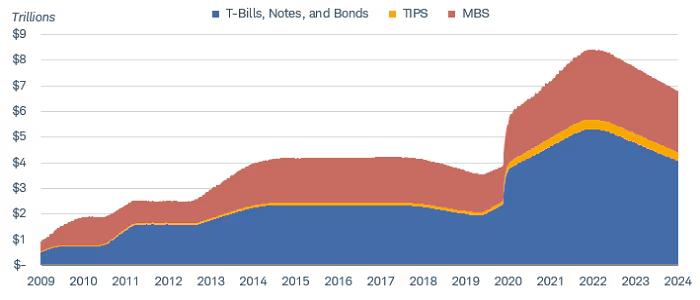

The Fed also announced that it is going to slow down the pace of balance sheet reduction. Quantitative tightening is the process where the Fed allows bonds held on its balance sheet to mature without reinvesting the principal. The Fed will reduce the cap on maturing Treasuries from $60 billion per month to $25 billion. The cap on mortgage-backed securities will stay the same at $35 billion, but proceeds of maturing bonds will be reinvested into Treasuries.

The announcement is not a big surprise, as the Fed had signaled it was reviewing the program and would likely slow it down due to concerns about the need to maintain liquidity in the financial system. It isn't likely to have much impact on the market. The Fed's caps were not reached most months during the program. Even with tapering the pace, the Fed's balance sheet should continue to fall. It isn't seen as a policy move, but rather a way to address liquidity concerns.

The Fed's balance sheet

Source: Bloomberg, weekly data as of 5/1/2024.

Reserve Balance Wednesday Close for Treasury Bills, Treasury Notes, Treasury Bonds, Treasury Inflation Protected Securities, and Mortgage-Backed Securities.

In the post-meeting press conference, Fed Chair Jerome Powell addressed a few questions that have weighed on the bond market. He indicated that the committee does believe policy is "restrictive" at current levels despite the ongoing resilience in the economy. He also said that he didn't expect that the next move would be a rate hike. It hasn't been ruled out, but he indicated it isn't likely.

Overall, the Fed's policy remains on hold. Powell described the Fed's stance as "patient." We still believe there is a potential for rate cuts in the second half of the year. However, the outlook depends on inflation resuming its declining trend. For now, the Fed's policy will continue to be one of "higher for longer," but the overall plan to reduce rates longer term is still intact.

The immediate reaction in the markets was a rally in bond prices. Treasury yields fell for all maturities. Markets had been concerned that the Fed might rule out rate cuts this year or even signal a potential rate hike. However, the message was consistent with the potential for one to two cuts of 25 basis points (or 0.25%) each in the federal funds rate in 2024.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation. Treasury Inflation-Protected Securities are guaranteed by the US Government, but inflation-protected bond funds do not provide such a guarantee.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes than other fixed income investments. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0524-0EUA

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Charles Schwab

Read more commentaries by Charles Schwab