The academic evidence shows that selecting investments, such as mutual funds or stocks, based on past performance is a terrible idea. Use our premium membership service to forward this article to clients with your logo.

Watch replays for CE credit. We recap the webinars presented at our Market Outlook Summit.

I discuss cultural and technical challenges and ideas that will lead to a successful client relationship when working with this group of great clients.

Watching hundreds of YouTube cooking videos revealed to me the secret to successfully managing your advisory firm.

Last week we looked at four "stinking thinking" cognitive biases that contribute to poor investment decisions. Here are six more.

Recently one of our best advisors gave notice. He said we don’t “value youth.”

While putting together a marketing plan is more complex than reading an article, here are three important pieces of advice to get female solo practitioners started.

I want to show you how to establish a system for getting client tax returns each year.

Here are the nine steps you need to take when entering a new niche market.

The prime targets for bad actors are companies buying others since they have the money and deep pockets.

Consider the upfront bonus checks often paid to advisors leaving one broker/dealer to join another. That “bonus” is not a bonus at all.

Last month, the Federal Reserve kicked off a campaign to increase interest rates to bring down the highest inflation the U.S. has experienced since the 1980s. Critics contend the Fed still isn’t doing enough, and the central bank seems to agree. Several high-ranking Fed officials, including Chair Jerome Powell, have said in recent days that interest rates may need to rise faster, and possibly higher, than initially planned.

Poor-performing chief executives can sleep a little easier. Bill Ackman, one of the world’s best-known investors, has all but ruled out future activist campaigns in favor of a lower-key approach to influencing portfolio companies. That’s a commendable investment stance. But efficient capital markets still need the odd rabble rouser.

The U.S. Commerce Department announced on Thursday that consumer spending fell 0.4% in February from January after adjusting for inflation. This may not seem like much, but real spending has dropped in three of the last four months. Without strength in household outlays, the economic expansion is doomed.

While most of the world watches in horror as Vladimir Putin advances his military invasion of Ukraine, Russia’s congruent foray into Bitcoin, gold-linked rubles and central bank digital currencies is triggering a conflicted response from financial technology and crypto enthusiasts.

A closer look at the LooksRare platform that has quickly become the leading NFT marketplace by trading volume shows that most of the activity is actually users selling tokens to themselves to help earn rewards in the form of more coins.

The good news is that after months of internal debate, the Securities and Exchange Commission has finally proposed rules mandating that publicly traded corporations address climate change.

As quarters go, this was one for the record books. Taking three months, or a calendar year, to have any particular significance makes no sense, but it’s difficult to quell it. So, here is an attempt to summarize what’s changed in the last three months from the point of view of markets.

Federal Reserve Chair Jerome Powell and his colleagues are on the march to return ultra-loose monetary policy and accommodative financial conditions to more normal levels. The trouble is, their destination is uncertain and the terrain may be shifting as they forge forward with higher interest rates.

Banks are gearing up to offload billions of dollars in junk debt backing leveraged buyouts, counting on the nascent stability in the market to finally get rid of underwrites for businesses such as Wm Morrison Supermarkets Plc and Unilever Plc’s tea unit.

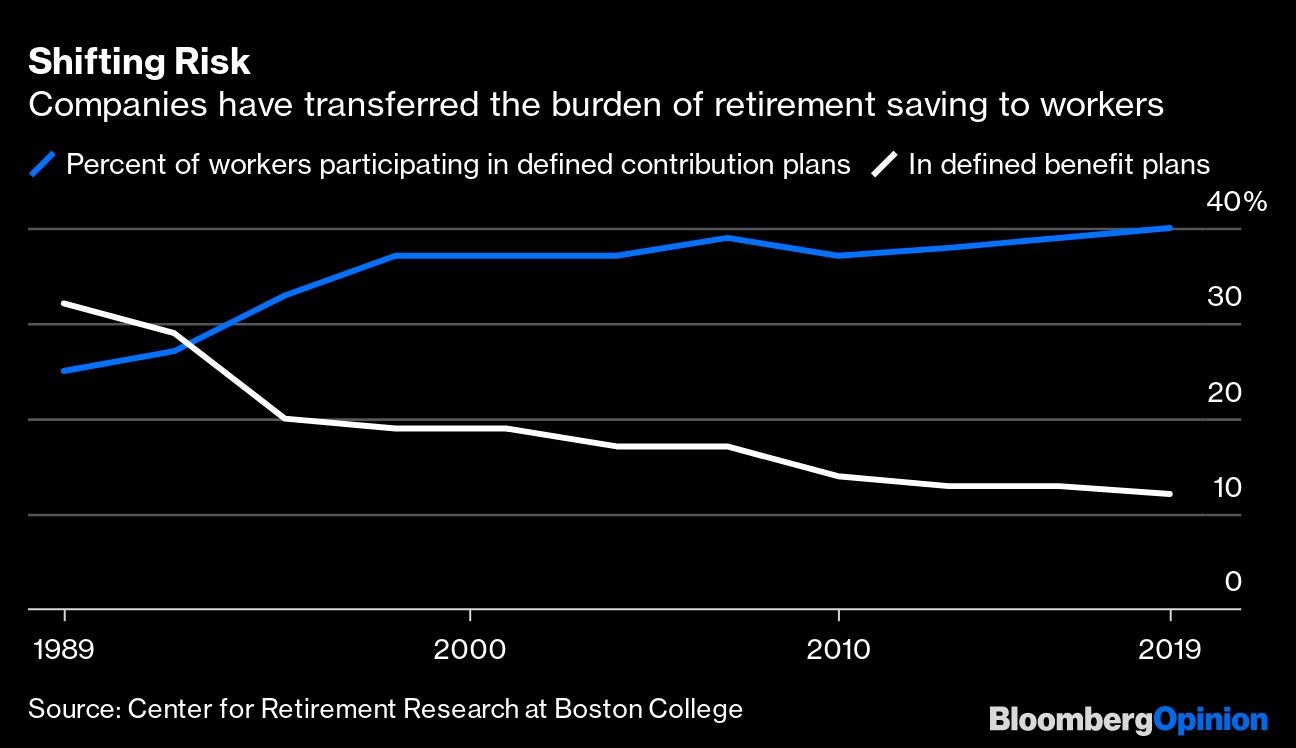

The U.S. government has long offered myriad contrivances and enticements to get Americans to save enough for a comfortable retirement — so far with woefully inadequate results. But why should it be involved at all? Why can’t people be responsible enough to prepare for an entirely foreseeable event?

For more than a quarter century, the U.S. government has been sending an unmistakable message to poor, single mothers: Get married. If America genuinely wants to address poverty and achieve gender equality, this has to change.

Twitter shares surged as much as 26% after Musk’s purchase was revealed Monday in a regulatory filing, the stock’s biggest intraday increase in more than four years. The stake is worth about $2.89 billion, based on Friday’s market close.

Do the investment products that advertise themselves as ESG-compliant actually deliver?

According to LIMRA, RILA sales for the first half of 2021 were 105% higher than the same period in 2020. What’s behind the popularity of this relatively new product?

The argument goes like this: A company’s value (and stock price) is driven by its ability to earn a profit and grow its business. Its dividend policy is irrelevant at best. In some cases, paying dividends could hurt the stock. Is it true? Let’s explore this idea further.

Reflecting on the history of our family office, our investing philosophy mirrors how previous generations built their wealth through farming. They patiently waited to harvest the crops they planted; we buy securities and patiently wait for them to appreciate.

The poor performance of factor-driven value strategies over the past decade has raised the question of whether intangible assets, such as patents and proprietary software, are properly treated. New research confirms that intangibles indeed distort valuation metrices, but there is no consensus on how to address the problem.

We are a service industry. Before we try to sell clients anything, we need to stop and consider what they want.

Managing your calendar can feel like a full-time job. Using an automated scheduling tool, such as Acuity Scheduling, Calendly, or OnceHub, is a must.

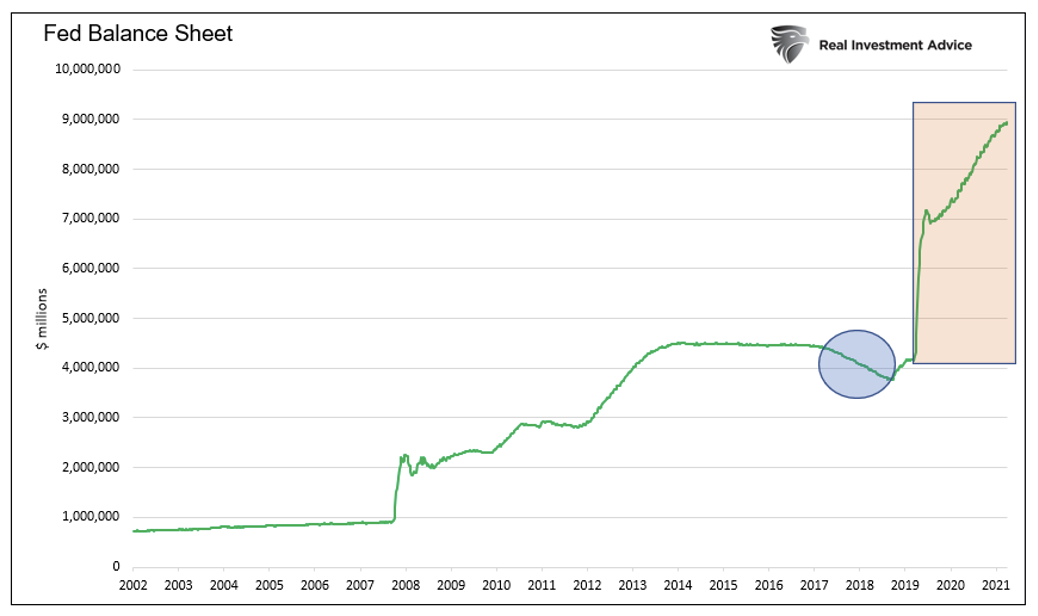

With QE finished and QT on the horizon, I answer a few questions to help you better appreciate what QT is, how it will operate, and discuss how draining liquidity will affect markets.

With the first quarter coming to a close, banks (mostly based in China) have helped coal companies raise $9.9 billion via loans and bond sales, according to data compiled by Bloomberg. For comparison, the number was closer to $4.4 billion during the first three months of 2021.

Add this to the pandemic lesson book: People may be willing to give up their homes in high-cost, densely packed coastal cities, but they still want their coastal lifestyles — just with a little more space, cheaper real estate and warmer weather.

Much of the commentary about the Ukraine war’s implications for the investment-management industry has tended to be both immediate and narrow, particularly in discussions about the spillovers for different segments. By zooming out, however, some longer-term ramifications become more apparent for both public and private markets.

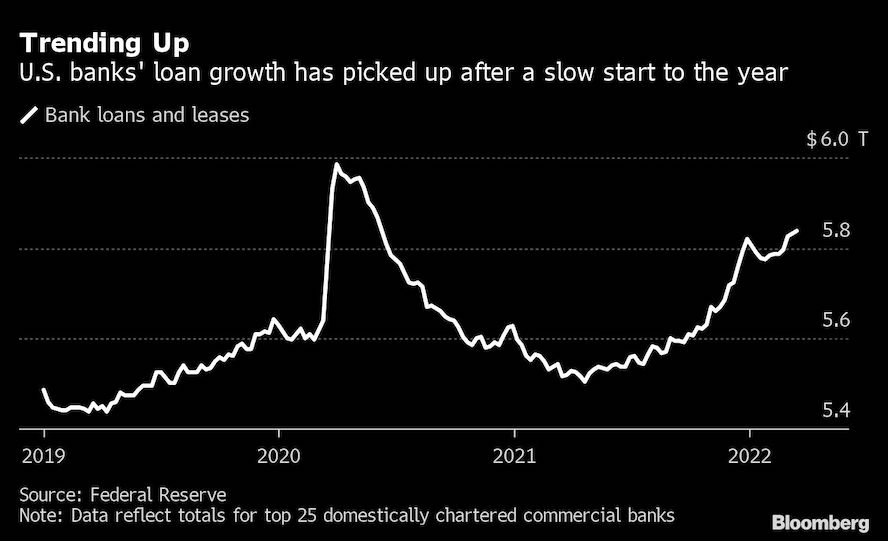

Loan growth at the largest U.S. banks is finally staging a comeback after being absent for much of the pandemic, but investors are eager for signs the rebound is strong enough to withstand rising interest rates and economic uncertainty following Russia’s invasion of Ukraine.

Volatility from Russia’s invasion of Ukraine, faster inflation and rising interest rates triggered the slowest quarter of U.S. initial public offerings in more than five years. At one point, the market ground to a complete halt, with longest period without an initial public offering since the Great Recession.

Purchases of goods and services, adjusted for changes in prices, fell 0.4% from the prior month, following a 2.1% jump in January, according to Commerce Department figures Thursday. The decline was due entirely to a decrease in spending on merchandise.

The pandemic has prompted a rethinking of many practices and routines of professional life, such as working from home, meetings and interviewing online. Now another such pastime is ripe for a reassessment: the face-to-face conference.

Investors in corporate bonds are bracing for more trouble after getting hammered by rampant inflation and rising yields in the first quarter.

The House overwhelmingly passed legislation that would expand the tax benefits for retirement accounts to bolster the savings of Americans, many of whom have nothing banked for after they stop working.

Things are never as good or as bad as they seem. That adage has generally served investors well. Ignoring the extremes of optimism and pessimism can spare equity buyers some painful mistakes — such as piling into tech stocks at the height of the dotcom boom — and may signal lucrative opportunities for the brave, such as during the depths of the 2008 global financial crisis.

It may be inconceivable to the moneyed class, but there are in fact very good reasons not to raise interest rates quickly or dramatically. Yes, inflation is worryingly high, Ukraine is burning and Covid-19 still threatens to upend supply chains. However, the reality many Americans face — if not low-income and middle-class workers across the globe — is quite different from what the stock market and go-to suite of economic indicators tell us.

It’s a question that faces every public company: Should corporate employees care about day-to-day stock fluctuations? Last week, Shopify Inc. CEO Tobi Lutke shared his perspective by tweeting that the “relationship between stock price and a public company is the same as the relationship between a pro sports team and betting markets. Sort of related, but irrelevant to the players on the field.”

Get out of stocks, according to Gary Shilling, who has gone to 30% cash in the portfolios he manages. The economy will be in recession by the end of the year, and stocks will fall in response.

I’m one of the 45 million foreign-born individuals who now call the U.S. home. I knew enough about budgeting, but struggled with financial decisions from day one, as this was a completely new system to me.

The insurance industry has struggled to build engagement with its customers. That is also true among financial advisors, who can apply the same tactics to grow their business.

No one is born a writer. It’s a skill to be learned and nourished. Unlike most skills that erode as we age, you can always improve your writing skills.

I’ll share some of the insights into how advisors can get the most value when they pay for training solutions..

ICYMI: In this roundup, we’re highlighting the five most popular pieces of content from the previous week.

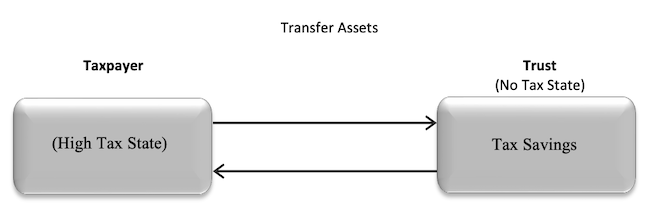

This article provides an overview of the benefits of using a Nevada Incomplete Non-Grantor Trust (NING) as part of a business sale to reduce or eliminate state income taxes and capital gains taxes.