The average size of a single-family house built in the 1960s was about 1,500 square feet, and homes within multifamily units were about 800 square feet. Now those figures are more than 2,000 square feet and more than 1,200 square feet, respectively.

Recently, Matthew Bartolini, global head of research strategists at State Street Investment Management, sat down with VettaFi to discuss where inflation stands, opportunities within portfolio construction, and much more.

Concerned about overfunding your 529 plan? Discover the strategic flexibility of modern 529 accounts. From tax-free Roth IRA transfers to building a multi-generational educational legacy, learn how to maximize your unused education savings for long-term wealth building.

Join the experts at Precidian Investments as they explore how to recognize, mitigate, and manage currency risk and how to better approach your international exposures.

We separate this article into two parts. Part one is the optimistic case: an AI-induced, productivity-led economic boom in which the benefits spread quickly to society. Part two will address a more bearish outlook: the possibility of a large gap in the distribution of AI's productivity benefits, accruing to corporations much more quickly than to employees.

The U.S. stock market is extremely expensive. In the past, stock markets have not remained expensive for long. Is it because of artificial intelligence? Perhaps, but a similar argument was made during the dot-com bubble.

Vanguard’s Total World Stock ETF (ticker VT) is an elegant product: a single fund that gives you cap-weighted exposure to the entire global equity market. For investors who want simplicity, it’s hard to beat. But is simplicity costing you money?

Put succinctly, the world today requires substantially more electricity than only a few years ago. AI, electrification, reshored manufacturing, and population growth in the developing world are converging into a demand curve that the existing global power system simply cannot meet.

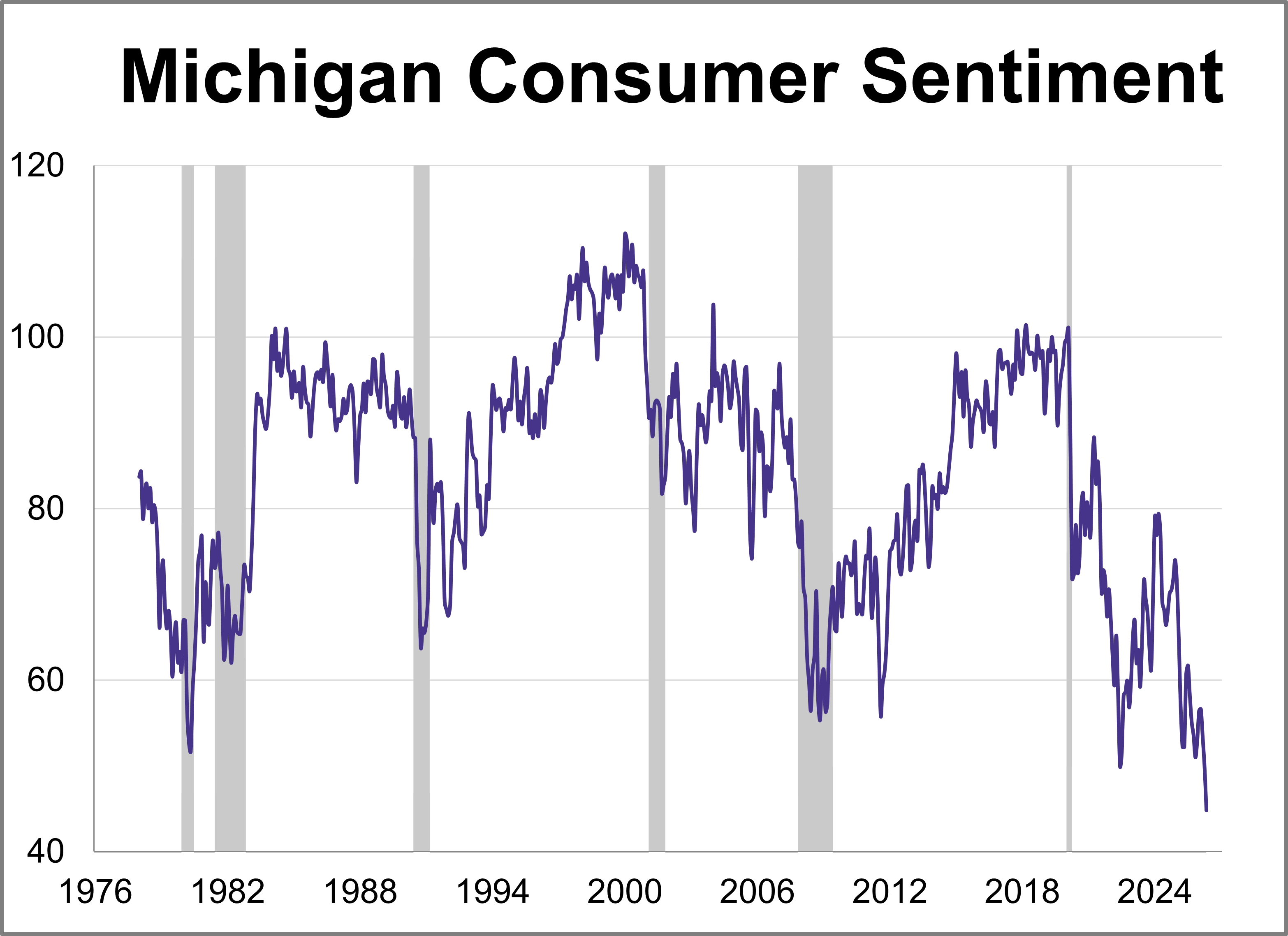

Consumer sentiment sank for a third straight month to another record low amid intense cost of living concerns and stubbornly high prices. The final May reading for the University of Michigan Consumer Sentiment Index came in at 44.8, marking a 5-point drop from April and falling well below the month's preliminary estimate of 48.2.

Private credit managers are increasingly turning to the once-unthinkable: Trading in and out of loans to dump troubled assets and hunt for bargains amid the industry’s first stress test after years of breakneck growth.

US stocks advanced as investors struck an upbeat tone ahead of a long holiday weekend, with optimism fueled by hopes for resolution of hostilities in the Middle East, resilient economic data and relentless enthusiasm for artificial intelligence-linked trades.

From the April payroll report released on May 8, we realize that not all industries are equally impacted by AI. Diagnostic imaging centers, an area where AI is thought to replace humans, have increased demand for workers, whereas bookkeeping demand has declined in recent years.

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

Hedge funds have been selling the scorching rally in US semiconductor stocks to book profits, while keeping their overall exposure to the AI theme, according to traders at Goldman Sachs Group Inc.

Equities advanced in April, but hedges remain few and far between, as traditional risk mitigants like bonds and gold continue to show a correlation with stocks.

Watching your children step into financial independence is one of the most rewarding and complex milestones families experience. As young adults begin earning income, managing expenses, and making major life decisions, the habits and financial knowledge they develop can shape their long-term success.

Even if armchair investors are fleeing private credit or panicking that their unlisted shares in Anthropic PBC are now invalid, the long-term trend is clear: Public markets keep losing ground to private funds.

Sustainable investing in fixed income has come of age. Against a backdrop of heightened geopolitical tensions, persistent economic and trade uncertainty, sustainable fixed income continued to demonstrate its appeal in 2025.

Stocks’ rally off the March 30 lows has been nothing short of wild, with internal market dynamics showing some performance divergences that we haven’t seen for decades. For example, in the first 6 weeks of the rally, the S&P 500 Growth index beat the S&P 500 Low Volatility Index by more than any other 6-week window on record.

At first glance, the retreat of foreign asset managers is ominous. Signs of a domestic retail frenzy are everywhere. Cash deposits in local brokerage accounts have reached 137 trillion won ($91 billion), a two-third jump from six months ago.

Emerging markets (EM) are using low-cost renewables to cut fuel imports, stabilize power costs and improve energy security—positioning EM as the growth engine of the energy transition. Countries and companies that leverage their dominance in critical minerals and green technology could pull ahead, creating dispersion in potential outcomes for investors.

Model portfolios are a key pillar for asset managers competing for advisor and investor attention. They offer straightforward, pre-packaged tools that help investors target and achieve specific financial goals. Designing and operating models, however, takes a particular set of skills. Goldman Sachs Asset Management recently made a big hire therein.

With mega tech AI capital expenditure projected to cross a staggering $660 billion to $750 billion, according to estimates from firms like Goldman Sachs, CreditSights and Bloomberg, saying the stakes are high for Nvidia and the AI ecosystem is an understatement. It’s no wonder we can focus on little else this week.

While most institutional investors recognize that private equity and public equity share similar economic risks, they often seem to ignore how their aggregate equity portfolio is affected by their substantial allocation to private equity.

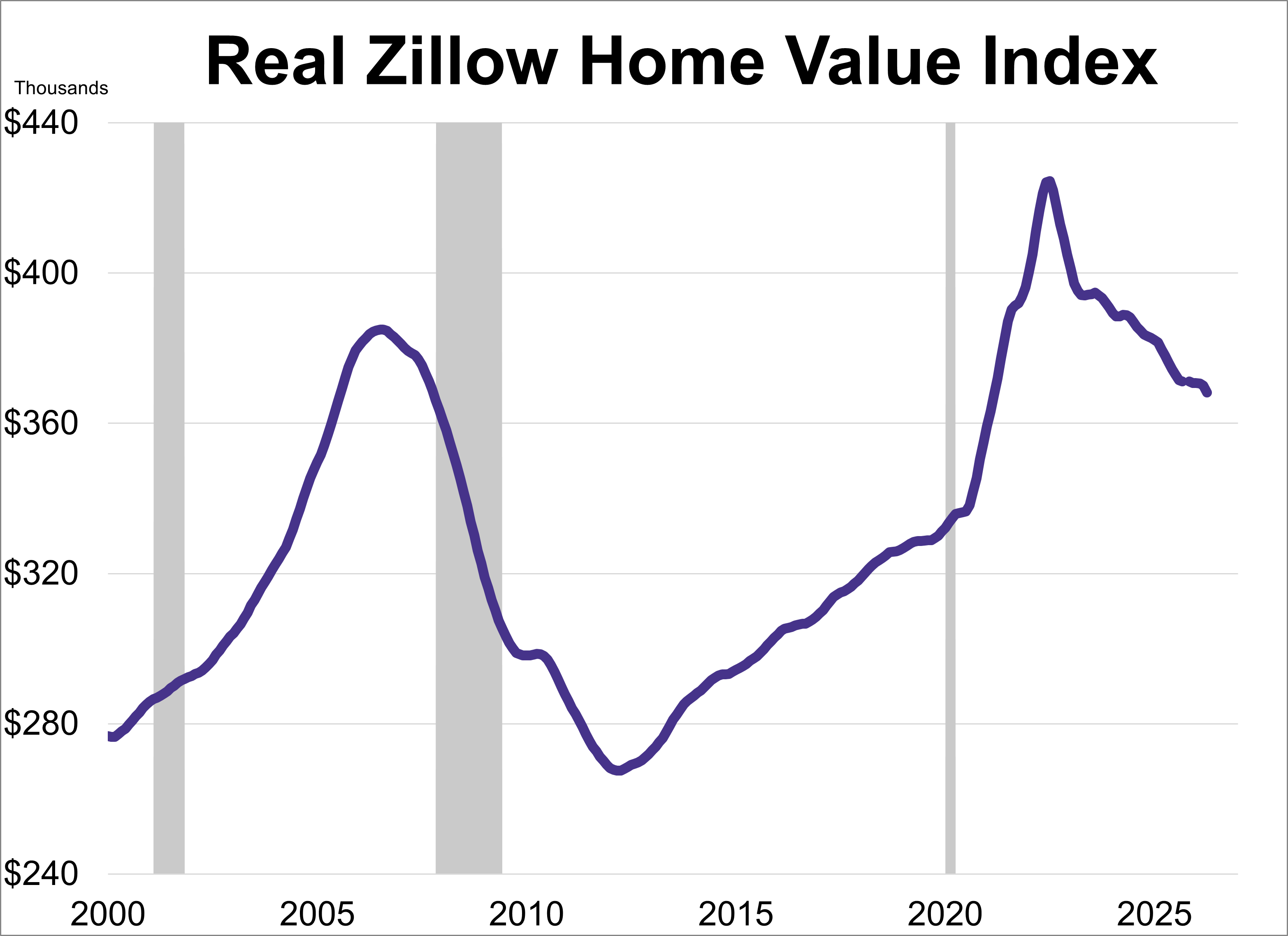

Home values continued their upward trend in April, according to the Zillow Home Value Index. However, after adjusting for inflation, real home values dropped sharply, remaining at their lowest level in over five years.

Join the experts at SS&C ALPS Advisors and VettaFi for a 30-minute discussion on May 21st at 12:30 pm ET on how the war has changed the playing field for North American midstream companies with impacts enduring well beyond the price spike.

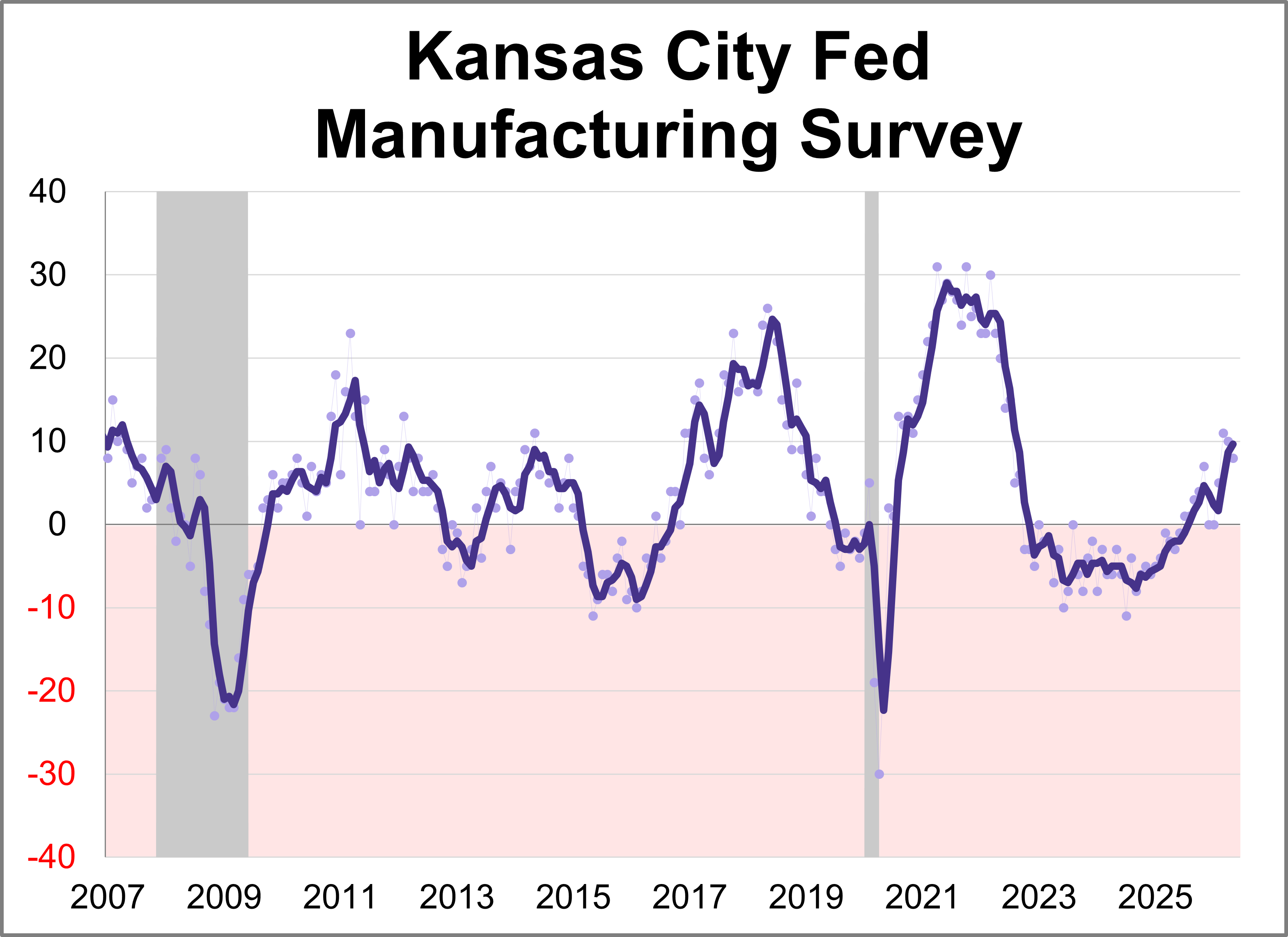

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

At Google’s developer conference, which is being held near its Mountain View, California, headquarters this week, Chief Executive Officer Sundar Pichai started his keynote by emphasizing the remarkable reach of Google’s services. Thirteen have more than a billion users, he said, and five of them have more than 3 billion.

There’s a whiff of panic among investors these days. US Treasury yields have climbed to levels unseen in more than a year at the same time as a furious rally has left stocks near all-time highs. Surely, both moves can’t coexist for long, goes the narrative.

Wall Street is racing to turn computing power into a tradable commodity with the first ETFs being filed even before the futures contracts they would track have started to trade.

Nvidia Corp., facing more investor skepticism, used its latest quarterly report to tout progress in diversifying the company, which aims to rely less on the giant data center operators that have fueled its runaway growth.

Najimah Roberson, a lifelong renter, spent the past two years searching around Harrisburg, Pennsylvania, for a home she could afford — getting outbid nearly 30 times along the way.

In the past year, new models from industry leaders have continued to boost AI’s capabilities. According to various capabilities tests, Anthropic’s Mythos model has leapfrogged other AI models – including in the ability to thwart or support cyberattacks.

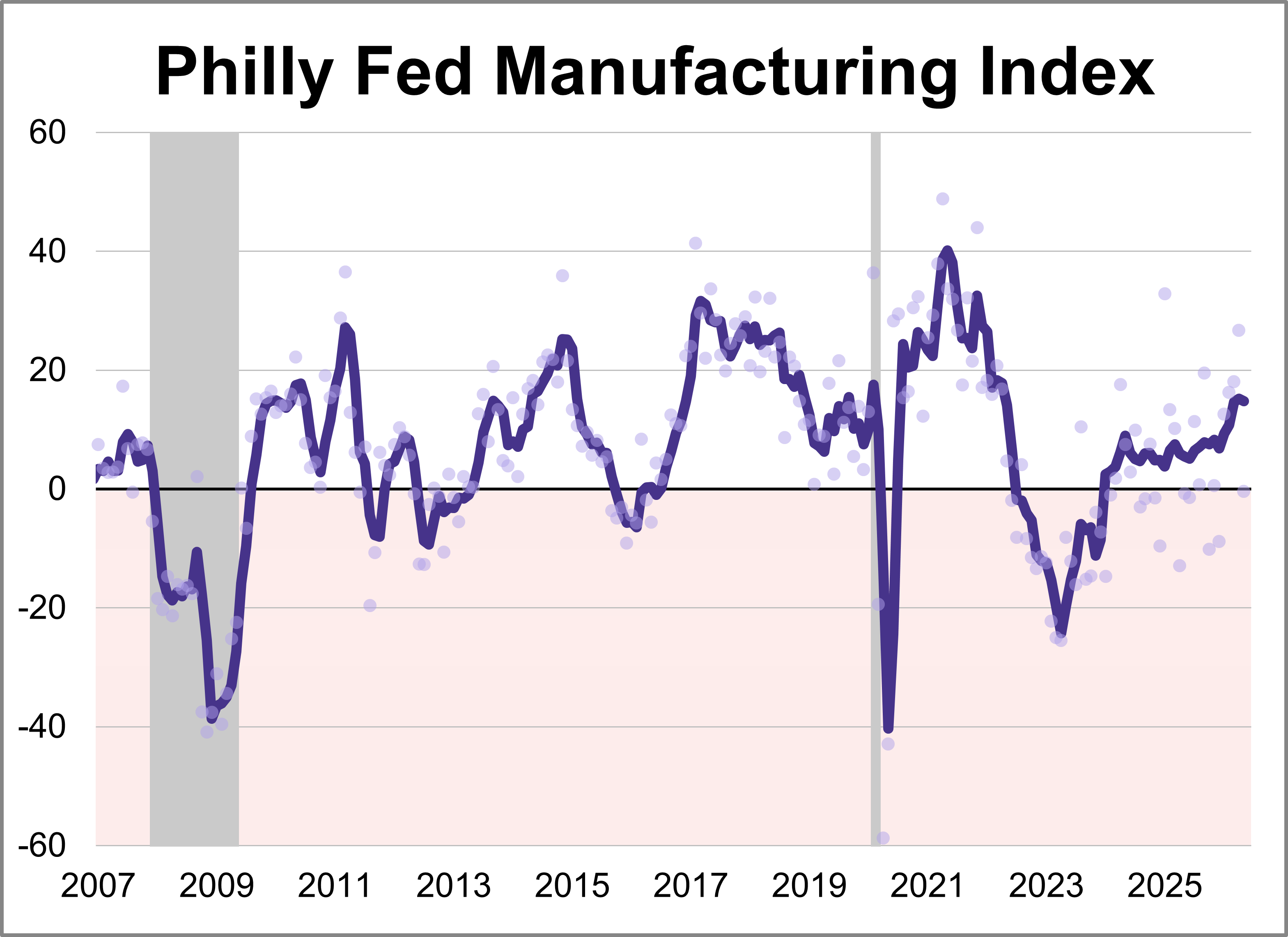

The latest Philadelphia Fed manufacturing index showed activity weakened in May, with the index sinking 27.1 points to -0.4. The latest reading marked the lowest level for the index this year and was worse than the forecast of 17.6.

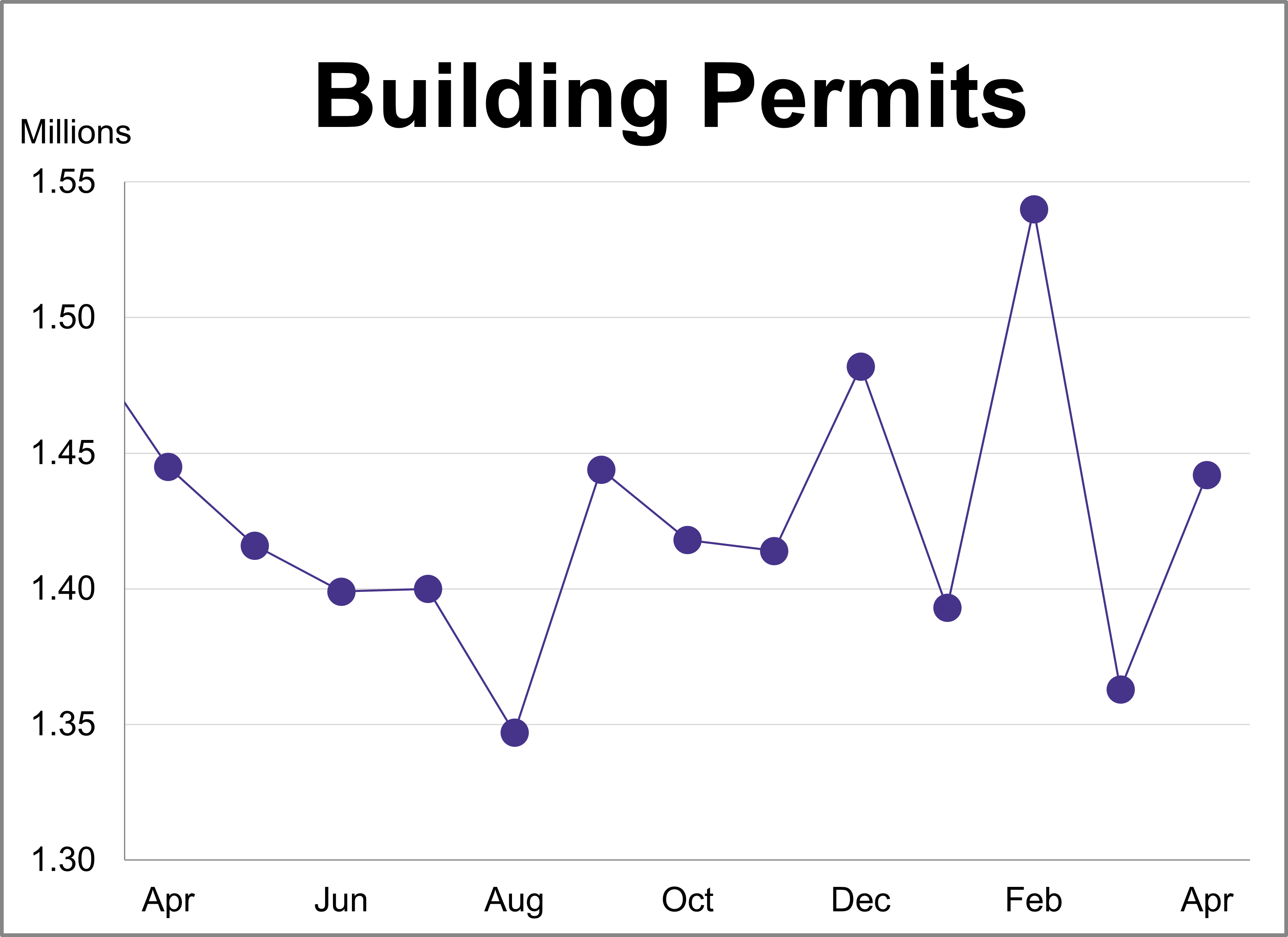

Building permits rose 5.8% to a seasonally adjusted annual rate of 1.442 million. The latest reading exceeded the forecast of 1.380 million.

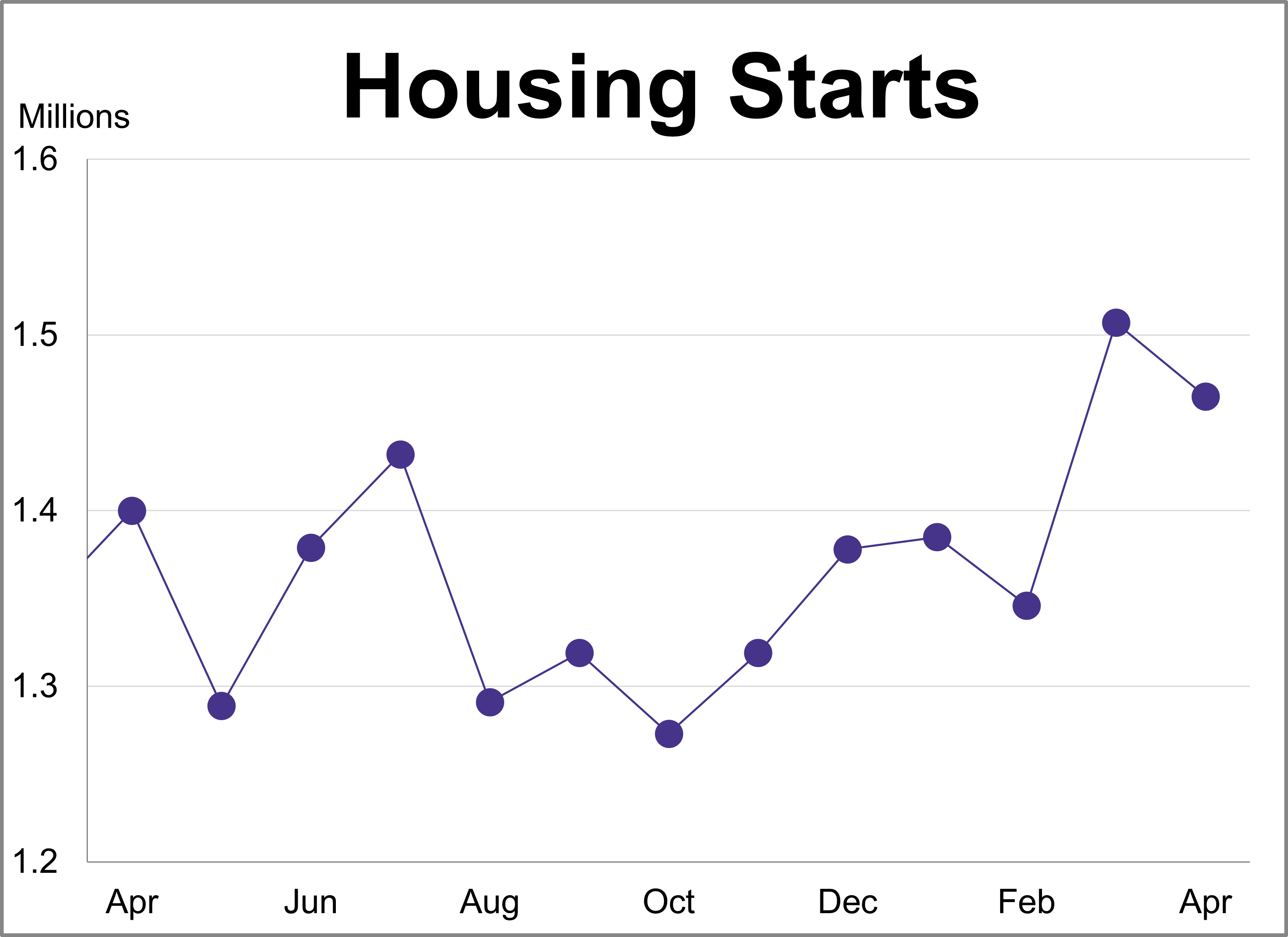

Housing starts fell 2.8% in April to a seasonally adjusted annual rate of 1.465 million. The latest reading exceeded the projected 1.420 million.

Right now, AAI’s two highest 10-year expected return forecasts are for large-cap value equity strategies outside the United States—Emerging Markets RAFI and Dev ex US Large RAFI. AAI’s expected return model anticipates valuations for equity strategies to mean revert and therefore tends to elevate out-of-favor regions and styles, predicting higher future returns for recently underperforming equity indices.

Enterprise software is undergoing its most significant reset in a generation. Artificial intelligence (AI) is reallocating value within software—creating clear winners and exposing vulnerabilities in business models that have worked well for the past two decades. We believe investors who treat software as a uniform asset class will make costly mistakes.

GMO has posted a new 7-Year asset class forecast as of April 30, 2026.

Institutional investors have spent years hearing about the promise of artificial intelligence. That phase is giving way to a more practical question: not whether AI can create more scale, but whether that scale can be governed, validated, and translated into better fiduciary decisions. For OCIO providers, AI without discipline is not an advantage.

In fixed income investing, trade execution plays an important role in overall portfolio performance. The ability to source bonds efficiently, invest capital thoughtfully and execute trades at competitive prices can directly affect investor returns.

The consumer is still spending, but with a higher level of caution. Inflation remains a persistent pressure point, particularly for lower- and middle-income households. This has caused the U.S. personal saving rate to fall to 3.6% as of March 2026, leaving significantly less breathing room for discretionary purchases.

LPL Research examines rising inflation risks amid geopolitical tensions, while resilient growth and strong investment support continued expansion.

It’s human nature to allow familiar patterns to guide our decision-making processes. But it’s just as important to recognize when changing conditions warrant a rethink. Return patterns in global equity markets appear to be shifting in ways that should prompt investors to revisit their allocations.

The exchange-traded fund marketplace continues to expand. Now with more than $20 trillion in assets under management ($14 trillion in the U.S., growing at an 18% five-year annualized clip), 2026’s volatility and emerging investment themes have taken the universe to new heights.

The "four horsemen" of the labor market are the unemployment rate, hiring rate, layoff rate, and vacancy rate. Analyzing them together may sharpen investors' read on the economy.

Inflation surged higher in April, with the Consumer Price Index (CPI) jumping 3.8 per cent from 3.3 per cent in March and the Producer Price Index (PPI) up six per cent from four per cent in March. The increase in the CPI owed much to energy and food prices.

Alex Evangeli has traded ETF products since 2007. He founded and led the fixed income trading business at Virtu Financial in Europe before relocating to New York to trade and lead the development of fixed income trading technology for the ETF block business.

Join the experts at State Street Investment Management and learn how the broader macro context is influencing sector leadership and what it may mean for portfolio positioning.

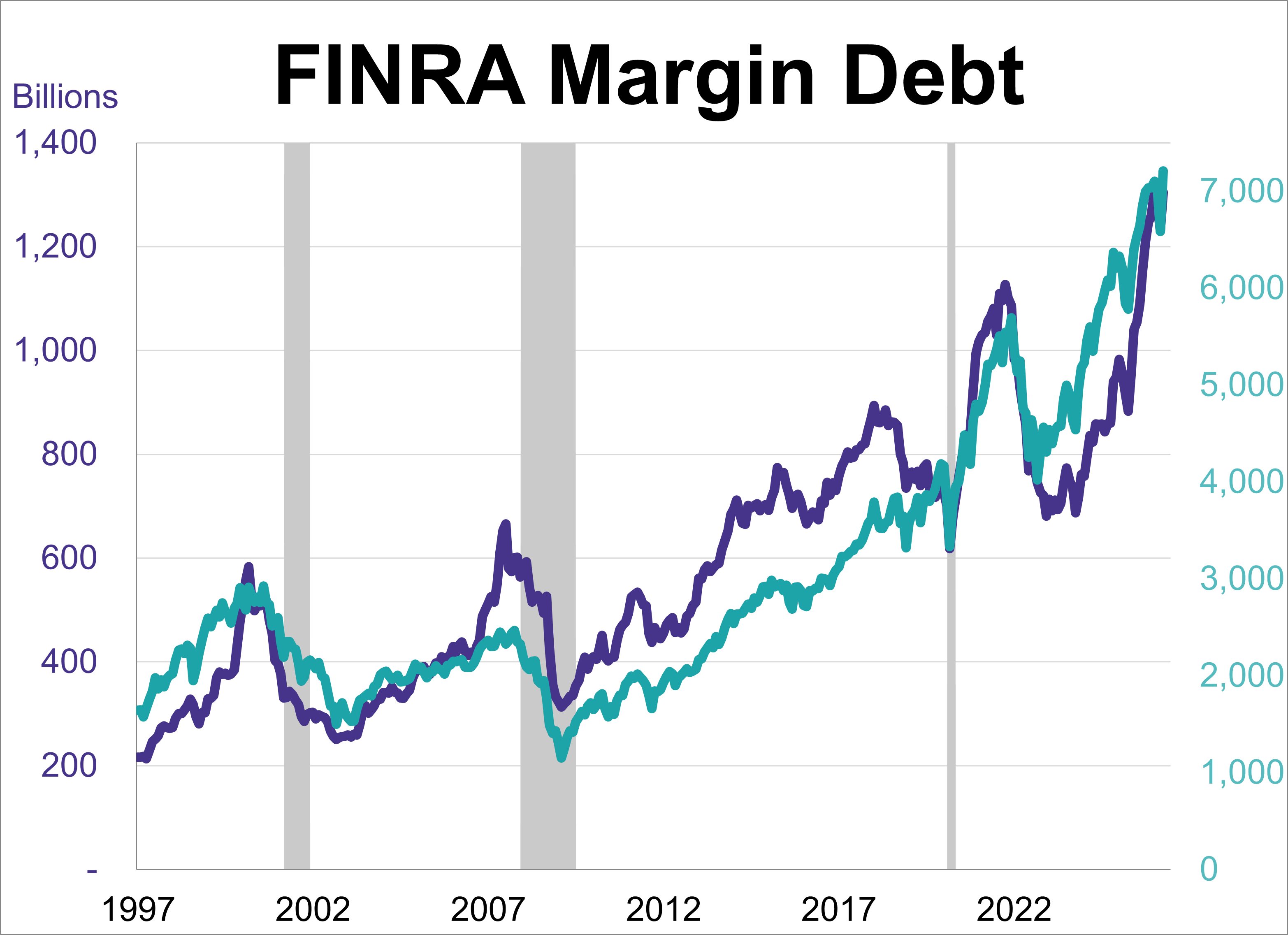

Margin debt rose for the first time in three months to a record high in April, coming in at $1.30 trillion. This marked a 6.8% increase from March and a 53.3% rise compared to the previous year.