Almost two-thirds of fund managers permit some level of “nuclear exposure,” with 34% allowing investments in nuclear weaponry, according to Jefferies Financial Group Inc.’s fourth-annual ESG and defense survey.

Global equity markets moved modestly higher this week as first-quarter earnings season continued to deliver strong results.

Despite the move lower late last week, U.S. Treasury yields are still holding well above recent lows and close to highs not seen in more than a year. By contrast, risk assets are firmly bid: U.S. equities have been routinely touching new historical highs, and credit spreads over Treasuries remain tight.

The White House’s decision to take a 9.9% stake in Intel Corp. is looking like very shrewd business indeed. Since the government bought in at $20.47 a share last August, the American chipmaker’s surging stock price has delivered the US a $43 billion return.

Gold has dropped more than 11 percent from its all-time high of just over $5,102 an ounce in January, and selling pressure continues to dominate the market. A well-established mainstream narrative is driving the bearish sentiment.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

You don’t have to go very far to find lots of negative commentary in the popular press about the current state of the US economy. High gas prices (due to a “war of choice”) are squeezing consumers’ budgets, and so the economy is headed for a ditch.

Yes, we have been there before, only to be disappointed. But the market smells a real settlement to open Hormuz, and WTI oil briefly dipped below 90 for the first time in weeks. If an opening occurs, expect the market to continue its march upward, as the momentum trade gathers strength.

Despite headwinds from rising oil prices, fundamentals have remained strong. The S&P 500 has notched 18 record highs year to date and, more importantly, surpassed our prior target of 7,250. Following a standout 1Q earnings season, we are raising our 2026 earnings per share (EPS) estimate to $326 from $300.

This week marked the passing of former Massachusetts Congressman Barney Frank. His signature legislation, the Dodd-Frank Act of 2010, was the most recent increment in a long-running history of tighter financial regulation. Some of those rules are now coming under scrutiny, with the goal of making bank lending more competitive.

This piece examines the distinction between volatility and drawdown risk in portfolio construction, and why managing routine market fluctuations may not address the drivers of long-term wealth outcomes. The article is attached as a Word document, and the related chart is included as a separate image file.

The SpaceX initial public offering prospectus is more than 400 pages of rocket fuel-grade ambition. It is also an extended warning for investors in Tesla Inc. who aren’t named Elon Musk.

On May 26, 1896, Charles Dow calculated a simple arithmetic average of 12 industrial stocks and arrived at a closing value of 40.94. Now, exactly 130 years later, that same benchmark has crossed the historic 50,000 threshold.

New AdvizorPro data shows RIAs broadened their ETF lineups in Q1 2026, leaning into real assets, active managers, and defense strategies.

The 2026 tax season is barely in the rearview mirror, but for advisors and their clients, this is when the real work begins. Right after filing, everything is still fresh. Clients remember what surprised them, what felt off, and where they may have missed opportunities. That awareness doesn’t last long.

Those driven to give to the point of harming themselves may be acting less from generosity than from deeply ingrained obligation, guilt, and fear. Helping clients navigate these conflicts requires compassion and a willingness to help them explore the emotional complexity of their money decisions.

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for May. The general business activity index rose 2.7 points to 0.4, indicating slower growth of manufacturing activity and stable business conditions perceptions.

The Conference Board's Consumer Confidence Index® fell for the first time in four months in May, dropping 0.7 points to 93.1. Despite the slight dip, the index came in above the forecast of 91.9.

Quantinuum Inc., a quantum computing company backed by Honeywell International Inc., is seeking to raise $1.05 billion in its US initial public offering, capitalizing on investor enthusiasm for the technology.

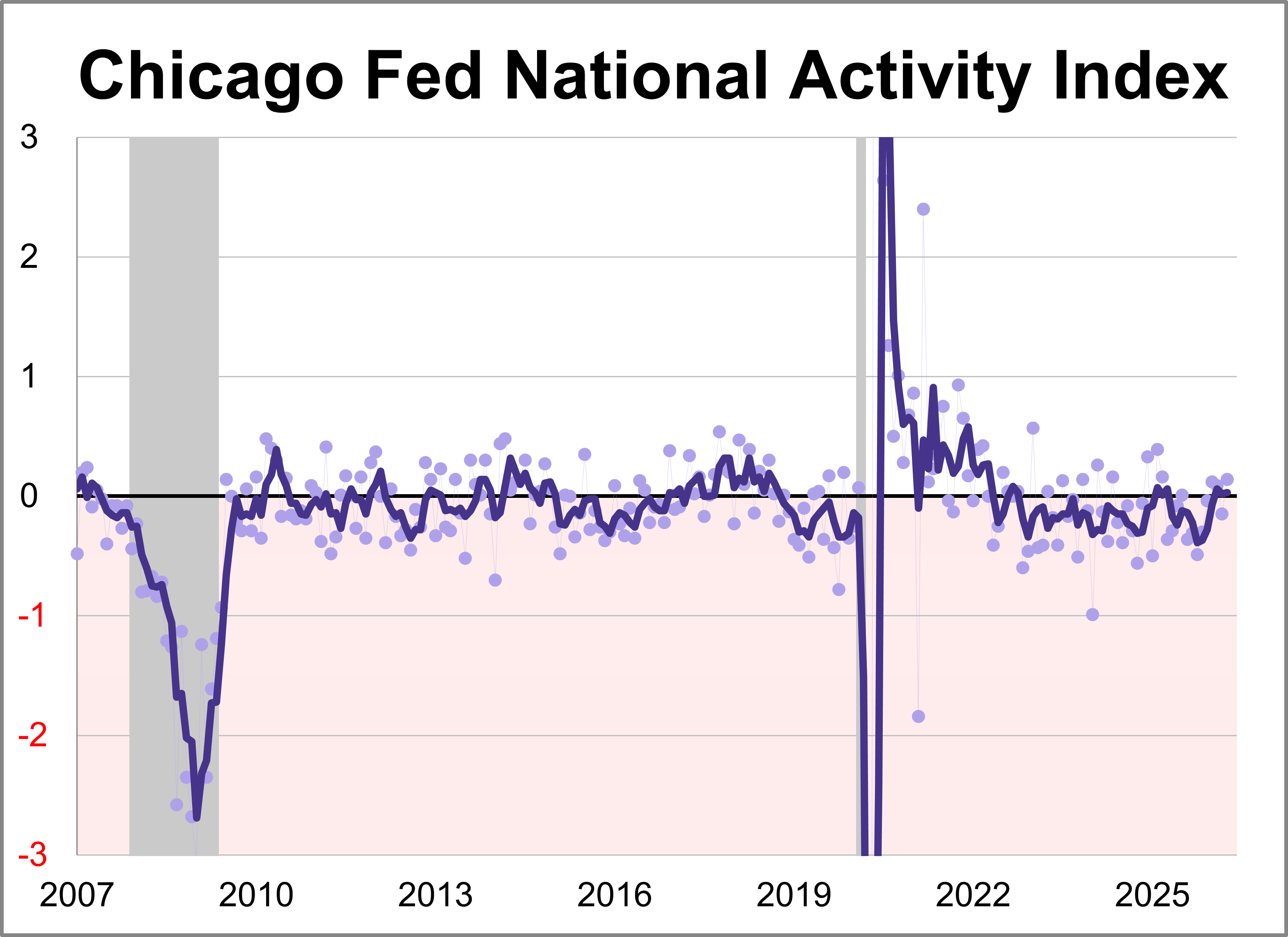

The Chicago Fed National Activity Index (CFNAI) rose to +0.14 in April from -0.15 in March. Two of the four broad categories of indicators used to construct the index increased from March, and two categories made positive contributions.

Prudential Financial Inc.’s asset-management arm has financed about $4 billion of land-banking projects through a partnership with Domain Real Estate Partners, part of a push to gain exposure to the US homebuilding industry.

As Kevin Warsh takes the helm at the Federal Reserve, bond investors are betting he’ll prioritize the central bank’s inflation-fighting credibility over President Donald Trump’s push for lower interest rates.

It’s been more than three years since Silicon Valley Bank lost a quarter of its deposits in a day, kicking off a string of bank rescues. The shocking speed of that run was attributed, in part, to the rapid spread of information on social media and the efficiency of digital banking.

I’ve lost count of the praise heaped on US hedge funds for their “historic performance” in April on artificial intelligence-related bets and alleged foresight of a ceasefire in the Iran war.

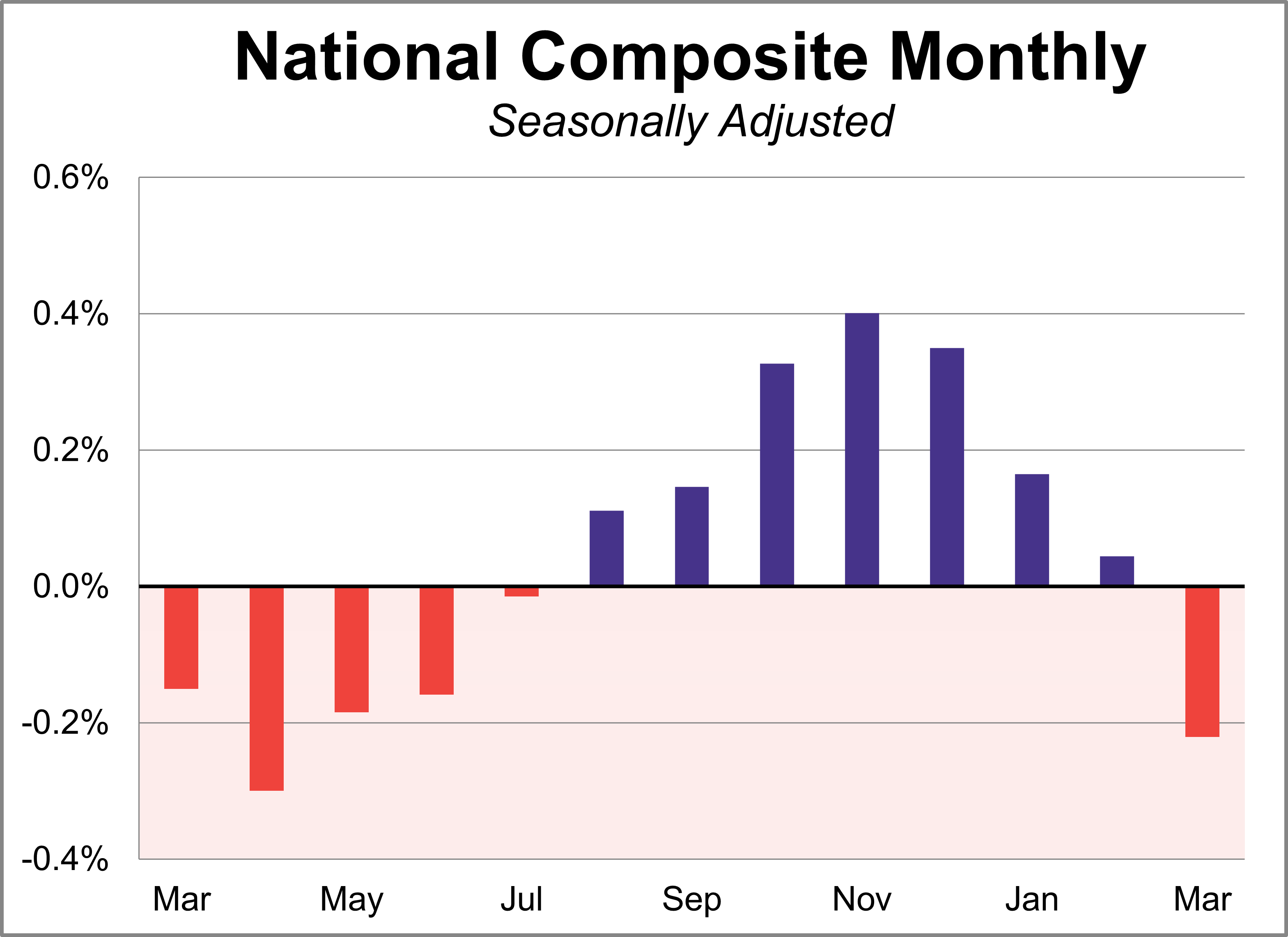

Home prices fell for the first time in eight months in March according to the S&P Cotality Case-Shiller index, as the housing slowdown intensifies. On a seasonally adjusted basis, the national index dropped 0.2% month-over-month and was up 0.7% year-over-year, the slowest pace since June 2023.

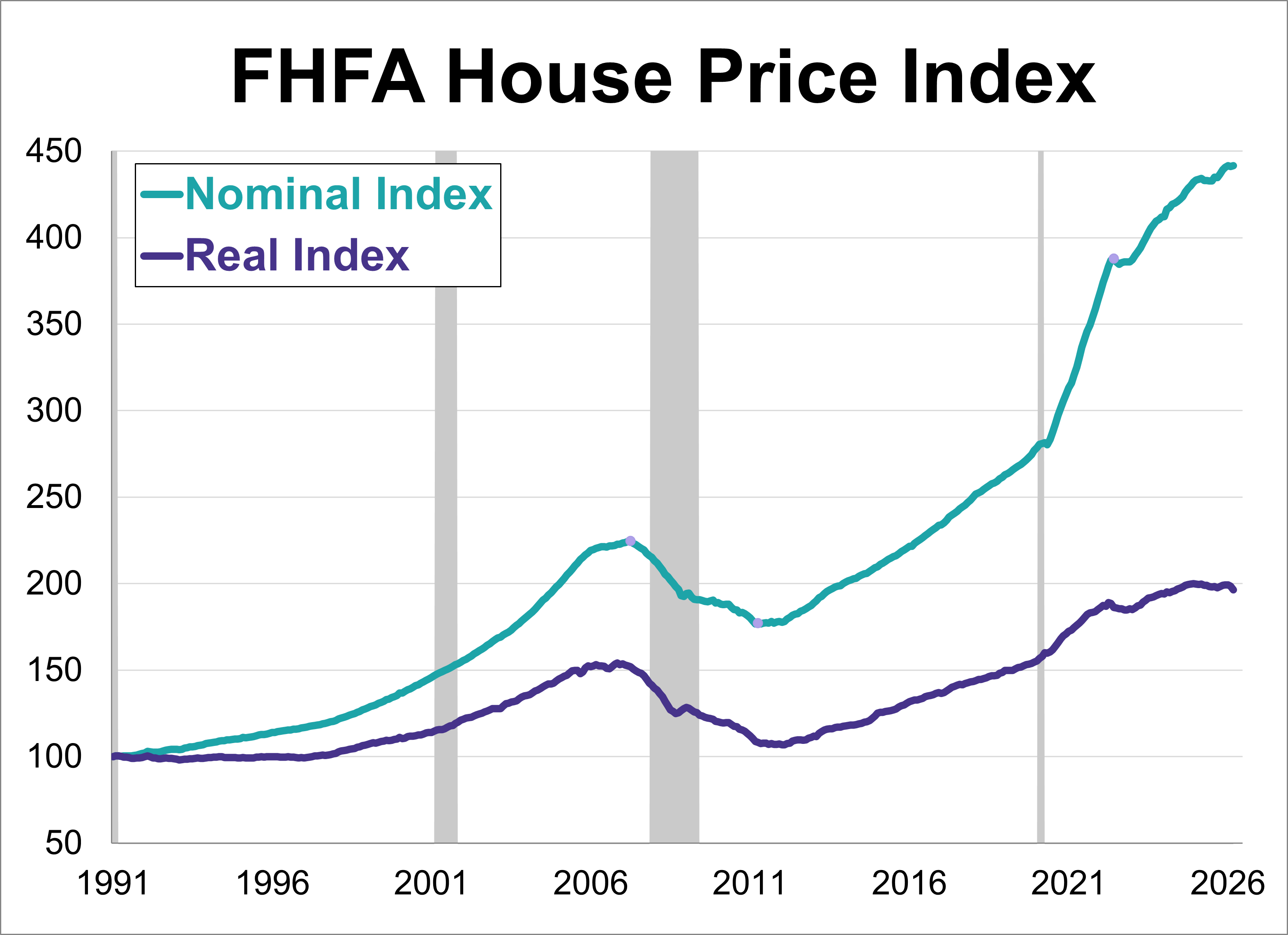

The Federal Housing Finance Agency (FHFA) House Price Index (HPI) reached a new record high in March, rising 0.1% to 441.6.

As more individuals turn to non-traditional financial advice — offered through social media, artificial intelligence, or other online services and platforms — advisors will be tasked with fostering a greater sense of trust with the public.

Last Friday closed with the 10-year Treasury yield at 4.60%, a one-year high, and the doom commentary about rising interest rates was waiting before the bell even rang. Hyperinflation. Bond market breakdown. Paradigm shift. A 1981 fair-value retest.

Private markets (private equity, private credit and real estate) have historically delivered an “illiquidity premium”. Institutions and family offices have recognized this illiquidity premium and have historically allocated significant capital to capture it.

Since the post-COVID recovery began, U.S. nonfinancial corporations have generally managed capital conservatively. They have kept credit metrics stable and, in many cases, actively improved them. That discipline was not entirely voluntary: The sharp adjustment in funding costs triggered by the Federal Reserve’s 2022–2023 rate hiking cycle raised the bar for incremental borrowing and pushed management teams toward balance sheet restraint.

In this video, Chuck Carnevale explains why he believes a diversified dividend-growth stock portfolio can be a better long-term strategy for retirees than the traditional 60/40 stock-and-bond allocation. Using a real-world portfolio he created in August 2021, Chuck demonstrates how an all-equity income portfolio can provide both rising income and capital appreciation while helping investors stay ahead of inflation.

After a slowdown earlier in the year, stronger April and May data support the view that weakness in January and February, followed by a rebound in March, was largely weather-related rather than the start of a broader deterioration in housing demand.

During the American cigar craze of the 1990s, a couple of my neighbors purchased humidors and began collecting. The holy grail for them was Cuban Cohibas, banned from import by longstanding U.S. sanctions.

Artificial intelligence (AI) might be the talk of the town these days, but quantum computing is the quiet thunder rumbling in the background. It just got much louder with the U.S. White House commiting to roll out a massive $2 billion funding package distributed across nine quantum computing companies.

I have often written about one of the few indicators in economics that has earned its reputation over the years, and for good reason. It has preceded virtually every US recession since World War II. I’m talking about the inverted yield curve.

Now, that prospect feels much farther off. Indeed, as government debt grows and macroeconomic pressures and inflation reemerge, investors face a complicated rate environment. Dividends can provide a solution.

There is currently a stark contrast between everyday consumer confidence and financial market behavior. On one hand, persistent inflation and elevated living costs have driven consumer sentiment to historic lows. On the other hand, financial market participants are exhibiting aggressive risk appetite, with margin debt surging to an all-time high record on the heels of major equity market gains.

Elon Musk has bucked the trend of industrial conglomerate breakups, including such illustrious companies as General Electric and Honeywell International Inc., and decided to form a somewhat unwieldy company that makes rockets, spacecraft, satellites, antennas, modems and now computer chips. With SpaceX’s purchase of Musk’s xAI in February, the world’s leading space company was married to an AI startup and the X social media platform.

In this second quarter update, Western Asset believes global fixed-income markets face a more complex backdrop as geopolitics, rapid AI adoption and private credit scrutiny intersect.

Chasing performance by deviating from a benchmark has long been the hallmark of active managers. But it may be time for a rethink. Our research suggests that investors allocating to core equities should consider refreshing the criteria they use to identify portfolio managers that can consistently beat their benchmarks.

For private equity firms, capital flexibility is prized today. Merger-and-acquisition (M&A) activity has cooled, while commodity prices and artificial intelligence (AI)-driven disruption have heated up, creating uncertainty for investors. This makes it more challenging to sell portfolio companies, so private equity firms are holding investments longer. As a result, many firms are turning to net asset value (NAV) loans for capital needs.

While US financial markets brace for what could be the three biggest initial public offerings ever, most entrepreneurship in the US is headed in the opposite direction: New businesses are shrinking.

By moving beyond benchmark constraints, active portfolios can access off-the-run bonds, specific securitized tranches, and maturity buckets with superior risk-reward profiles. They also have the flexibility to adjust positioning throughout the market cycle — reallocating across sectors, ratings, and issuers as conditions evolve to capture opportunities and mitigate drawdowns.

I still don’t think the Fed is close to a rate hike, but for the upcoming June FOMC meeting, a shift in the language of the policy statement from an easing bias to one of a ‘balanced’ outlook seems to be the most likely scenario. However, the fed funds futures market has now fully priced in a rate hike for March 2027, a remarkable shift from its pre-war status of discounting almost three rate cuts for the same timeframe.

Industry discussions on Janus Henderson’s ETF lineup are typically centered around its fixed income funds given the firm’s history in this asset class. However, the issuer also has equity ETFs that are garnering attention, which include a fund that’s close to crossing the $1 billion assets under management (AUM) threshold: the Janus Henderson Small-Mid Cap Growth Alpha ETF (JSMD).

Stephen Dover shares key insights from the Franklin Equity team about how artificial intelligence is changing the economics of the software industry.

Some institutional investors who had grown accustomed to outperforming the broader private equity composites are finding they have not done so consistently in recent years. Their diagnoses of the problem often center on specific decisions or biases they made in their recent manager selection, whereas a likely culprit is a falloff in the persistence of outperformance among private equity managers.

There is a growing risk of economic overheating in the US as the artificial intelligence boom expands beyond semiconductors and spills into the broader economy — never mind the tame wage growth and house prices that would typically point in the opposite direction.

College costs continue to rise, and for many families, education is one of the most meaningful investments they will make. Preparing for those expenses often requires planning years, sometimes decades, in advance.

Nvidia is now a textbook fit for quality-focused indexes in ETFs given its strong underlying business fundamentals. The company has become the smartest kid in the quality classroom, scoring exceptionally high on metrics like high return on equity (ROE), strong return on invested capital (ROIC), stable earnings growth, and low balance sheet leverage.