If you want a blueprint for how countries can survive this era of great power rivalry, look no further than Vietnam.

Growing excitement around the burgeoning space economy is increasingly favoring companies positioned to benefit not only from Elon Musk’s SpaceX filing for a public offering, but also from rising enthusiasm for space exploration and increased funding.

Large asset managers are rolling out a wave of actively managed emerging-market ETFs, pitching them as alternatives to benchmarks increasingly dominated by AI stocks.

As globalization gives way to reshoring and resurgent resource nationalism, emerging markets may offer fresh alpha opportunities through their ability to supply the raw materials required to fuel the AI boom.

Kevin Warsh was officially sworn in as 17th Federal Reserve chair on May 22. Warsh is likely to build consensus at the Fed rather than push for aggressive action to cut rates.

The U.S. government’s decision to invest $2 billion directly into nine quantum-computing companies through minority equity stakes—not just grants—signals a major shift toward treating quantum as a strategic commercial industry, with potential implications for investors seeking targeted exposure through funds like the WisdomTree Quantum Computing Fund (WQTM).

May is 529 Month. As college costs rise, learn five practical ways to maximize your plan’s tax benefits, flexibility and growth potential to prepare for the future.

Commodity market trends: Commodity markets have been on an impressive, and volatile, run so far this decade, with leadership oscillating between energy and precious metals. Not surprising, after commodities’ “Lost Decade” of the 2010s, given the asset class tends to move in long capital cycles.

Equity investors are facing monumental questions about their allocation strategies in a new market regime. Market concentration has risen sharply, valuations have climbed to record highs in parts of the market and factor volatility has dominated returns.

Recent market volatility and the conflict in Iran have understandably pushed many emerging market investors to the sidelines. But periods of uncertainty have historically offered attractive entry points into emerging market debt (EMD), particularly when underlying fundamentals are improving and asset flows are likely to increase.

Since early April, U.S. stocks have rallied sharply despite an ongoing war, rising inflation fueled by soaring oil prices (near $100/barrel), higher bond yields (up 0.6 to 0.7 percentage points), and frothy valuations (21 times projected earnings vs. a historical average of 17 times for the S&P 500 Index).

The ETF industry has exploded in popularity in recent years. Old mutual fund heavy firms have increasingly leaned into the space, while new shops have proliferated, adding all kinds of new ETFs for investors to consider. That has benefitted investors and advisors immensely.

On the surface, last week looked engineered to embarrass our positioning. The dollar index climbed to a six-week high above 99.3 by Friday and finished the week roughly flat at those levels.

California continues to demonstrate fiscal resilience, supported by strong liquidity balances and the absence of projected cash‑flow borrowing through FY 2026–27. However, Medicaid cost pressures, a progressive tax structure highly sensitive to equity market swings, and constitutional spending constraints remain key differentiators between California and other large states.

An unexpected rap on your front door is sometimes cause for anxiety. You are not sure who or what is out there, wanting to get in.

This persistent growth highlights how central low-cost core index products remain to advisor and retail portfolios alike. Even as asset managers roll out specialized strategies, capital continues to flow within broad-market beta.

A tidal wave of conversions has siphoned an unprecedented amount of capital out of mutual funds and into the ETF wrapper. Last year’s record 60 mutual-fund-to-ETF conversions in 2025 across 31 firms pushed total converted assets past $260 billion, and the past five years have now seen a grand total of 203 conversions.

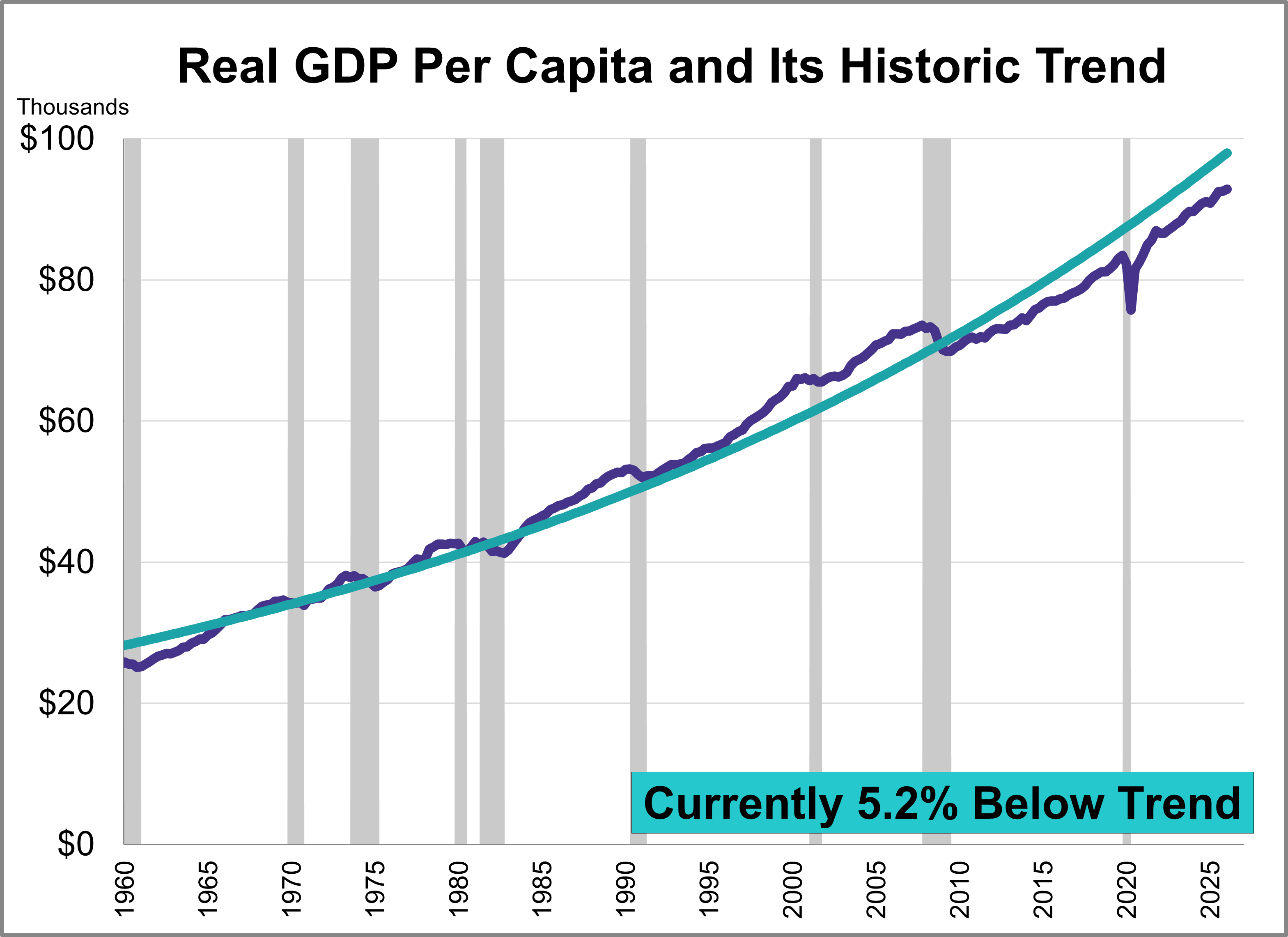

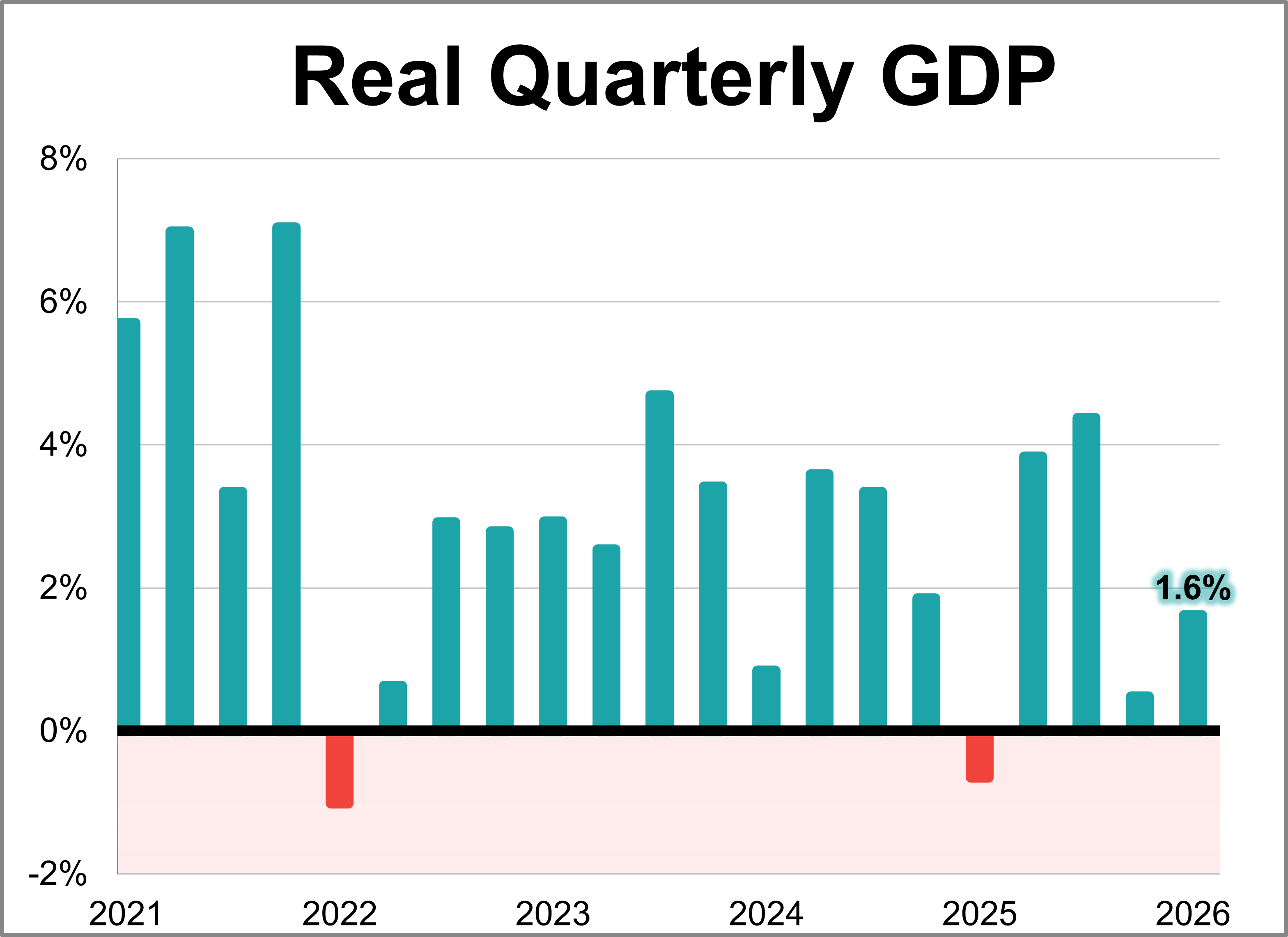

The second estimate for Q1 GDP came in at 1.62%, an acceleration from 0.48% for the Q4 final estimate. With a per-capita adjustment, the headline number is lower at 1.44%, a pickup from 0.18% for the Q4 headline number.

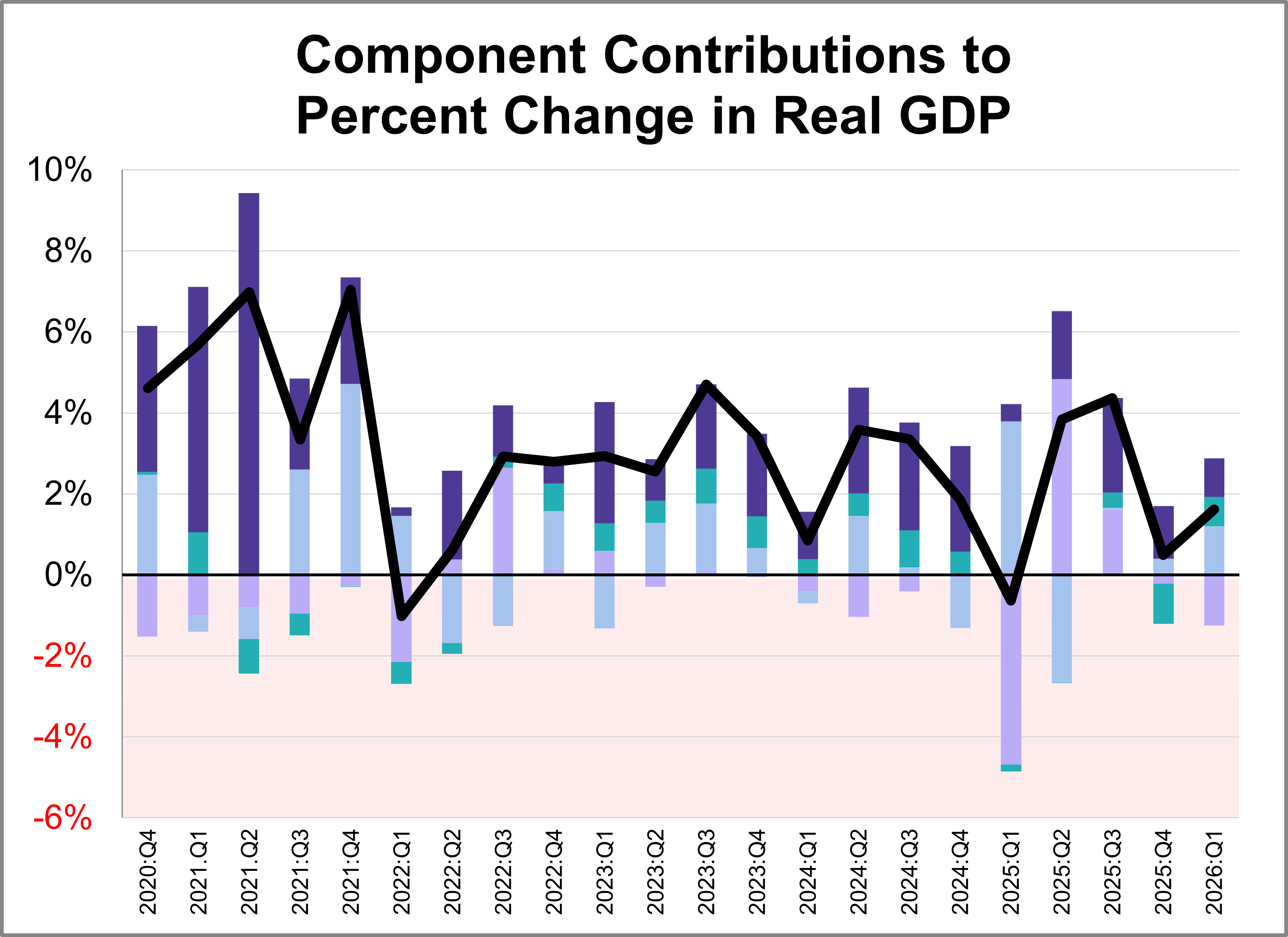

Real gross domestic product (GDP) is comprised of four major subcomponents. In the Q1 2026 GDP second estimate, three of the four components made positive contributions.

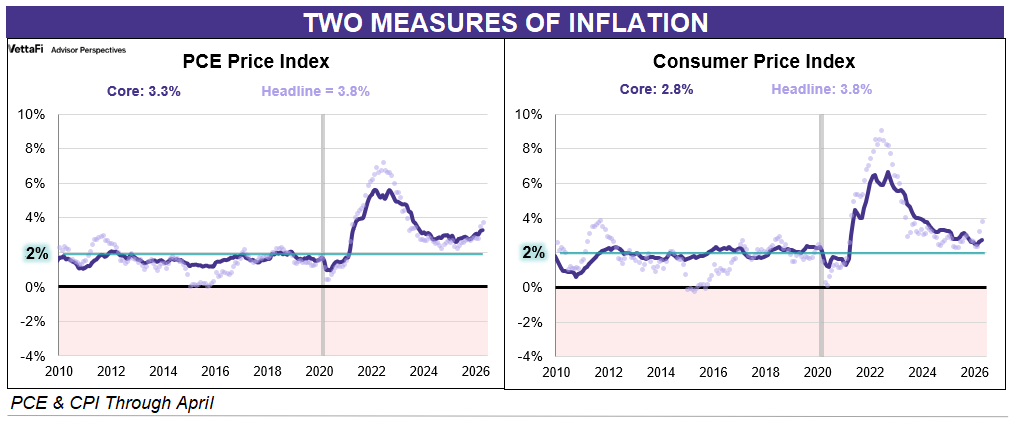

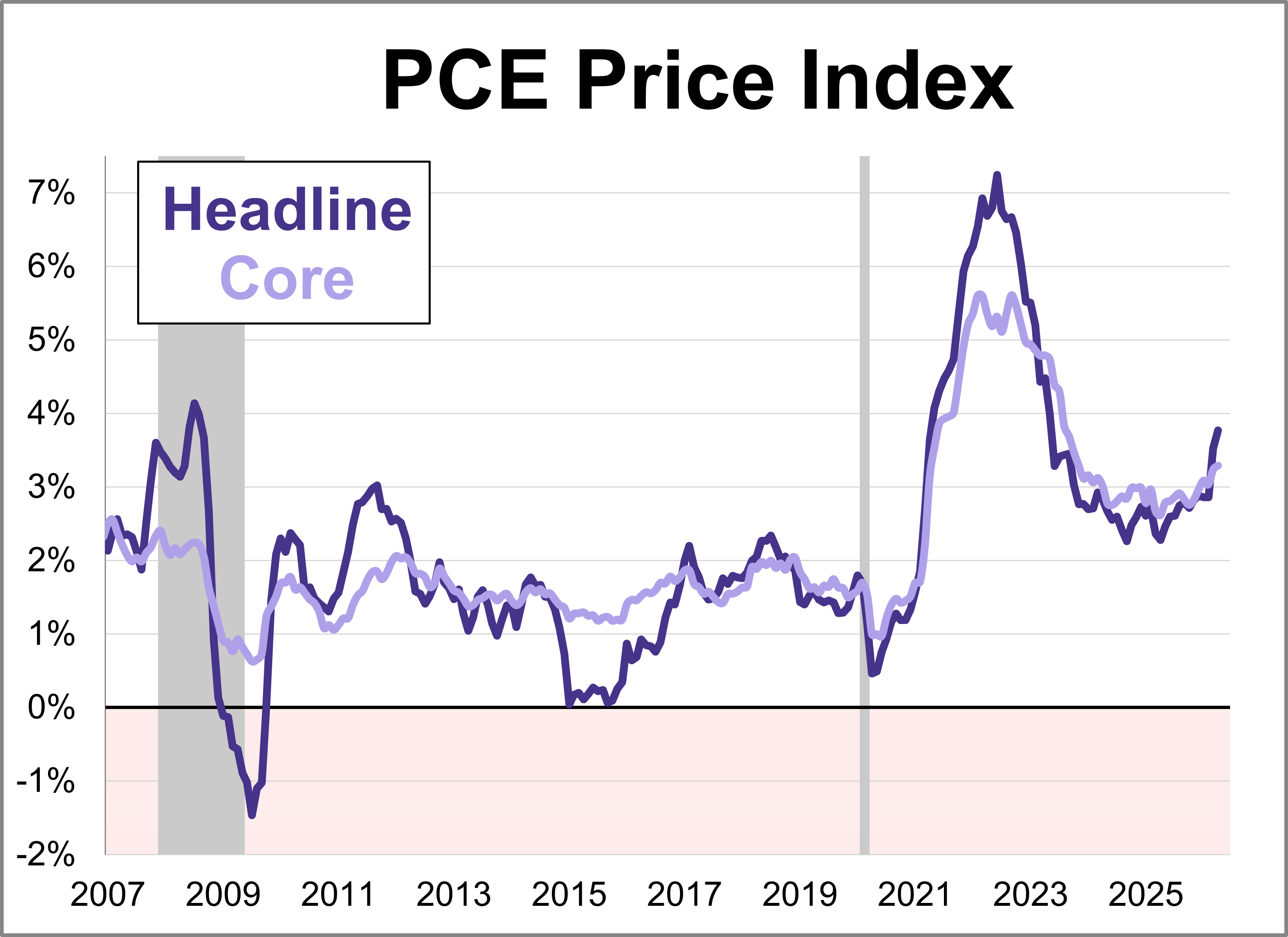

Inflation remains a hot topic, directly impacting everything from your grocery bill to interest rates. As of the latest data, two key inflation gauges — the Personal Consumption Expenditures (PCE) Price Index and the Consumer Price Index (CPI) — show that prices are still above the Federal Reserve's 2% target, with the core PCE at 3.3% and core CPI at 2.8%.

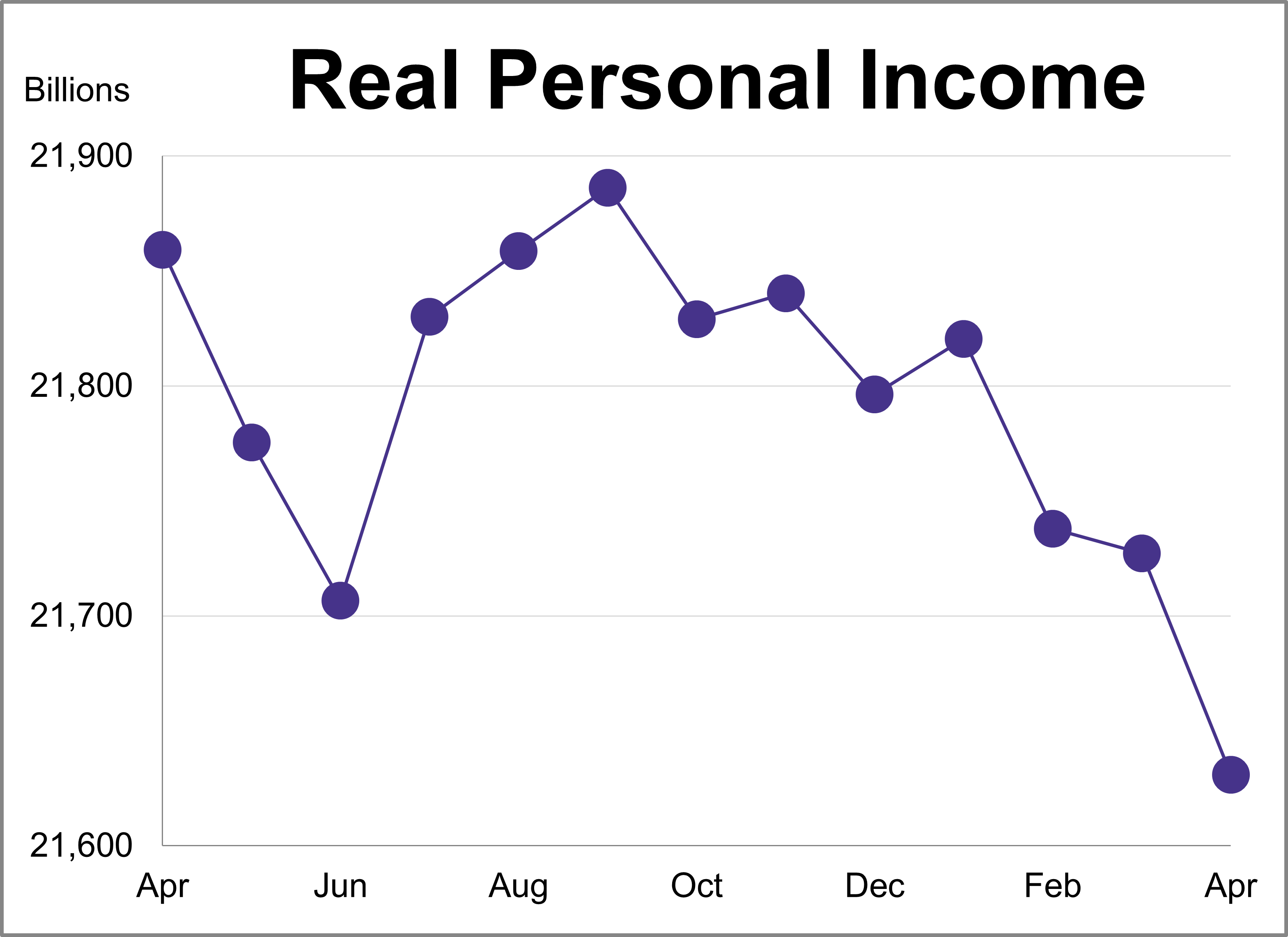

Personal income (excluding transfer receipts) was down 0.05% in April and was up 2.68% year-over-year. However, when adjusted for inflation using the BEA's PCE Price Index, real personal income (excluding transfer receipts) was down 0.44% month-over-month and down 1.04% year-over-year.

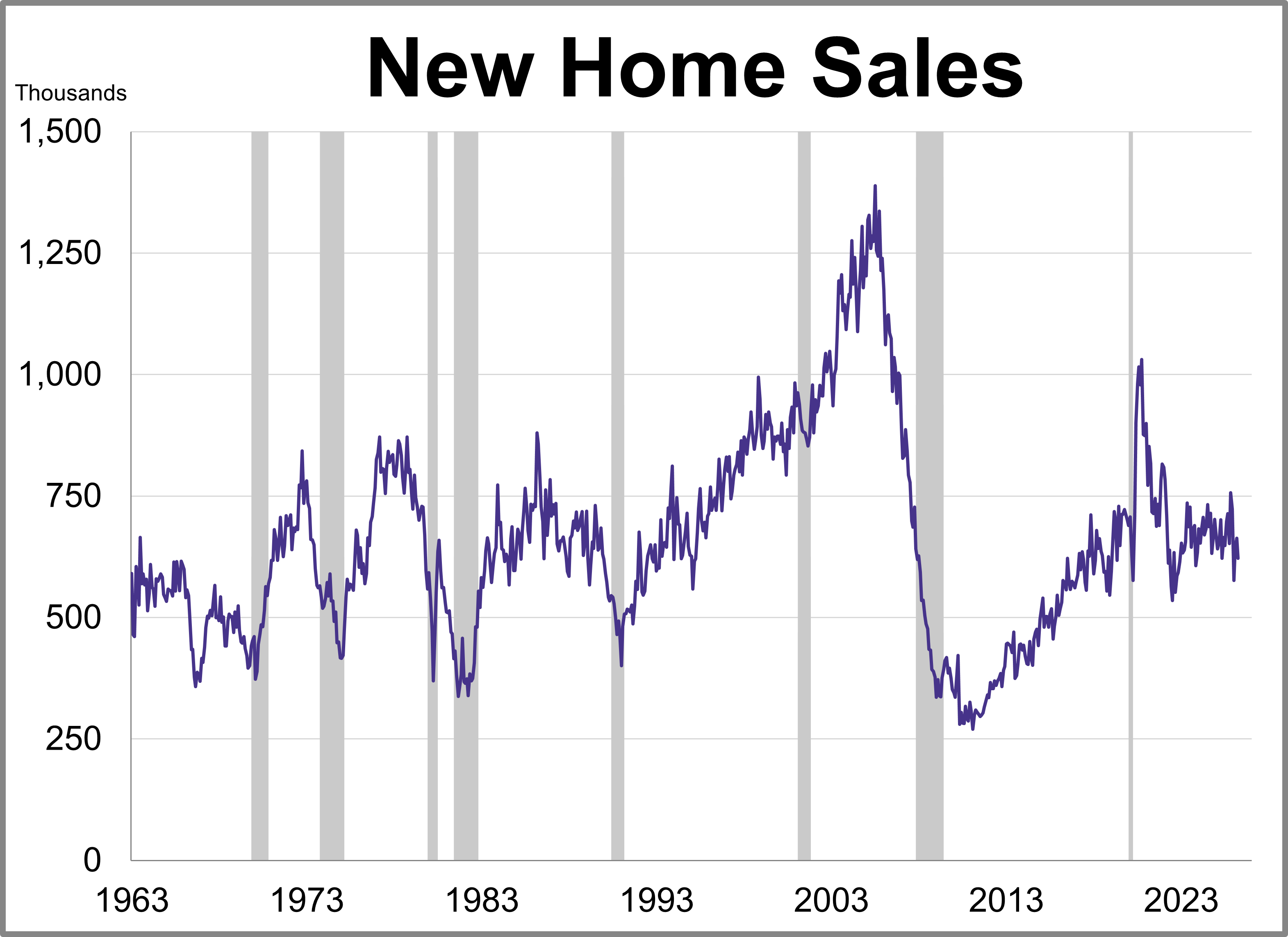

New home sales fell more than expected in April while the median price experienced its largest jump in seven years.

Treasuries rallied back to be little-changed on the day, erasing earlier declines spurred by higher oil prices, after a key US inflation gauge rose less than expected.

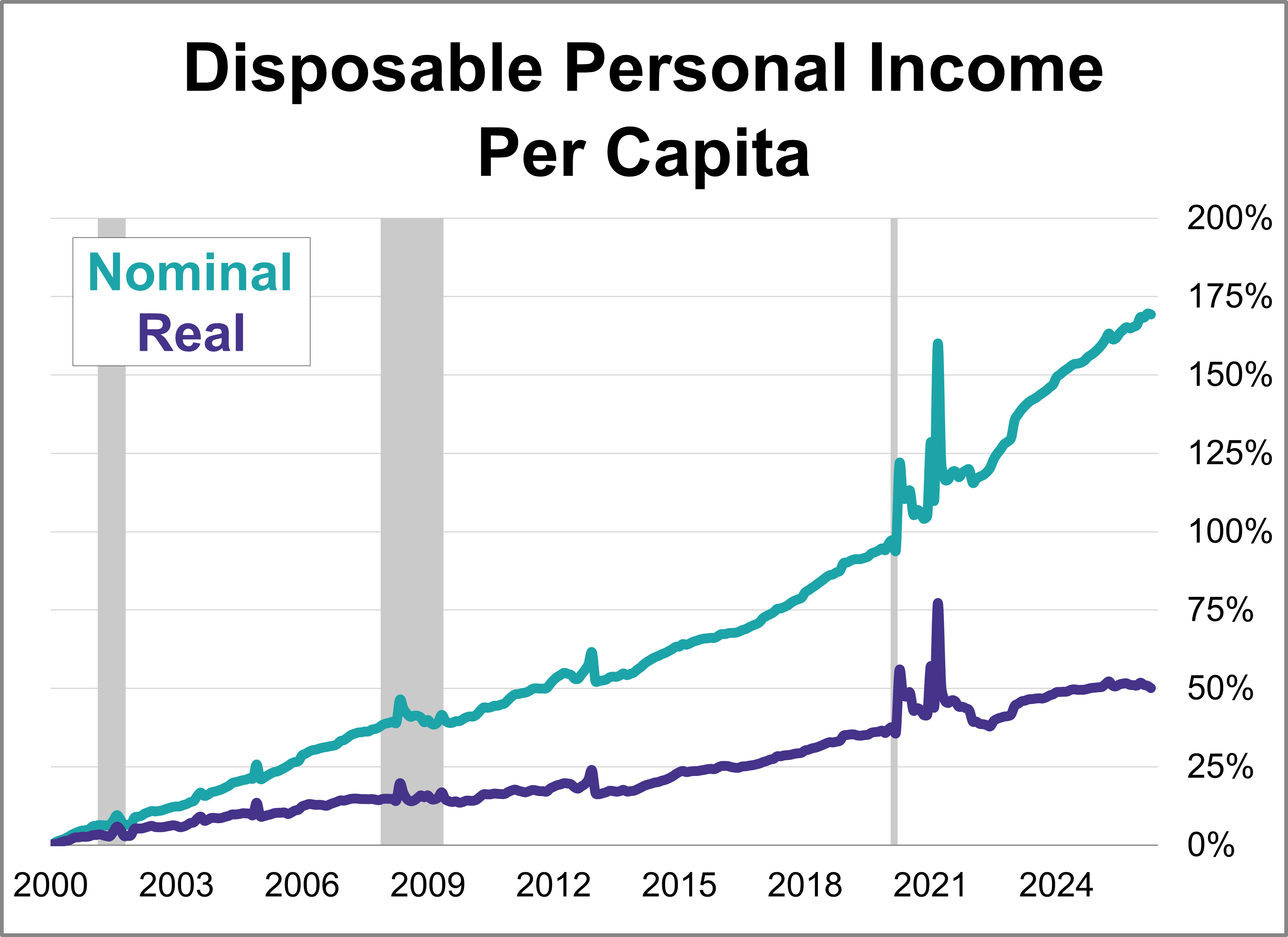

With the release of April's report on personal incomes and outlays, we can now take a closer look at "real" disposable personal income per capita. To two decimal places, disposable income per capita was up down 0.10% month-over-month. But when adjusted for inflation, real disposable income per capita was down 0.50%.

Shares of retailers spanning Kohl’s Corp. to Best Buy Co. and Dollar Tree Inc. rose on Thursday amid optimism that shoppers are still spending when they see what they want at the right price.

An abundance of cash in US funding markets appears to be driven by deeper structural shifts that are unlocking billions of dollars in balance-sheet capacity at the biggest banks, Wall Street strategists say.

Coverage of prediction platform Polymarket has recently converged on a single statistic, delivered with the cadence of a verdict: Most users lose money. The top 1% of accounts capture roughly three-quarters of the gains, while most traders since 2022 are underwater.

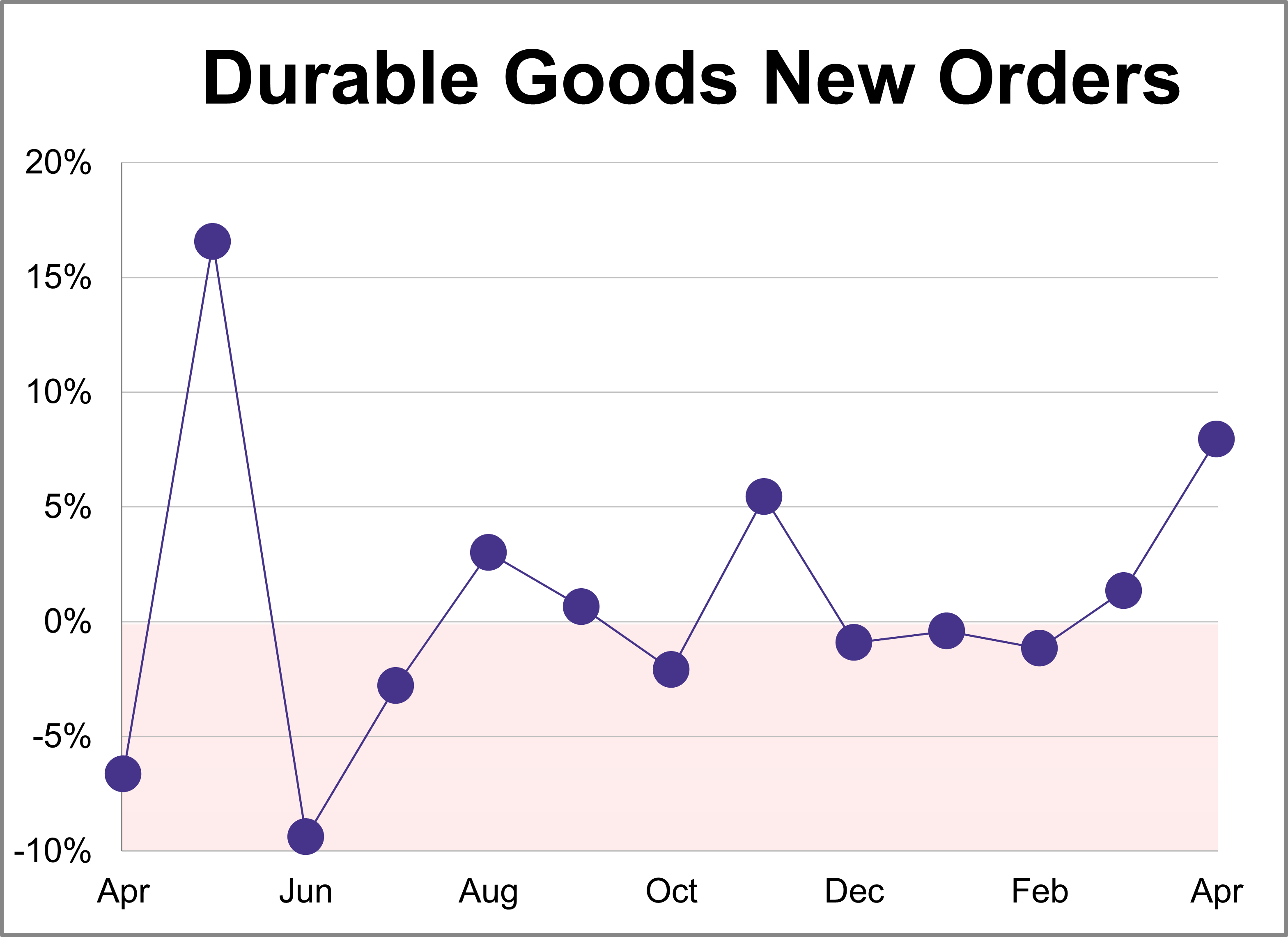

New orders for manufactured durable goods jumped 7.9% in April to $345.96B, almost twice as much as the projected 4.0% monthly growth.

Bankers are preparing to sell a jumbo debt package to support the $110 billion acquisition of Warner Bros. Discovery Inc. It’s a risky deal and comes at a moment when the bond markets have been wobbling.

U.S. economic growth rebounded at the beginning of 2026, according to the BEA’s latest estimate. Real GDP rose at 1.6% annual rate in Q1, falling short of the 2.0% forecast but marking an acceleration from the 0.5% final estimate seen in Q4 of last year.

The Federal Reserve’s preferred inflation gauge, the core PCE price index, climbed 3.3% year-over-year in April. This marks the highest level since November 2023 and marks a steady pickup from March's 3.2% reading. On a monthly basis, core prices rose 0.2%.

In a relatively light week for traditional economic data, a mix of corporate earnings, business surveys, Federal Reserve minutes, and the latest read on the consumer from the University of Michigan helped paint an increasingly clear picture for investors.

The push for international equities diversification continues amid shifting global macroeconomic conditions. These days, investors have more options when it comes to international exposure. Given the current market uncertainty, they may want to put quality at the forefront of their decision-making process.

It’s the first word that comes to mind to describe Q1 2026 U.S. company earnings. S&P 500 earnings growth is looking set to reach 28% year over year (yoy), more than double the consensus estimate of 12% at the start of the reporting season.

The artificial intelligence (AI) boom has transitioned from an equity market narrative to a defining force in fixed income. Hyperscalers (Amazon (AMZN), Alphabet (GOOG/L), Meta (META), Microsoft (MSFT), and Oracle (ORCL)) are shifting from internal cash flows to substantial bond issuance to fund massive data center, graphics processing unit (GPU), and power infrastructure buildouts.

Thanks to strong gains in markets over recent years, the 60/40 default portfolio has quietly morphed into a bundle of expensive U.S. growth equities and credit exposures offering narrow spreads over Treasuries.

Contrary to what legal television series portray, verdicts rarely turn on a single moment of drama. They take shape gradually, as evidence accumulates and a broader narrative comes into focus.

US growth stocks underperformed in early 2026 amid AI disruption fears and an unresolved conflict in the Middle East. But these stresses could create favorable conditions for selective, diversified investors to unlock long-term growth potential in a rotating market.

Goldman Sachs Asset Management (GSAM) made a big announcement this week, touting $100 billion in total ETF AUM. The milestone comes following the firm’s recent acquisition of Innovator ETFs adding several notable funds to the firm’s overall roster.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing.

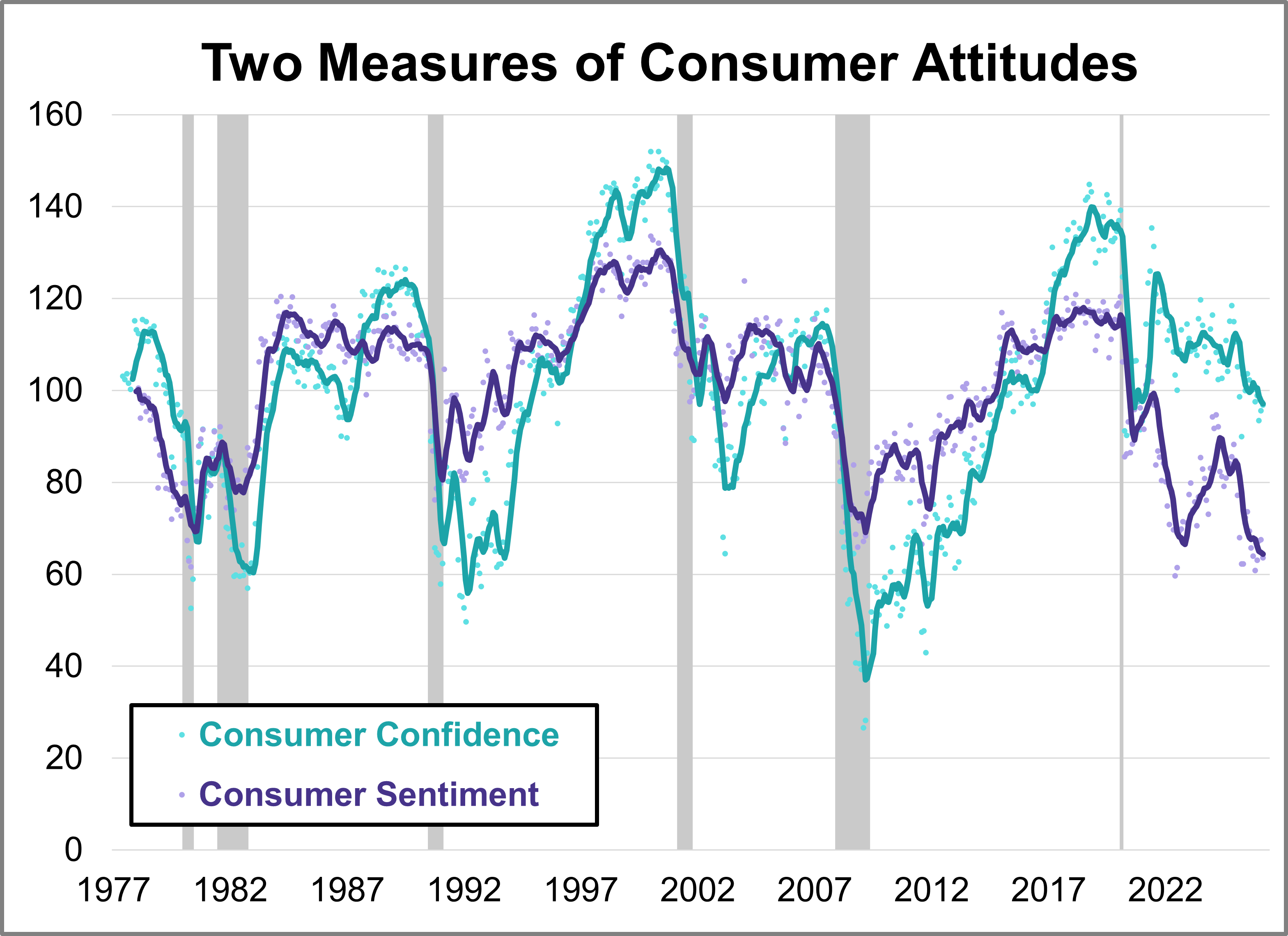

What are consumers thinking about the economy? Their collective mood offers crucial clues for businesses, investors, and policymakers alike. In May, the two leading benchmarks, the University of Michigan’s Consumer Sentiment Index (MCSI) and the Conference Board’s Consumer Confidence Index (CCI), offered similar views with both retreating amid ongoing inflation concerns.

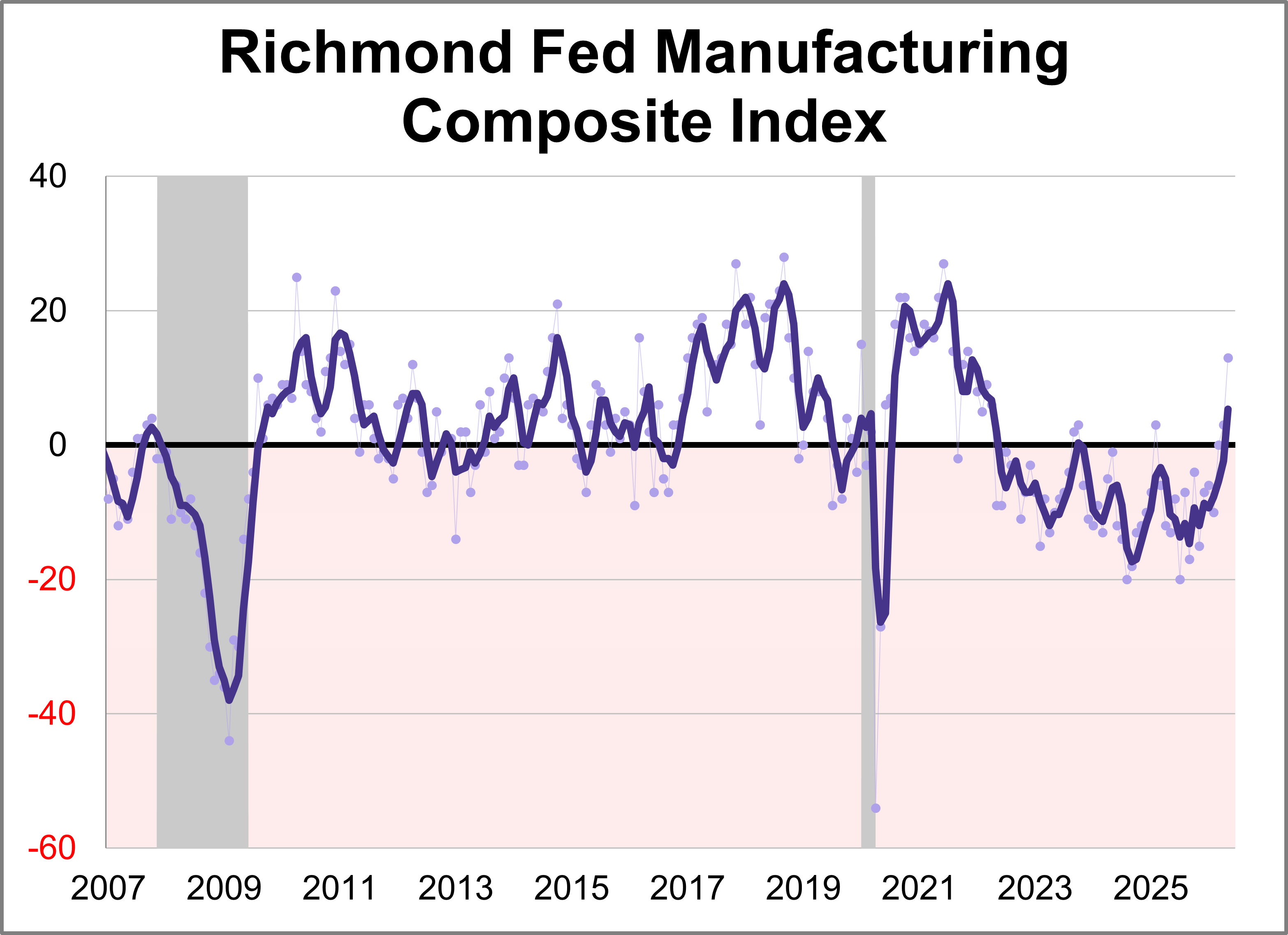

Fifth district manufacturing activity increased in May according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose ten points points to 13, marking the highest level in nearly five years. This month's reading was above the forecast of 4.

Join the experts at Reckoner for an educational webcast exploring the CLO space and how to navigate it.

Advisory firms need tighter integration between their daily work tools and the CRM at the center of their world. When notes sit siloed from the rest of a firm's data and operations, the chance to deepen team collaboration and sharpen client insights goes with them.

Leading with bad news can feel wrong and even confrontational at some level, but the psychology research supports it, the behavioral finance supports it, the career math supports it, and the clients who stay through multiple cycles apply the final confirmation stamp.

Some people do much better with change than others. It isn’t that they can’t change or they actively resist it. Rather, they experience more fear, more concern and they need more clarity about what the change means to them.

Private credit is more inherently complex than the traditional bond market. In comparison, private credit information comes at a deficit. That’s because private credit loans are essentially bespoke agreements between a lender and a private borrower.

The breakneck surge in memory-chip stocks is intensifying, sending the market capitalizations of SK Hynix Inc. and Micron Technology Inc. above $1 trillion for the first time, as investors bet the AI boom will lead to a sustained revaluation of the industry.

Despite the pickup, India’s municipal paper still makes up for less than 1% of the total rupee bond sales. By comparison, the segment represents 7% of the overall bond market in the US, according to CareEdge Ratings’ January report.