U.S. equities are lower as the global markets await the final results of the U.S. midterm elections as the control of the Congress remains undetermined.

The U.S. Dollar Index (DXY) took a dive last Friday following a middling jobs report.

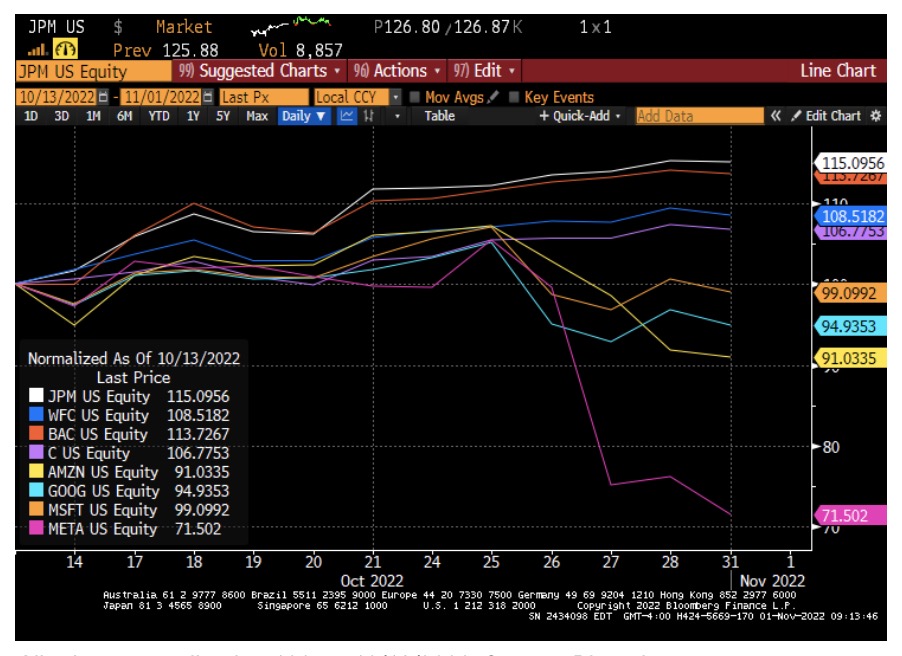

Market negativity reached a crescendo sometime around the middle of October, as interwoven narratives of doom and gloom occupied investor and media attention

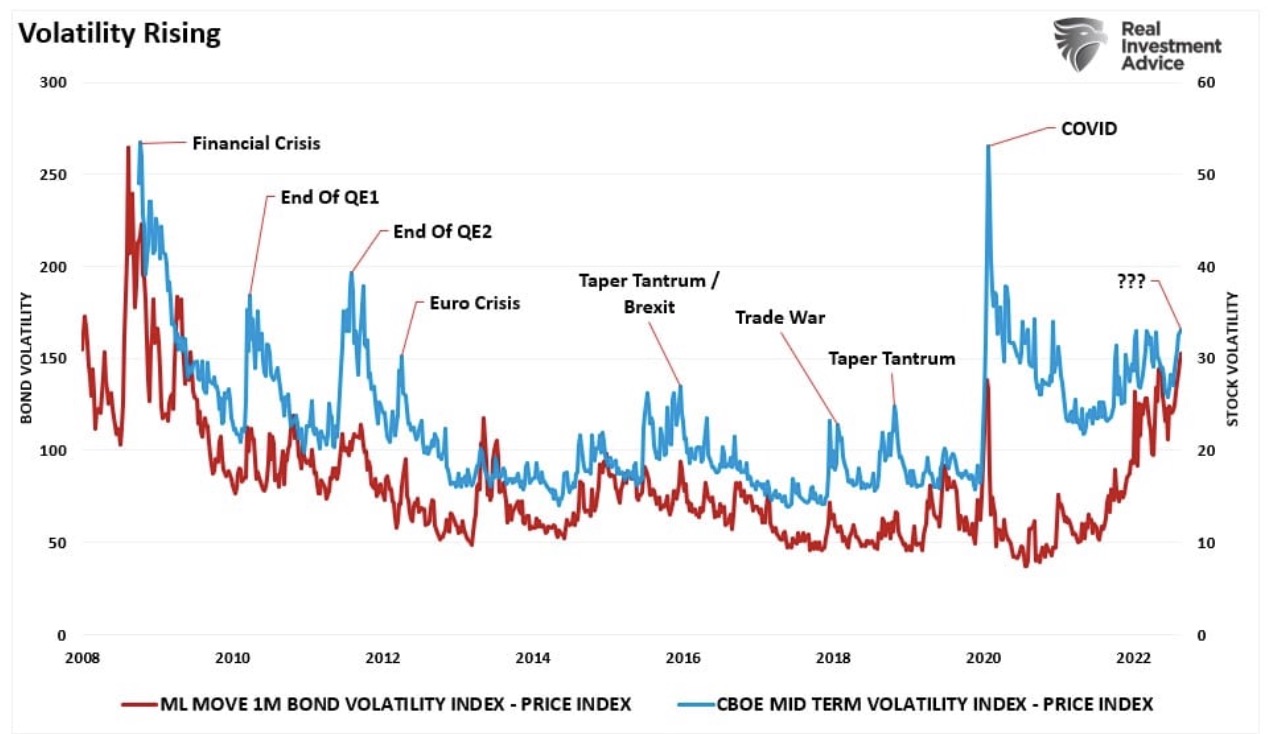

The Federal Reserve has been raising rates at an extremely aggressive manner in 2022, taking the federal funds rate from 25bps to 4%.

The era of the dynamic sales growth tech company, with a religious quality to its leadership, appears to be over.

Senior Investment Strategist Steve Lipper examines two calendar-based performance patterns that may suggest robust small-cap returns lie ahead.

Election day is tomorrow and will bring results for key Senate, House, and Governors races from all around the country, plus local legislative races and more.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

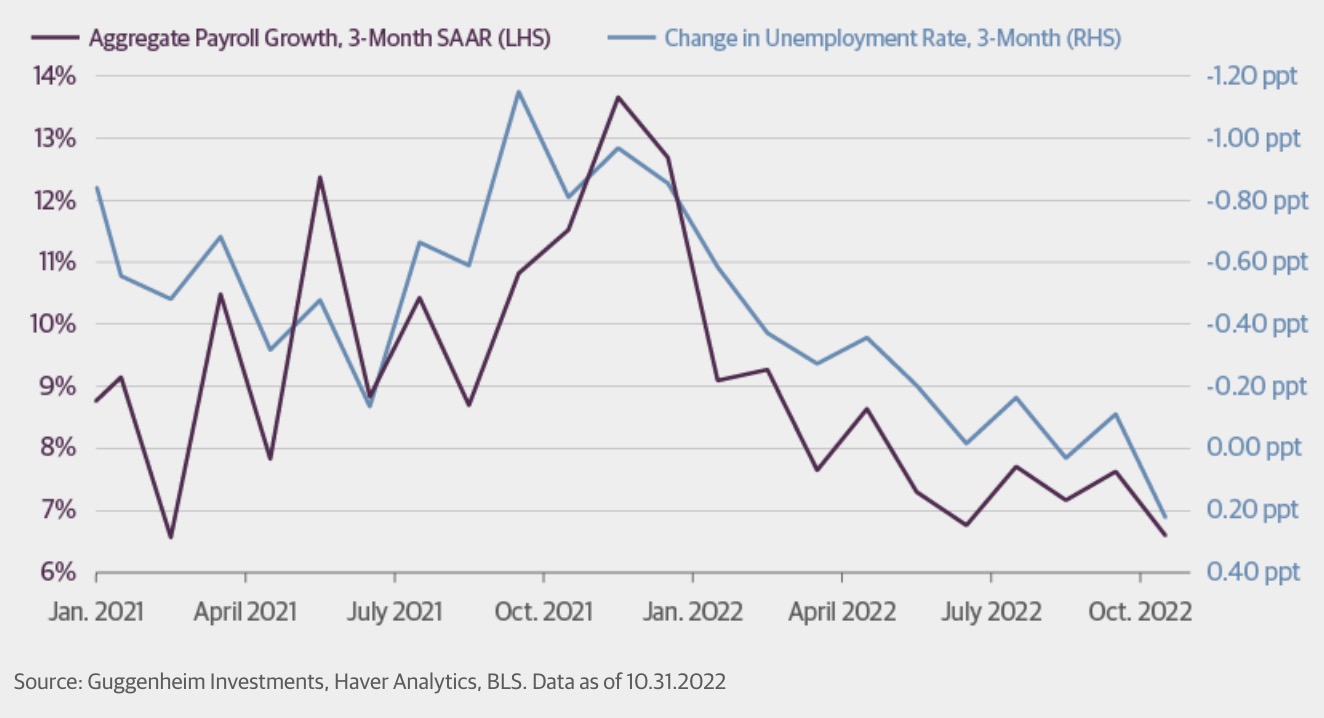

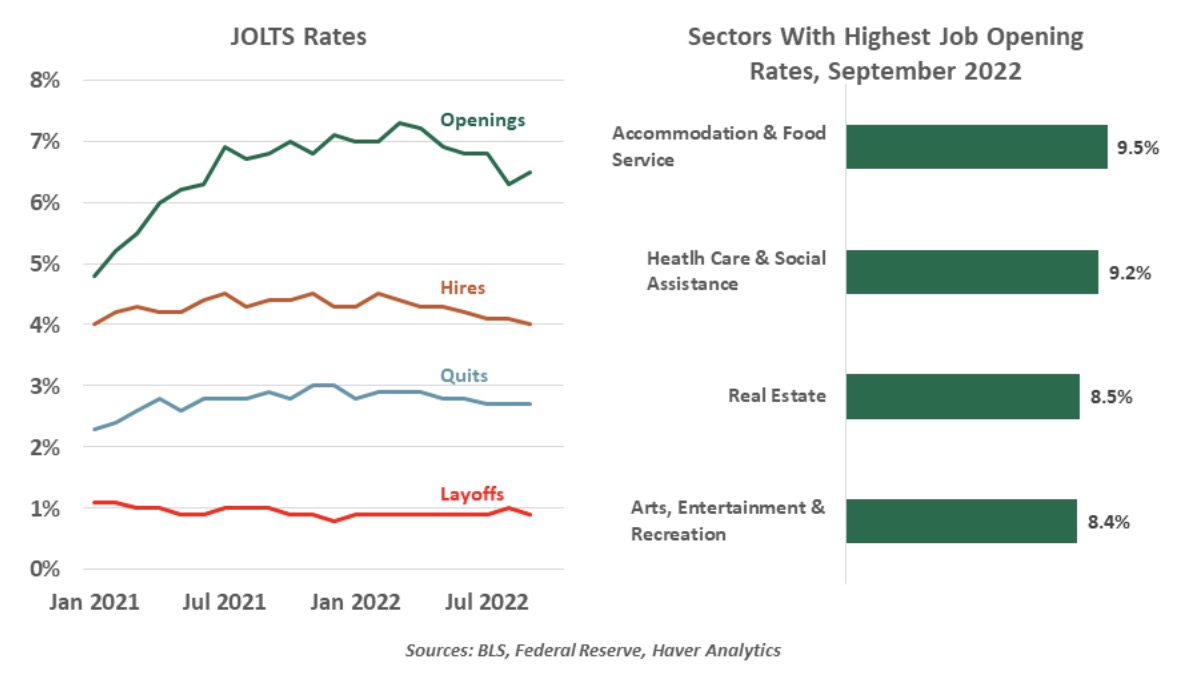

October jobs data suggests a cooling labor market.

Equities saw a strong rebound last month, with the S&P 500 gaining 8% and the Dow posting its biggest October ever¹. Was this the start of a new bull market? In this week’s “What to Watch”, we explore this question and dive into historical bear market rallies.

The Fed will keep hiking, but at a slower pace.

October started strong and then slid to new lows but managed to rally back toward the month’s end.

Precious metals investors remain cautious following the Federal Reserve’s latest jumbo rate hike.

I have been in Spain since early September, which is why you have not seen me in these pages for a while.

As I see it, decentralized assets have never looked more attractive than they do now.

Historically speaking, this phase of life we call “retirement” is a new concept.

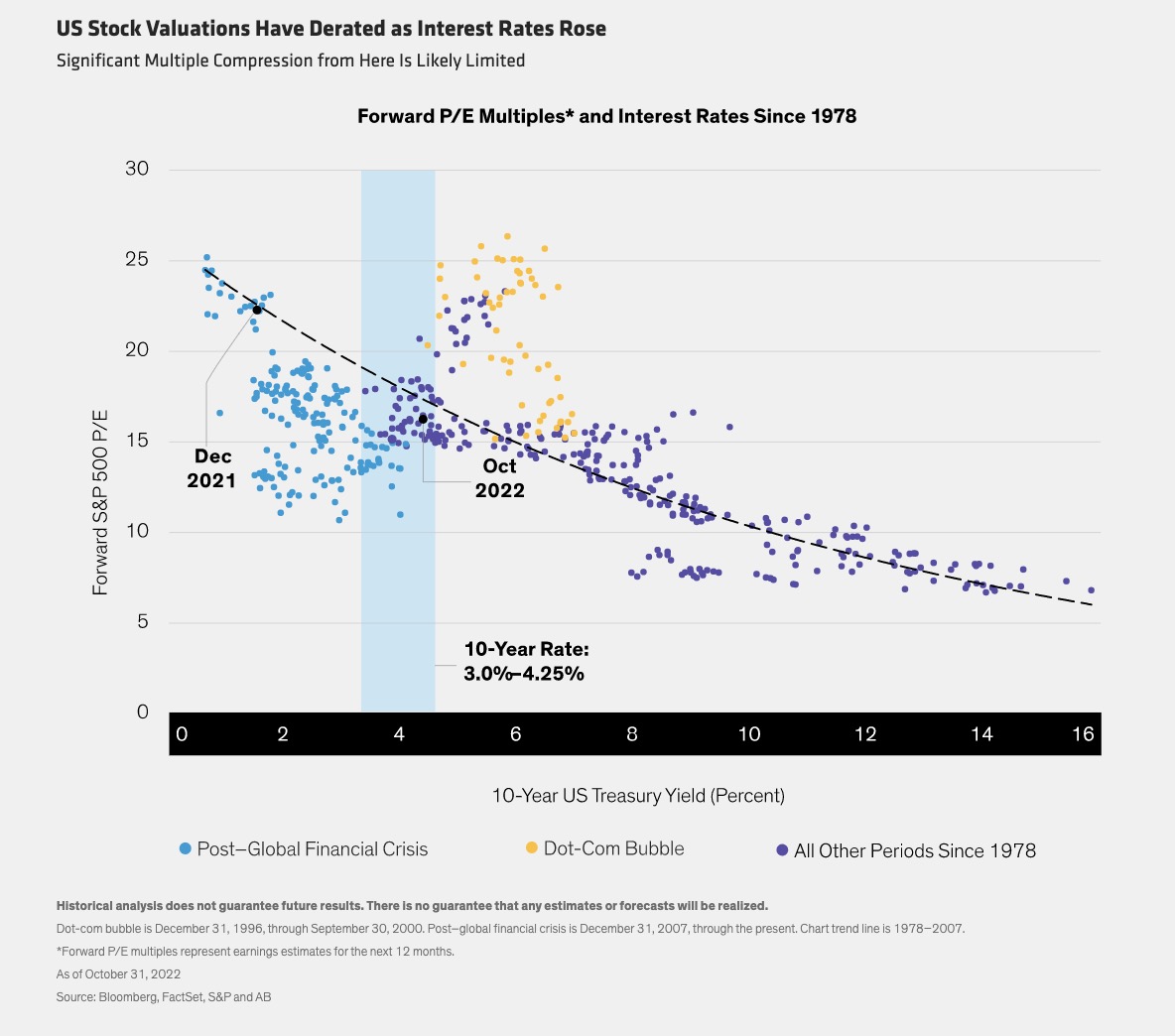

Equity valuations have fallen substantially as central banks hike interest rates to combat inflation.

Does it matter who wins the Senate? It matters a great deal. Read our latest blog regarding midterm elections.

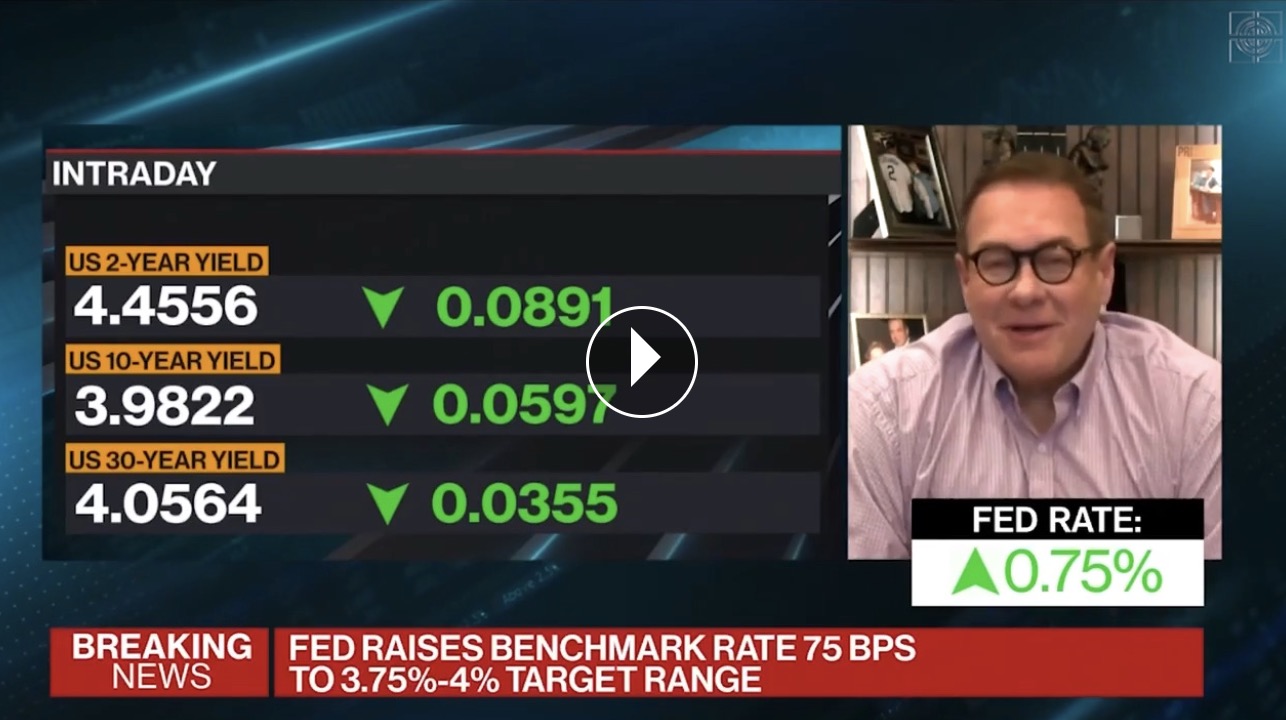

Scott Minerd, Guggenheim Partners Global CIO and Chairman of Guggenheim Investments, joins Bloomberg TV on Fed Day.

The Federal Reserve’s November statement included dovish language, but Fed Chair Powell warned investors not to expect the Fed to stray from its full focus on fighting inflation.

This is now the third consecutive quarterly letter in which we express a cautious stance toward both the global economy and financial markets. A

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

What are the implications of strategic asset allocation, the dynamics of public and private credit, tech-driven megatrends, and more?

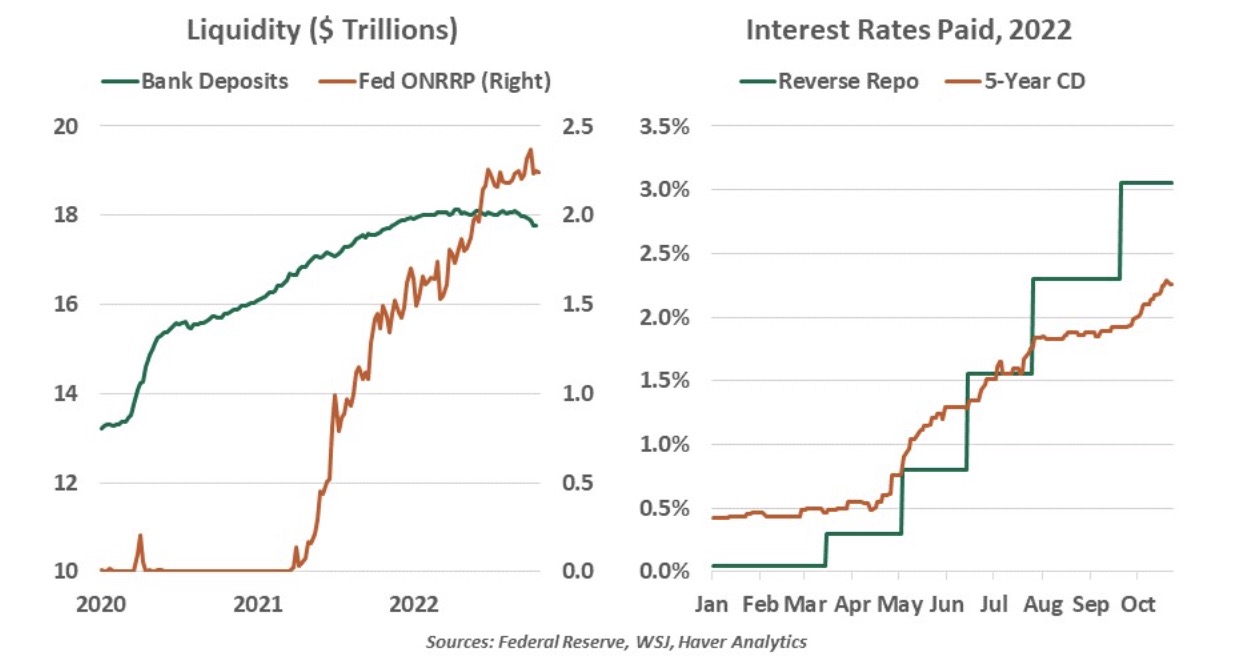

The Fed’s next crisis is already brewing.

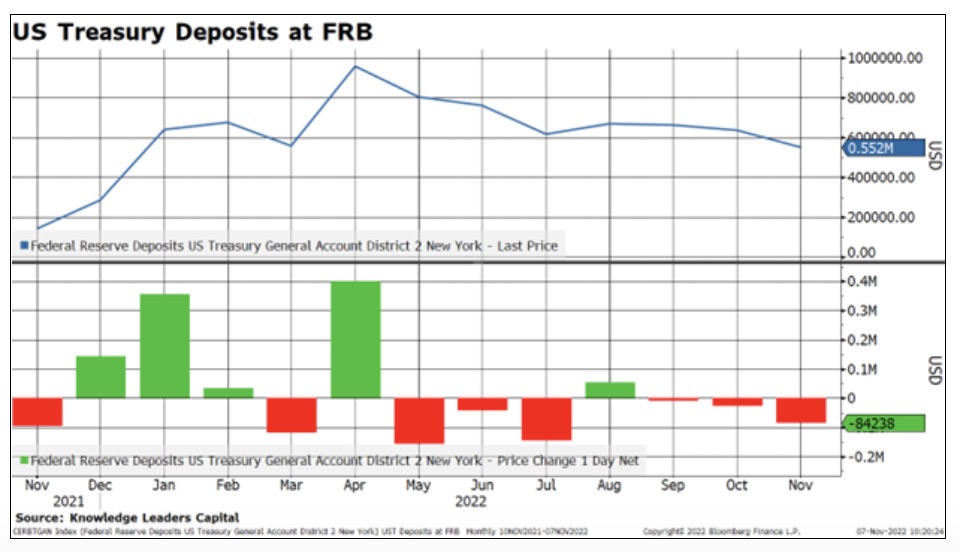

The Fed needs to carefully mop up excess liquidity to avoid funding stress.

The Fed continues to raise interest rates to try and fix the economy and bring down inflation.

Markets hoped for a dovish Federal Reserve “pivot,” but got a hawkish surprise instead.

The Federal Reserve plans to keep raising rates at future meetings, but at a slower pace than it has for the last four meetings.

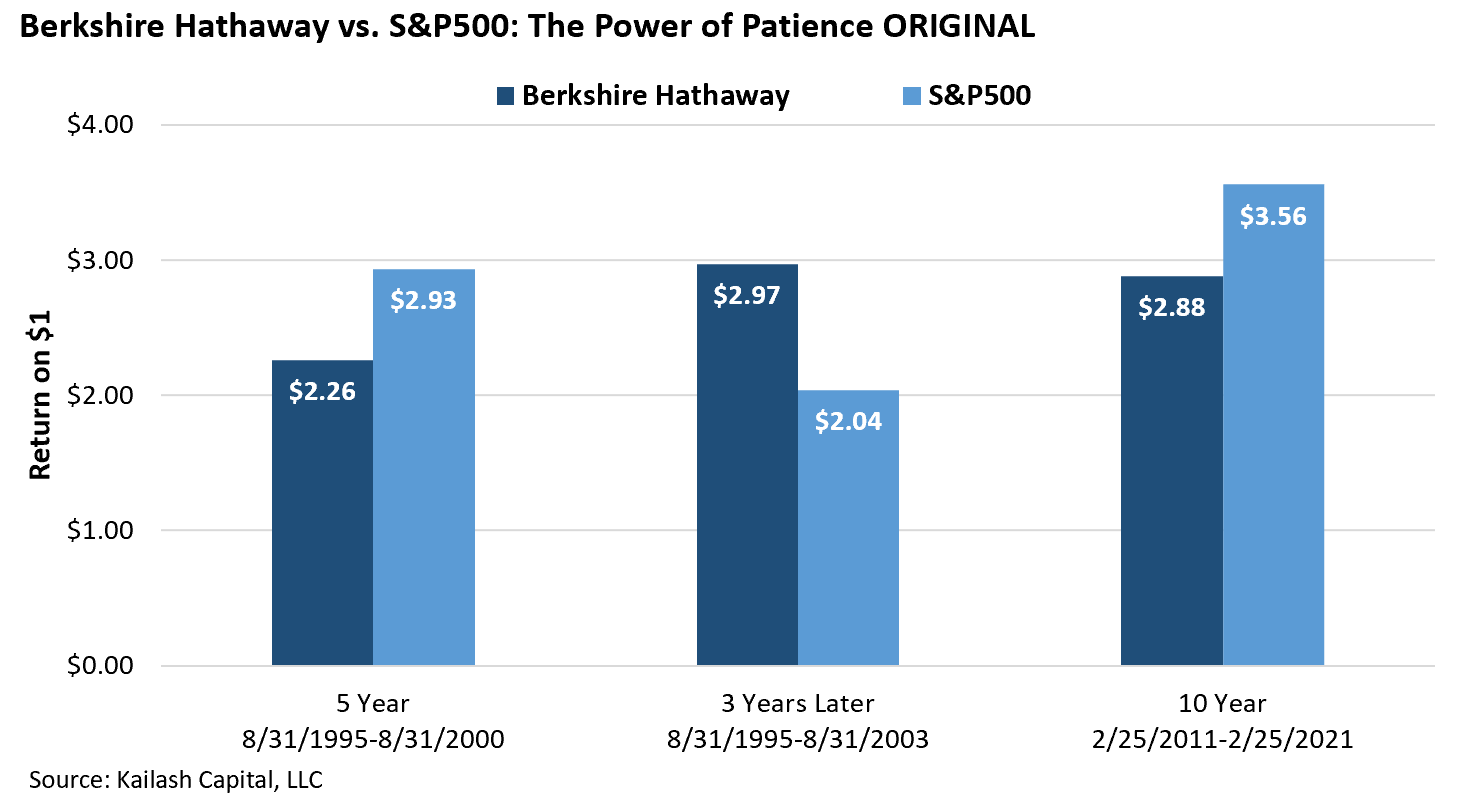

In 2021, enthralled by rank stock speculation, the media returned to a familiar refrain that occurs every time there is a bubble: that Warren Buffett is over the hill and has lost his touch.

Although the economy is showing signs of slowing down, inflation has remained higher than expected.

U.S. equities finished lower with the Dow whipsawing within a more than 900-point range following the Fed's monetary policy decision.

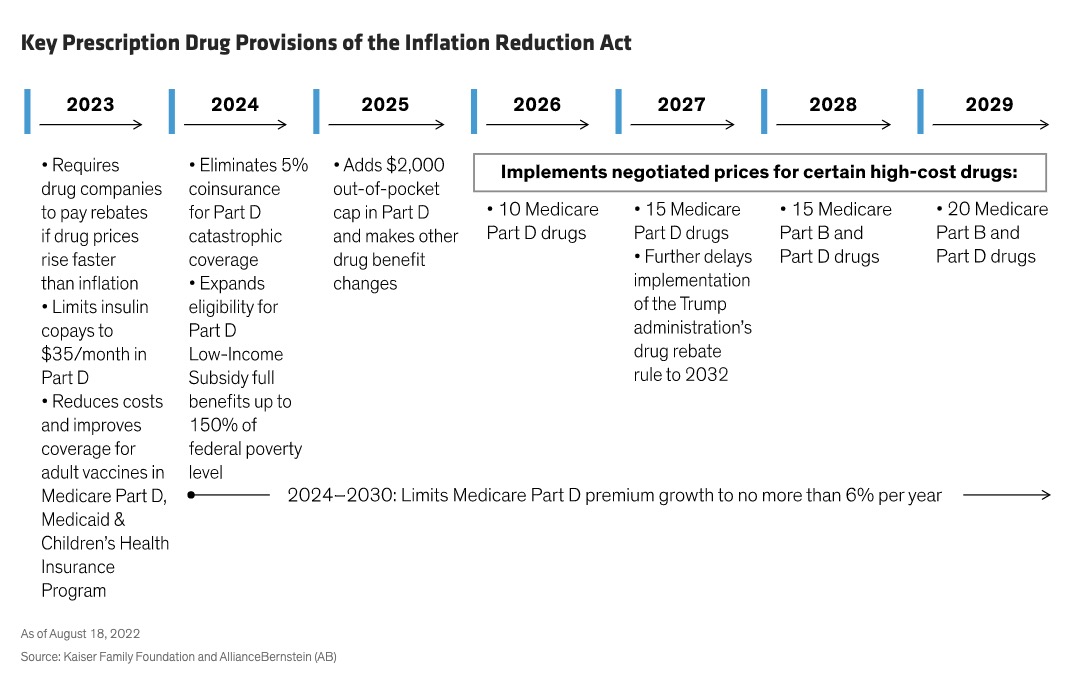

The cost of prescription medicine is a constant strain for many Americans.

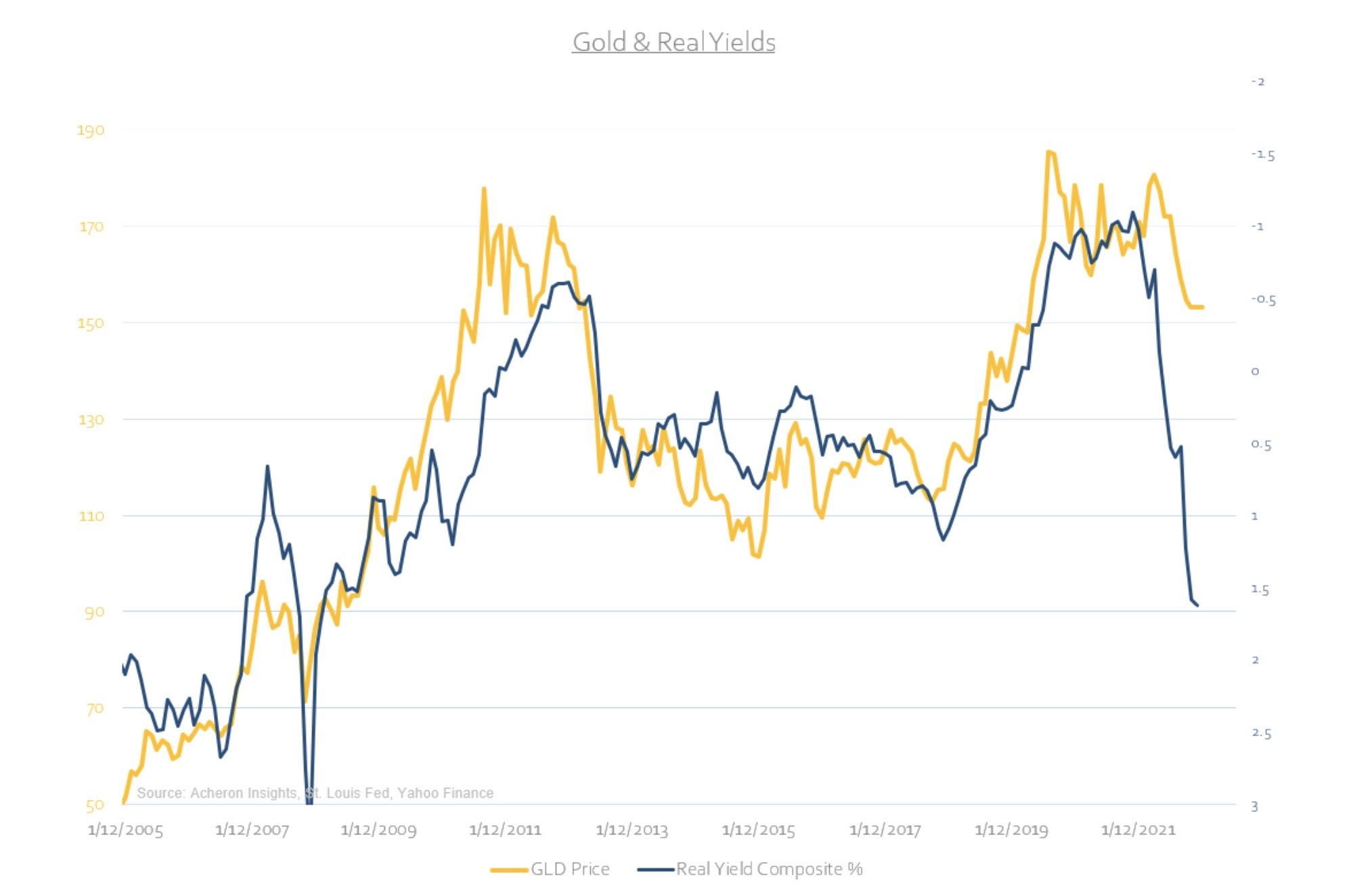

The gold market enters trading for the month of November on a losing streak.

Rising and positive real yields continue to be a major headwind for gold over the short-term.

Gone are the days when China could point to soaring real-estate prices and rising incomes to justify endless new construction.

If you were walking down the street and saw a $100 bill just sitting near the curb, would you pick it up?

This morning I had to laugh when I saw an email that read, “Winter Is Coming – Owning Puts Is Not Enough.”

After nearly three years of the economic and financial market distortion due to COVID lockdowns, money printing, and massive government borrowing, some of these distortions are subsiding

We see central banks on a path to overtighten policy.

Americans will vote in the midterm elections next Tuesday.

“If the Fed loses its independence, the age of magic money could end in catastrophe”.

U.S. equities are declining, struggling to continue the past two week’s positive momentum.

On Thursday, October 21 stock plunged following a sharp rise in consumer prices.

Is a “lost decade” ahead for markets? Stanly Druckenmiller believes that could be the case.

Governments will have to resist the temptation to address stagflation with stimulus.

The uncertainty of a looming recession and high market volatility makes almost all investment options look doubtful as investors search for safe and reliable investment tools.

The U.S. economy is weak, as GDP numbers in both the second quarter and the third quarter have shown. The fundamental reason why the U.S. economy grew 2.6% during the third quarter of the year was because Net Exports, which is exports of goods and services...

Russ Koesterich, CFA, JD, Managing Director and Portfolio Manager, of the Global Allocation team discusses whether markets have bottomed or not.

Equity investors are trying to figure out whether steep share-price declines have led to attractive valuations, given mounting threats to fundamental business performance. The answer varies from company to company and requires an active equity investing approach to separate winners from losers.

In 1990, a new tech start-up was spun out of Apple to invent the future.