Inflation, instability, interference, these are the things that try our souls (to paraphrase American patriot Thomas Paine). They’re also the things that can make one think twice about keeping their wealth in dollars.

GMO 7-year asset class forecast: 3Q 2022.

The difficult capital markets saga of 2022 continued through the third quarter with few safe harbors as rates rose and growth slowed.

From an investment standpoint, aggressive regime shifts like the current one often create price dislocations as allocators restructure their portfolios, according to K2 Advisors.

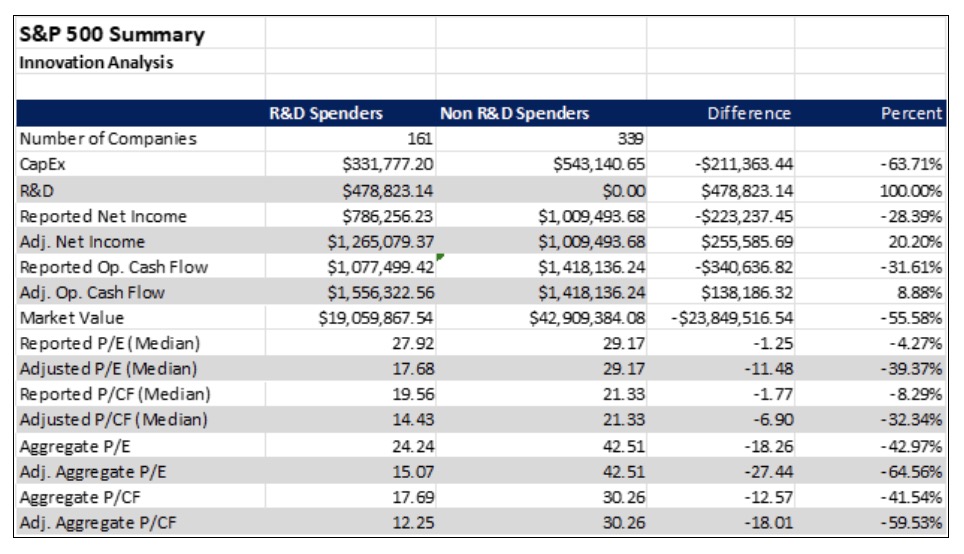

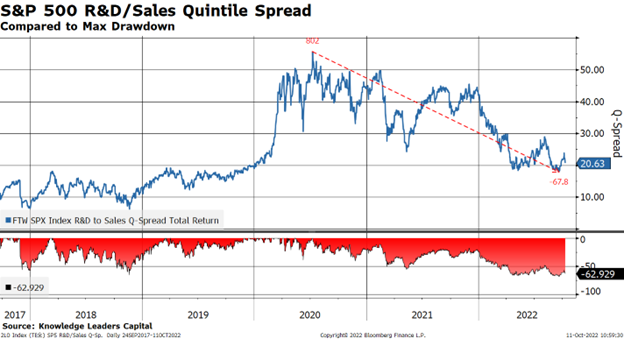

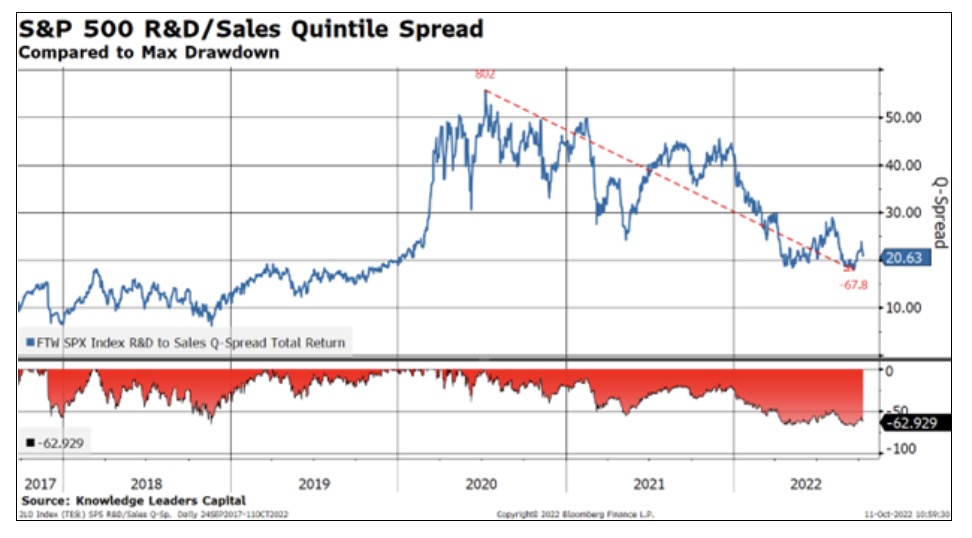

While many perceive the S&P 500 Index to be a broad innovation-heavy index, in a way it is and in a way it isn’t.

When it comes to elevating the “customer experience” to improve client satisfaction and results, today’s family offices could learn a thing or two from Starbucks.

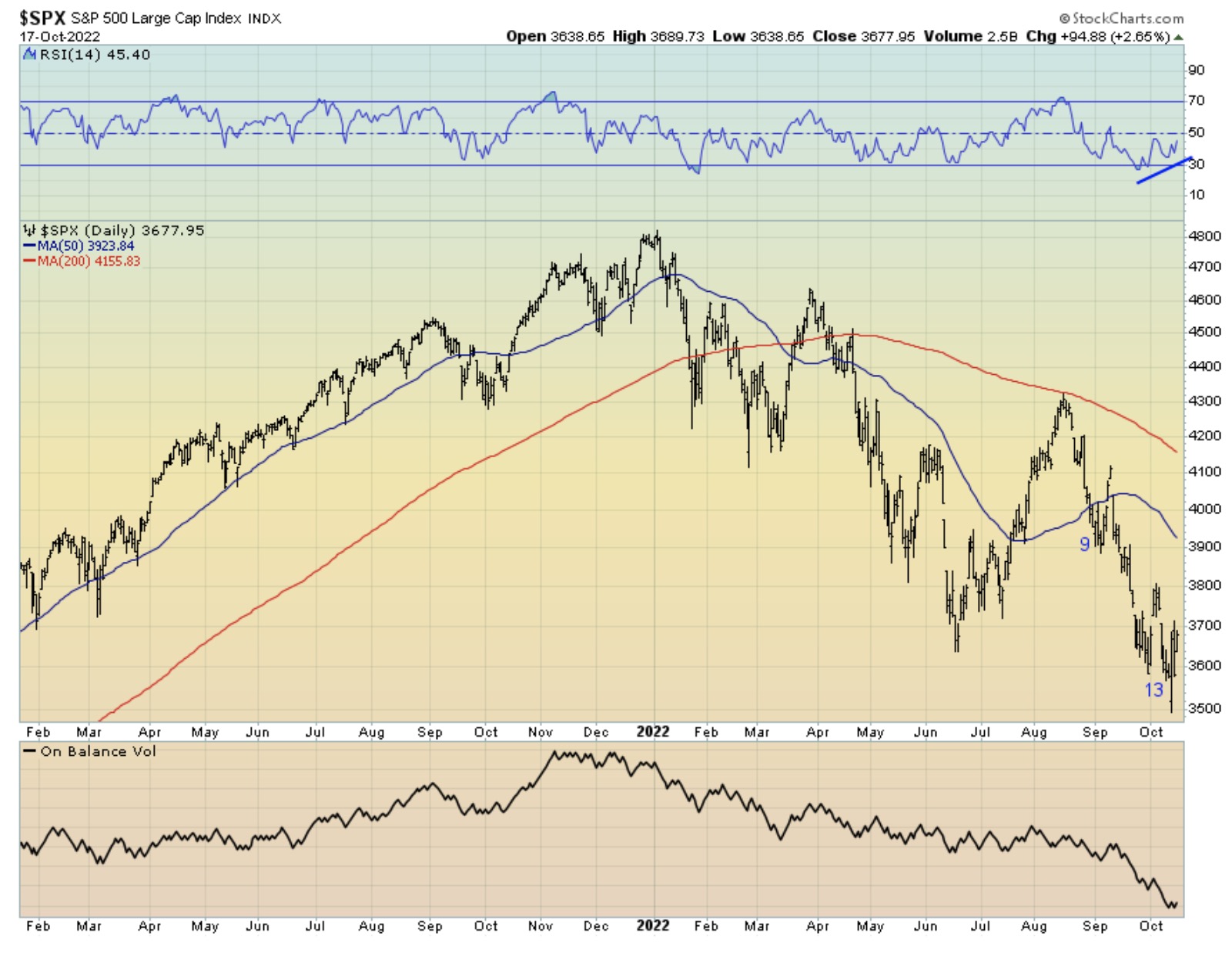

We are at the point in this nasty bear market where those who are buying the glamour tech stocks of the last ten years (on the way down) are at a crucible.

A new Money Metals client reported to us significant trouble retrieving of his silver American Eagles which were supposed to be held for him in a segregated storage account at another prominent bullion dealer.

Investors may have to wait until the Fed’s done tightening for equity market fortunes to change. History suggests that next bull market may not start until both inflation and valuations are again low.

As has been the case in recent weeks, the stockmarket finds itself in a position where various technical factors, market internals, positioning and sentiment are suggesting this sell-off may be overdone and a short-covering rally due.

The Nobel Prize in Economics was recently awarded to former Federal Reserve Chairman Ben Bernanke, as well as professors Douglas Diamond and Philip Dybvig, for their work on understanding the role banks play in the economy, especially during a financial crisis.

The world is in a very different macroeconomic position today compared to the prior forty years.

U.S. equities are beginning the new week sharply higher, getting a boost from the U.K.'s decision to abandon nearly all its tax cut plans.

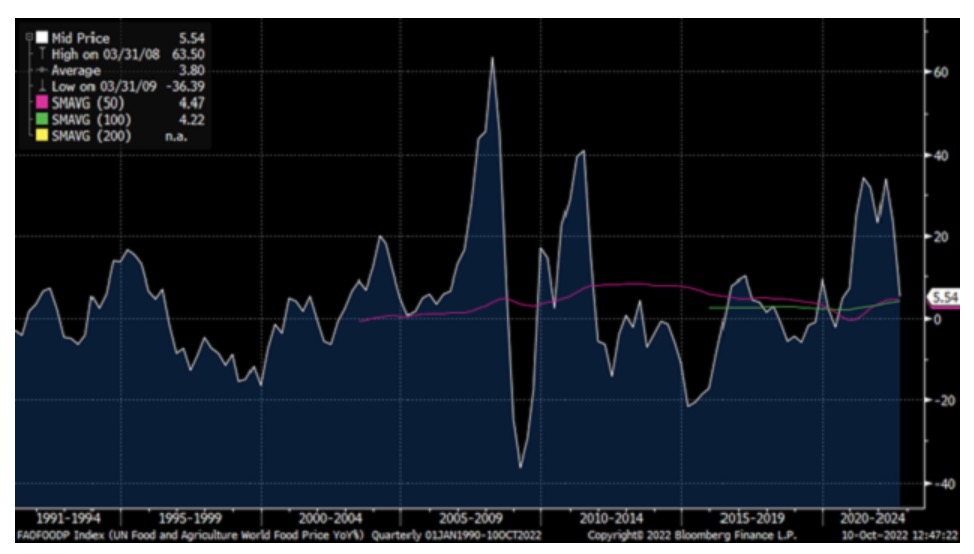

Renewed increases in energy prices come at a bad time in the battle against inflation.

Is this the “Superbubble’s Final Act?” Such was a fascinating piece of commentary recently from Jeremy Grantham, famed investor and co-founder of GMO.

Readers of a certain age will remember Carnac the Magnificent, Johnny Carson’s recurring alter ego.

In 1987, Sports Illustrated, the preeminent sports periodical of the time, predicted the Cleveland Indians would win the American League pennant in its baseball season preview.

Inflation concerns on Friday once again pulled the rug from under investors struggling to find their footing as the Federal Reserve's battle against rising consumer prices shakes the economic terrain.

S&P 500 Introduction 2022 has been a bad year price-wise for the stock market as measured by the S&P 500. However, I contend that is not enough to simply know that the market is down, it is even more important to know why.

2022 has been a stormy year for bond investors, and the forecast calls for more of the same. We address today’s biggest investment challenges—from persistent inflation to rising rates to a looming recession—the silver linings of higher yields, wider credit spreads, and strategies for navigating bad weather.

When markets are challenging, your clients look to you to help manage their expectations as well as their hard-earned money.

Millennials were more comfortable with the stock market this year, a May survey found. We explore the outlook for equities through a generational lens.

Core inflation in the U.S. outpaced expectations for September and may fortify the Federal Reserve’s hawkish resolve.

A couple of weeks ago, in our quarterly strategy report, I argued that it appeared that innovation had bottomed.

Digging in a little deeper, we sifted through this first quintile of the S&P 500 for other insights.

Is a recession lurking around the corner in 2023? If so, how might it impact defined benefit (DB) plan sponsors—and what steps, if any, should they consider taking?

Sandpiles can be fun. Nothing beats taking kids to the beach (or being a kid!) and watching their creativity blossom into all kinds of magical shapes. The problem with sand construction is it doesn’t last. I have it on good authority that building your house on the sand probably won’t end well.

As new inflation data pushes the Fed toward continuing with rate hikes, precious metals markets are struggling to make headway.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

You might be surprised to learn that despite the devastation, we do not expect Hurricane Ian to have a material credit impact in Florida.

The Northern Trust Economics team shares its outlook for growth, employment, inflation and interest rates.

In August 2020, as the global pandemic was straining emerging countries’ ability to make debt payments, we published a white paper – “Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief” – introducing the concept of “sovereign coco bonds,” a way for countries to structure bond agreements to allow for more flexible policy options in the face of a crisis.

2022 has hit investors with an unprecedented 1-2 punch of sharply negative returns in both the equity and fixed income markets, but our Strategic Income team feels the selloff has created attractive opportunities in high yield bonds.

Senior Sovereign Analyst Jon Levy tackles three big questions on the Bank of England's recent operations.

Medical Properties Trust (MPW) claims to be the second largest nongovernmental owner of hospitals in the world.

After enjoying a long period of deflationary conditions, the global economy is being pushed by a wide range of forces toward a new and more difficult equilibrium.

What I want to talk about today is this moral panic we’re having about inflation.

The strong dollar remains a risk to corporate profits and asset prices as the impact on the global economies grows.

The Fed’s inflation-fighting efforts have resulted in a stronger dollar relative to most other major currencies.

U.S. stocks are mixed and subdued as the markets digest another hot inflation report in the form of the September Producer Price Index.

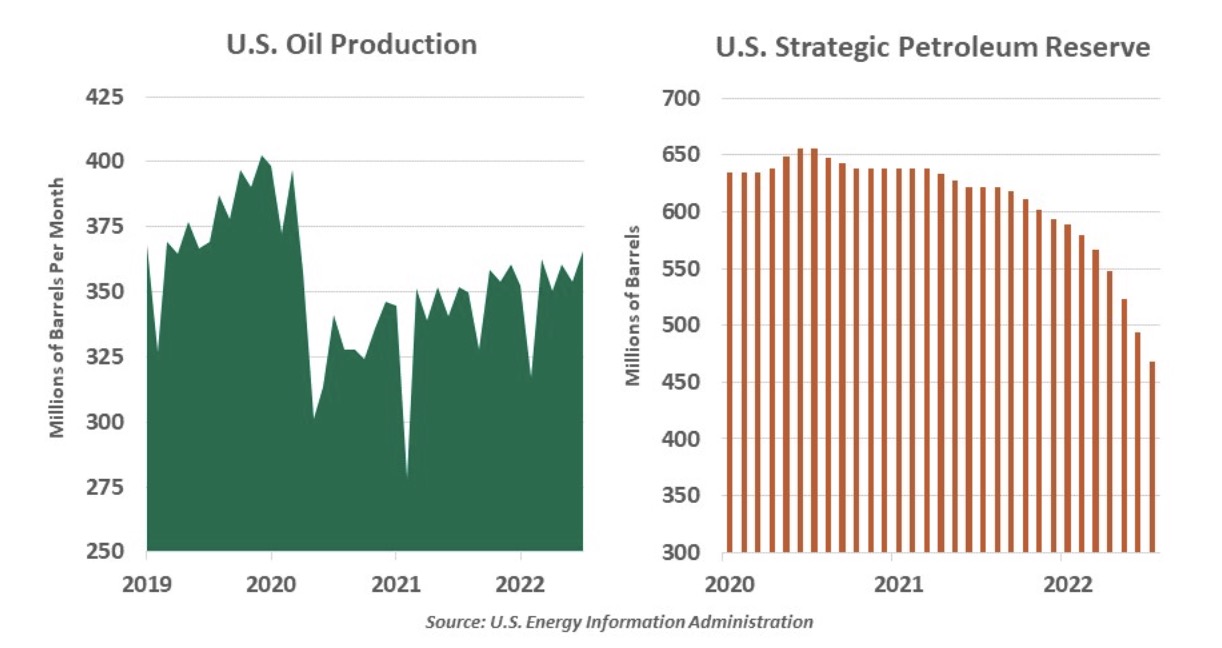

The OPEC+ plan to curb oil production complicates the global economic, inflation, and geopolitical outlook and will likely lead to higher prices for key commodities.

"Carry on!!" was the gruff but oh so welcomed command screamed at me by Marine drill Sergeant Jo Quinn Cruz in October of 1967.

A couple weeks ago, in our quarterly strategy report (see: QSR-Has Innovation Bottomed?), I argued that it appeared that innovation had bottomed.

Robert Leroy Higgins, owner of precious metals dealer Argent Asset Group and the First State Depository (FSD) in Delaware, is in hot water with the Commodities Futures Trading Commission (CFTC).

The era of “TINA”—short for “there is no alternative” and describing a phenomenon where bond yields were so low that many investors felt they had no choice but to invest in stocks, even at stretched valuations—has given way to a market where they can “pay attention to the yield(s).” Or “PATTY,” for short.

When you look at expectations for corporate earnings for the third quarter, you get a bunch of mixed messages.

Cannabis stock Innovative Industrial Properties Inc. (IIPR) claims to be “the leading provider of real estate capital for the regulated cannabis industry.”

U.S. equities are mixed as investors await this week’s highly anticipated September inflation data.

It is as though the finance world decided to take a page out of the music industry's book by recycling a melody with only slight variations.

The World Bank should be a major vehicle for crisis response, post-conflict reconstruction, and, most importantly, for supporting the huge investments necessary for sustainable and healthy global development.

We do not expect the current environment of weakening economic growth to dislodge the long-term staying power of our investment themes and have also taken great care to try to insulate against the most pernicious risks that inflation poses to equity investments.