The secrets for a blueprint for young investors are: Start young. Be disciplined, do it regularly. Focus on what your needs are and what your goals are.

The members of the Bank of England’s Monetary Policy Committee (MPC) are probably not intimately familiar with Taylor Swift’s back catalogue. If they were, Swift’s hit “Cruel Summer” may have been ringing in their ears when cutting rates today for the first time since March 2020.

Once again, the Fed kept rates unchanged at the July FOMC meeting. As a result, the Fed Funds trading range remains in the 5.25%–5.50% band that was introduced exactly a year ago and still resides at a more than 20-year high watermark.

Advisors and investors that want to try to outperform can still gain some diversification benefits using concentrated ETFs.

Jeff Bezos’ wealth slumped by more than $21 billion after Amazon.com Inc. said it planned to continue spending big on artificial intelligence even at the expense of short-term profits.

Municipal bonds extended their rally on Friday after a lackluster jobs number cemented expectations that the Federal Reserve will start cutting interest rates by the end of its next meeting in September.

While election news dominated July's headlines, small-cap stocks had their best monthly performance relative to large-cap stocks since December 2000.

Wall Street banks are calling for aggressive interest-rate cuts by the Federal Reserve based on the latest evidence that the labor market is cooling.

We have been talking about resiliency-driven inflation for the past several weeks. As the US and its Western allies realign supply chains to strengthen economic resiliency, the cost of certain goods and commodities will go up.

In markets and economics, you sometimes have to hold two thoughts in your head simultaneously — an important lesson on a day in which the US unemployment rate unexpectedly surged to its highest in nearly three years.

Global investors are gobbling up bonds that can be turned into stocks, feeling good about the prospects and return potentials of smaller companies.

Cassandras seldom get opportunities to be right about two disasters. Even the original Cassandra scored no notable victories after predicting the fall of Troy. But when a seer who successfully called one catastrophe warns of another coming, you might want to listen.

Amazon.com Inc., Microsoft Corp. and Alphabet Inc. had one job heading into this earnings season: show that the billions of dollars they’ve each sunk into the infrastructure propelling the artificial intelligence boom is translating into real sales.

The bond-market rally escalated Friday after a report showed that job growth slowed sharply last month, further stoking speculation that the Federal Reserve will start aggressively cutting interest rates to keep the economy from stalling.

The violent rotation from Big Tech plunged the Nasdaq 100 Index into correction territory, wiping out more than $2 trillion in value in just over three weeks, as traders unwound bets that had been minting money for over a year.

Some investors who had previously expressed devotion to the largest digital currency propelled it higher last month.

ETFs had a big July, with some leading strategies lifting their YTD inflow totals behind strong July numbers.

Like you, we have read countless comparisons between today’s enthusiasm for all things AI and the top of the TMT bubble in 2000, with the implication being that stocks are on thin ice.

The central bank’s latest policy statement and Chair Jerome Powell’s remarks suggest that an initial interest rate cut could come as soon as September.

The Federal Reserve noted that inflation is moving closer to its 2% target after electing to hold rates steady at its July FOMC meeting.

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates in major markets.

Coming into this earnings season, one of the most intriguing questions was how well the consumer-facing companies would be able to maintain their pricing power. The new algorithm for success is a bit more complicated than “raise prices by x.”

A fifth of Americans are on the hook for an 833% jump in the cost to ensure the lights stay on. The folks being paid that premium, mostly electricity generators in this instance, face that most welcome of problems: What to do with a windfall.

In this article, Russ Koesterich discusses factors behind gold’s impressive performance year to date.

Economists Stephen Miran and Nouriel Roubini are making waves by suggesting in a paper published last week that the Treasury Department has actively engineered easier financial conditions by increasing the issuance of short-term bills and, consequently, reducing the share of longer-term notes and bonds, thereby keeping yields lower than they would otherwise be.

The Federal Reserve kept its policy rate unchanged at the July meeting, but left the door open to rate cuts later this year.

With tech stocks making up a substantial portion of broad market indexes, investors may wonder what will happen when the tech rally ends.

Today’s passive index investing requires active choices, as customization and innovations in index funds have resulted in new considerations for investors and the potential for greater control.

Federal Reserve Chair Jerome Powell signaled central bank officials are on course to cut interest rates in September unless inflation progress stalls, citing risks of further labor-market weakening.

Nvidia Corp.’s wild ride this week is headed for the record books.

In mid-July, VettaFi's webcast asked what advisors were concerned about. “Market valuation” topped the list of choices with 56%.

Predicting a labor-market downturn was never an easy task. But unique post-pandemic dynamics are making it even harder for economists to determine whether a recent uptick in the unemployment rate is signaling trouble ahead.

Demand growth is cooling, but evidence suggests that overall fundamentals are still sound.

Reasonable Treasury debt ratios and more than enough buyers put Treasuries in a much better light than is commonly heard.

Could this be the last Fed meeting before rate cuts begin? With inflation moderating and job growth weakening, the Fed prepared markets for a more eventful meeting in September while not committing to anything just yet.

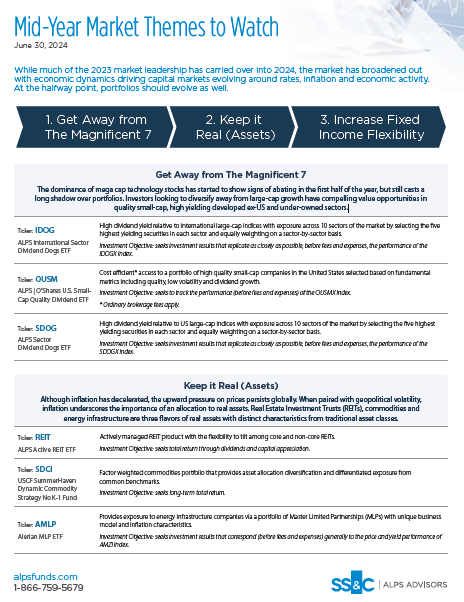

The dominance of mega cap technology stocks has started to show signs of abating in the first half of the year, but still casts a long shadow over portfolios. Investors looking to diversify away from large-cap growth have compelling value opportunities in quality small-cap, high yielding developed ex-US and under-owned sectors.

Jeff and Ron discuss the state of the economy, inflation, the bond and stock markets, and they outline, in broad terms, their current investments.

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. This committee statement is about as close as they get to identifying their method.

Third party custodians provide a critical back-office function for RIAs – and beyond the important job of safeguarding client assets, they have more sway over operations than one might initially expect.

It’s hard to work daily with and for someone who clearly doesn’t like you or want you to succeed.

When dealing with millennials and often with more seasoned investors, it’s important to understand their barriers to acceptance of a boring approach to investing.

Investors will want to see valuations justified by robust fundamentals during big tech earnings reports this week.

Options strategies remain a popular choice with advisors and investors for the benefits they bring to portfolios.

US companies added the fewest number of workers since the start of the year and wage growth slowed, consistent with signs of a softer labor demand.

Private equity has been in the news frequently in the last few weeks, and not in a good way.

Which financial assets a central bank should buy and sell is hardly a novel question. Historically, the US Federal Reserve has focused on shorter-term Treasury securities, but quantitative easing had the Fed buying mortgage securities and quality commercial paper in significant quantities. More generally, central banks often hold gold and foreign currencies.

The US Treasury left its quarterly issuance of longer-term debt unchanged for the second straight time, and maintained its guidance that it doesn’t expect to need increasing issuance of notes and bonds for “several quarters.”

Value — defined by stocks with a low book-to-market ratio — handily beat growth by a minimum of 4% on average annually over the period 1927-2014, although surprisingly with a higher standard deviation. In today’s world, think Verizon versus the Magnificent Seven decades forward.

We are approaching a turning point in policy decisions as the FOMC attempts to walk the fine line of hitting their inflation targets while maintaining a healthy labor market.

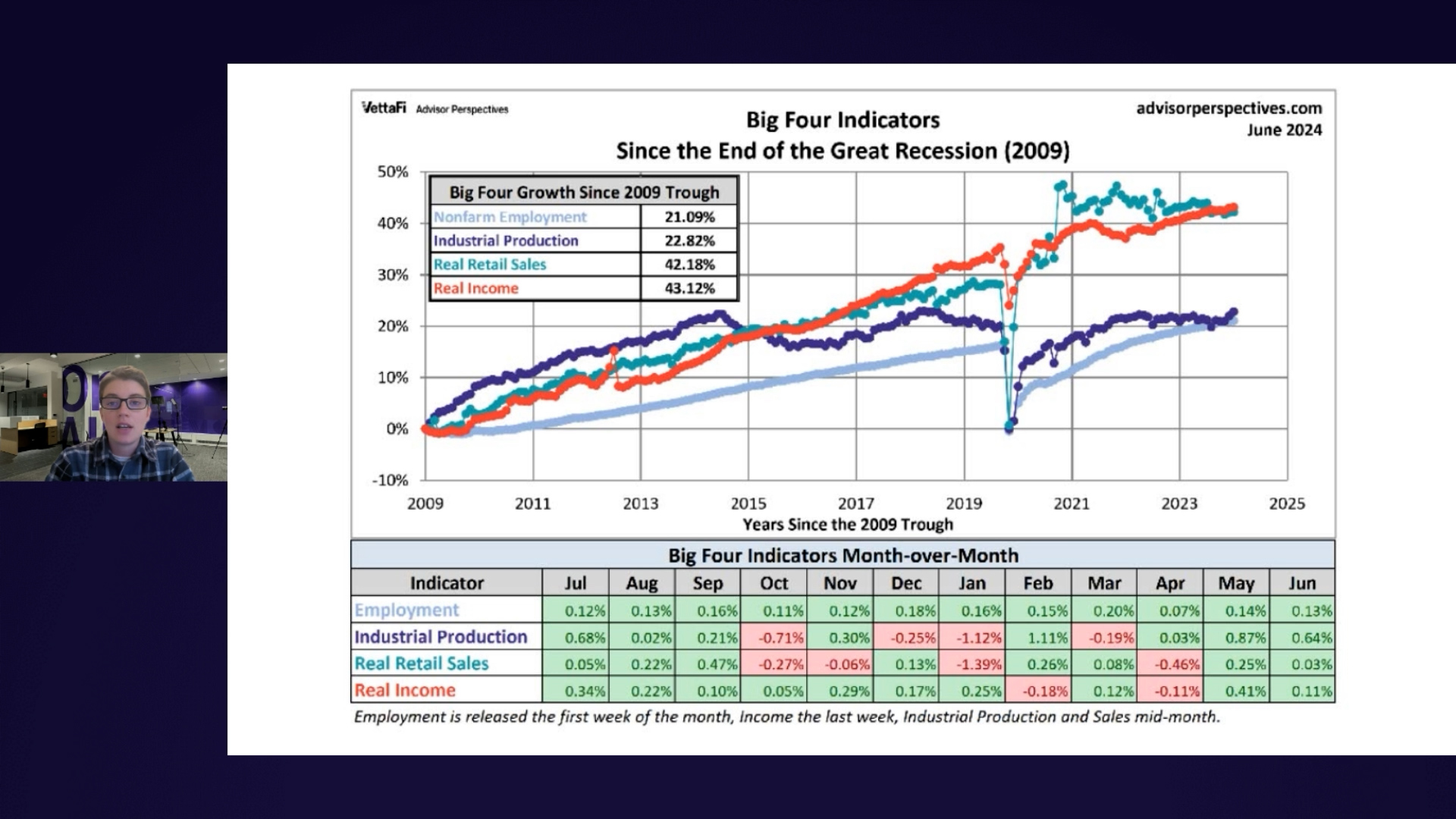

The economic data is coming in very good for markets. Starting with GDP, we observed a modest growth rate of around 2% in the first half of the year. While not spectacular, it’s far from recessionary conditions. This level of growth, with slight inventory accumulation, suggests a stable economic backdrop.