Inflationary pressures from the COVID-19 crisis have been compounded by the surge in commodities prices sparked by the Russia-Ukraine war. In the US, the Consumer Price Index hit 9.1% year over year in June—its highest since 1982. In fact, most major economies are dealing with inflation highs not seen in decades.

On the latest edition of Market Week in Review, Chief Investment Strategist for North America, Paul Eitelman, and Research Analyst Laura Bardewyck reviewed early results from second-quarter earnings season.

Infrastructure has recently seen increased attention as broad equities have been weaker in 2022 due to inflation, rising interest rates, global supply chain disruptions from COVID-19 and the war in Ukraine.

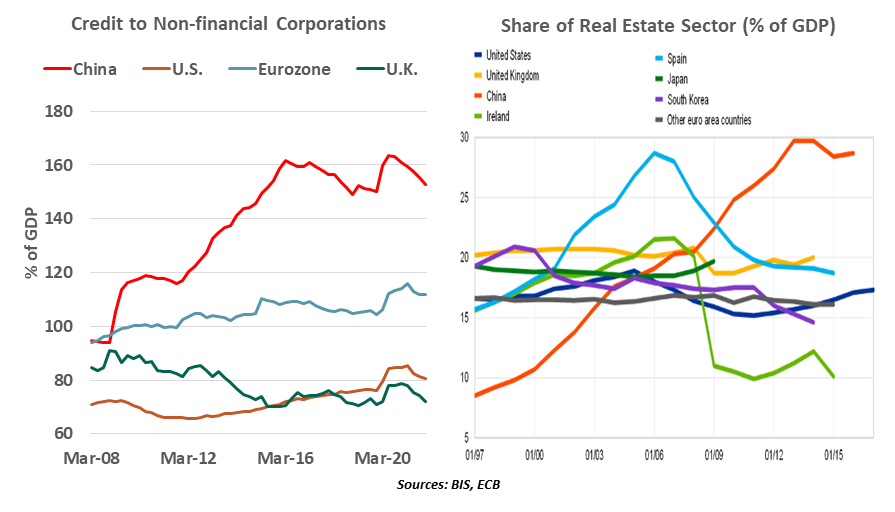

New signs of stress are evident in China's property market.

Since the VPCI W bottom on June 21st, the bulls have taken short term control of the market.

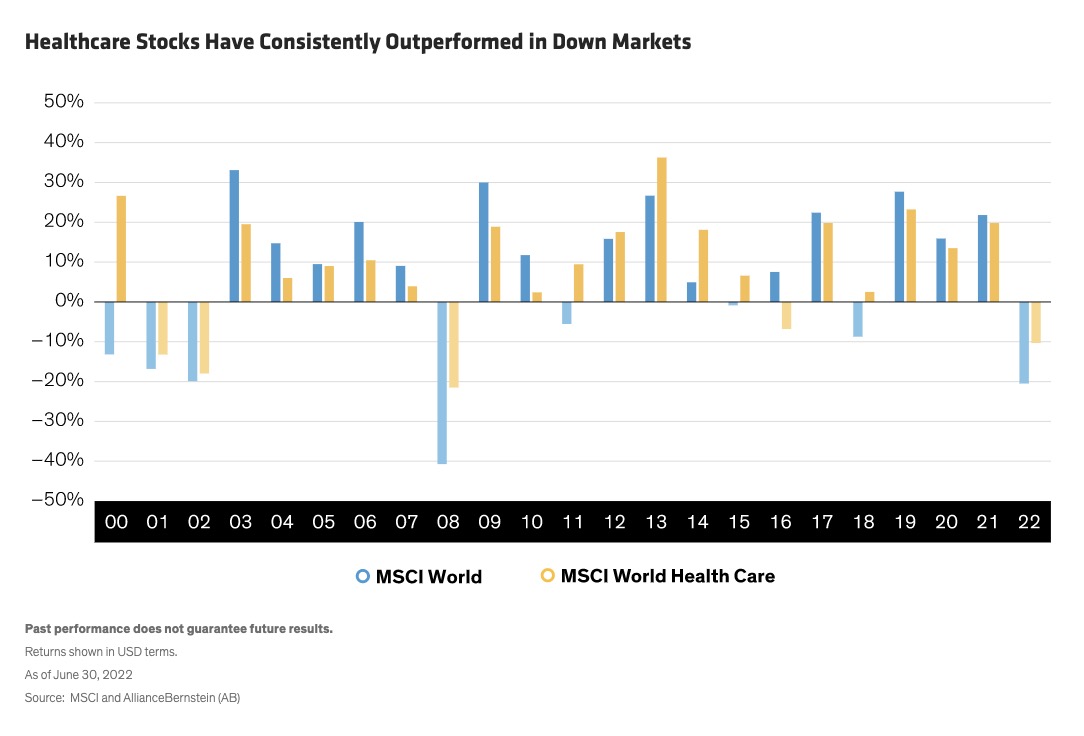

Healthcare has long been considered one of the most reliable defensive sectors—an effective portfolio buffer when equity markets turn volatile.

To many investors, this week’s GDP report is more important than usual.

It’s been a rough couple of months for copper.

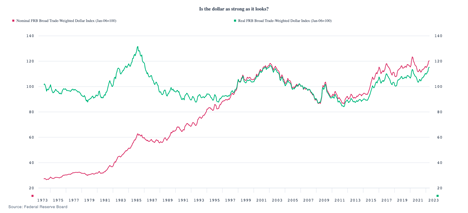

What drove the U.S. dollar's surge, and can it last?

Attracting international investors and securing new trade partnerships while a country is involved in an internal armed conflict is very challenging.

MMT Policy (Modern Monetary Theory), the grand experiment, was tried following the pandemic-driven shutdown of the economy.

Our last two quarterly letters conveyed a cautious attitude regarding both the economy and financial markets. The cautious season persists this quarter.

In our last Advisor Perspectives article we discussed the possibility of a market rally and suggested our favorite way to trade it was Biotech, likely IBB (iShares® NASDAQ Biotech ETF).

During Tesla’s quarterly results webcast this week, Musk admitted to dumping some $936 million of Bitcoin to raise cash out of concern of an economic pullback due to pandemic lockdowns in China.

We can draw a direct line from the Fed’s low rate regime to today’s surging inflation, asset inflation, and income and wealth inequality. Low rates produce asset bubbles which ultimately pop, but not before blowing themselves larger and multiplying into other bubbles. The process that pushed stock prices higher is the same one that is now pushing food, energy, labor, and every other cost higher. Just follow the bouncing ball.

We’ve all heard the famous Yogi Berra quote, “Nobody goes there anymore. It's too crowded.” Investors today seem jazzed up on an opposite but similarly absurd concept: Wall Street thinks it’s a huge buying opportunity because everybody’s too bearish. In his latest Quick Insight, Dan Suzuki analyzes explains seven signs that suggest that investors have yet to capitulate.

Managing Director Justin Takata discusses the technical and fundamental drivers of value in investment grade corporates, and U.S. Economist Matt Bush addresses recession timing and the possible progression of policy.

Throughout the duration of the recent bull market (one of the longest on record) common stocks in the general sense became significantly overvalued.

U.S. stocks are mixed in a subdued session to close out the week, but remain on target for a sharp weekly advance.

At this point, where do we honestly see ourselves on the journey to more and better energy storage solutions?

The current spread differential between European and US corporate spreads have us considering a shift in our thinking.

Equity markets have struggled so far in 2022, but in our view the declines are largely due to “The Great Normalization” – the unwinding of the Covid economy that was defined by excess liquidity, unusually high demand, and extremely low interest rates.

The Fed’s most pressing concerns are to not only reverse its monetary excess and misjudgment of inflation, but also to instill confidence that they will follow important provisions of the Federal Reserve Acts.

One of the headlines I have been asked about recently is the strong dollar. People are concerned about what it means, how it could hurt the U.S. economy, and, of course, how it will affect their investments. Good questions all.

“Desengaño” was noted by one Antonio Garcia Martinez in his most excellent book, Chaos Monkeys: Obscene Fortune and Random Failure in Silicon Valley, as a unique style of Spanish genre painting.

Born in the 1980s, special purpose acquisition companies (SPACs) are growing up. A surge in SPAC activity that started in 2019 only grew in 2020, bolstered by the market volatility brought on by the pandemic – but also by an influx of more serious investors in a previously niche space. By the end of 2021, SPACs had raised $160 billion on U.S. exchanges – a new record that nearly doubled the level of the previous year.

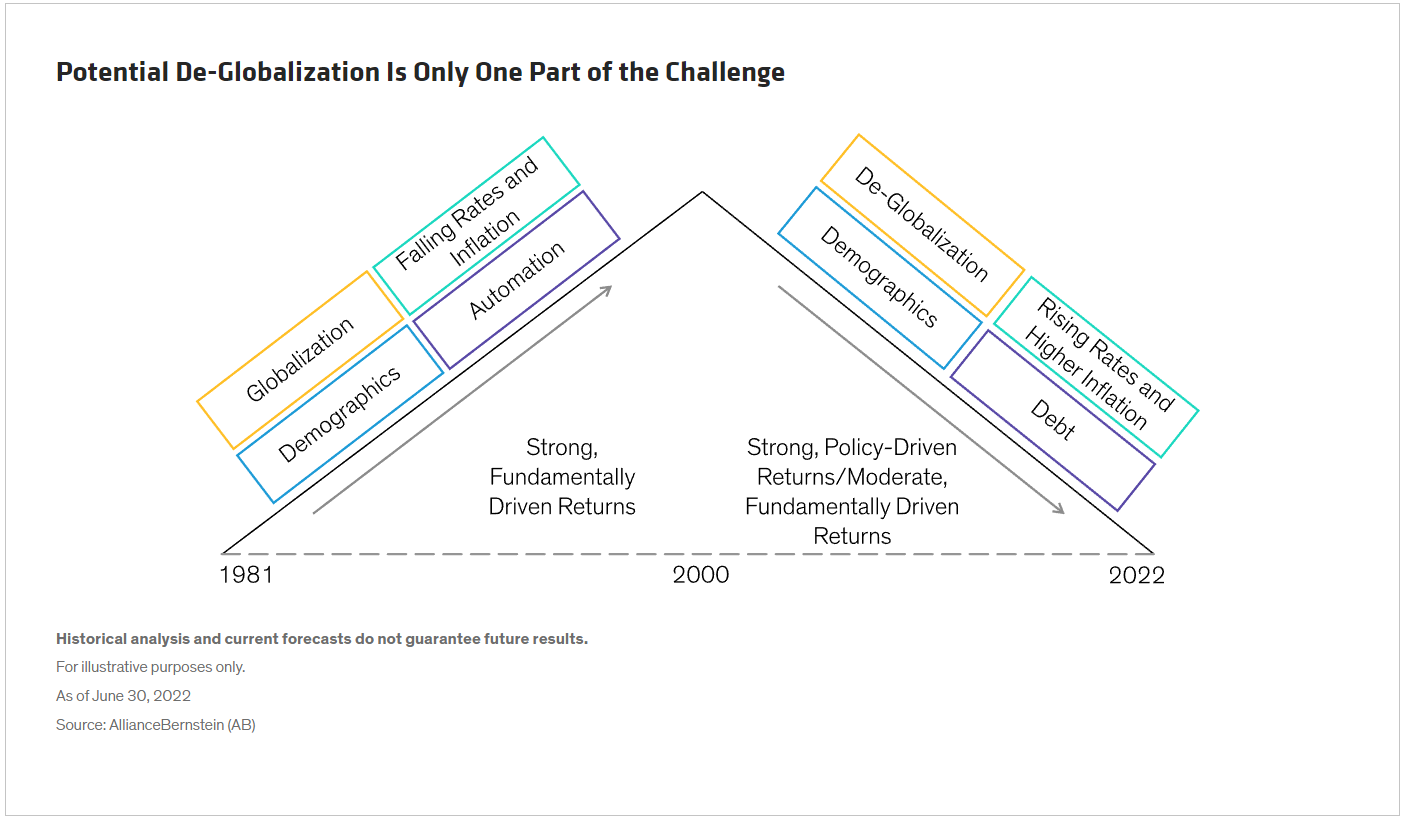

For decades, globalization has been on an inexorable rise, a key pillar fueling economic growth, driving inflation and yields down, bolstering corporate profit margins and supporting an upward climb in market valuations. Over the past few years, though, cracks have started to develop in globalization, as populism has seen a resurgence and trade wars have erupted.

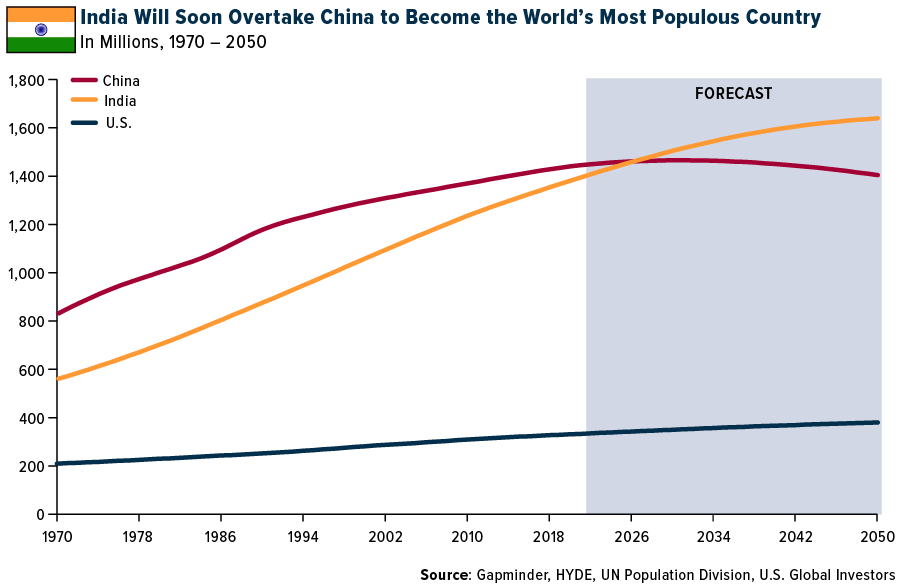

This incredible milestone underscores the need to solve a number of ongoing challenges related to population growth, but it also presents what I believe are some very attractive investment opportunities.

After the June 17, 2022 low, stocks have jumped higher, taking out the 50-day moving average yesterday in the S&P 500. Many are debating whether this is a bear market rally or the reversal of the bruising 6-month decline.

There is much debate about the effectiveness of Western sanctions, the Ukraine war’s implications for markets and the global economy, and what the West’s next steps should be. While there are few good options, some are clearly worse than others.

The business press sometimes likes to say that a recession is a decline of real GDP lasting at least two consecutive quarters. Not so.

As institutional investors, we most often represent risk as annual standard deviation or tracking error. But when we implement changes in our portfolios, the real-time risk happens much faster.

Although an economic rebound in China is underway according to government and private sector data, its economy and stock market may remain volatile.

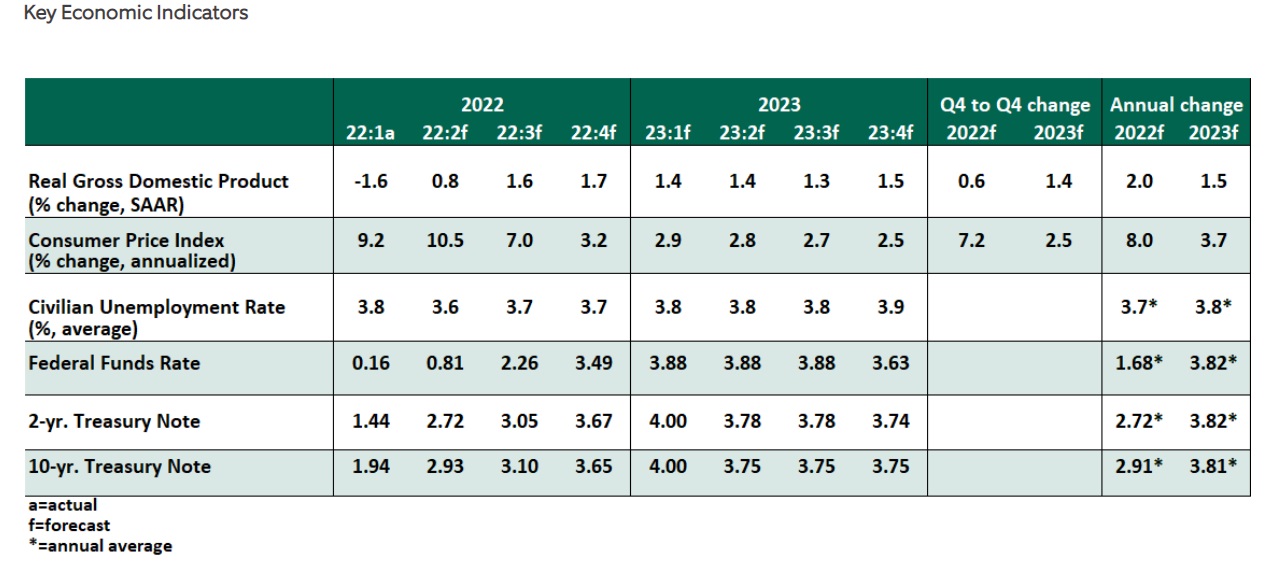

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates.

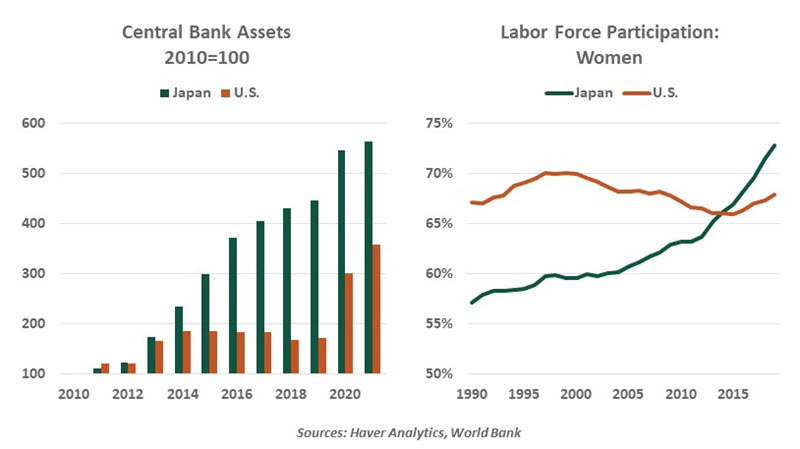

Templeton Global Equity Group explores the legacy of Abenomics, the emergence of inflation in Japan, and finding value opportunities there.

One of the most surprising things to come out of the first half of 2022 was the walloping fixed income investors received from bonds. The Bloomberg U.S. Aggregate Bond Index posted its worst 12-month return in its entire history, which caused many investors to shed exposures, particularly longer-term sectors.

Investors can choose one of two popular scaling methods for carbon emissions comparisons across companies. Our analysis guides investors in making this important decision.

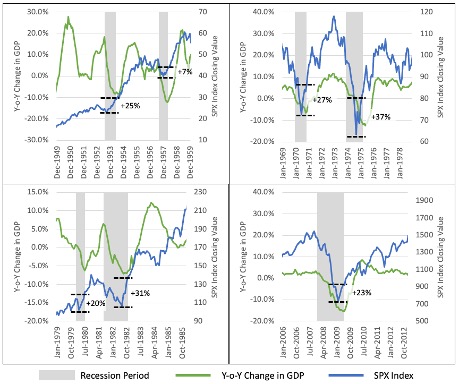

Bad news dominates the headlines. The question for investors is when to become optimistic on markets. Since nobody rings a bell to signify that the market has hit bottom, this commentary looks back at previous recessions to see what history reveals.

Basic economics says that companies can only set prices at a level where the current supply will meet demand. Moreover, looking at prices in a vacuum is also very misleading because it doesn’t account for changes in the firm’s input or operating costs.

With central banks tightening aggressively to beat down inflation, growth is beginning to slow—and the risk of recession is ticking higher. Historically, creditworthiness has soured when growth slows. But instead of bracing for a wave of downgrades and defaults, we think income-seeking investors should embrace the high-yield corporate bond sector.

U.S. equities are seeing solid gains, as the bulls look to sustain the rise today after failing to do so yesterday.

How inflation expectations are formed determines how firmly the Fed must react. If expectations respond to current inflation, they’re possibly “unanchored”—and this makes the Fed’s job harder. Unfortunately, we can’t yet say that expectations haven’t changed for the worse.

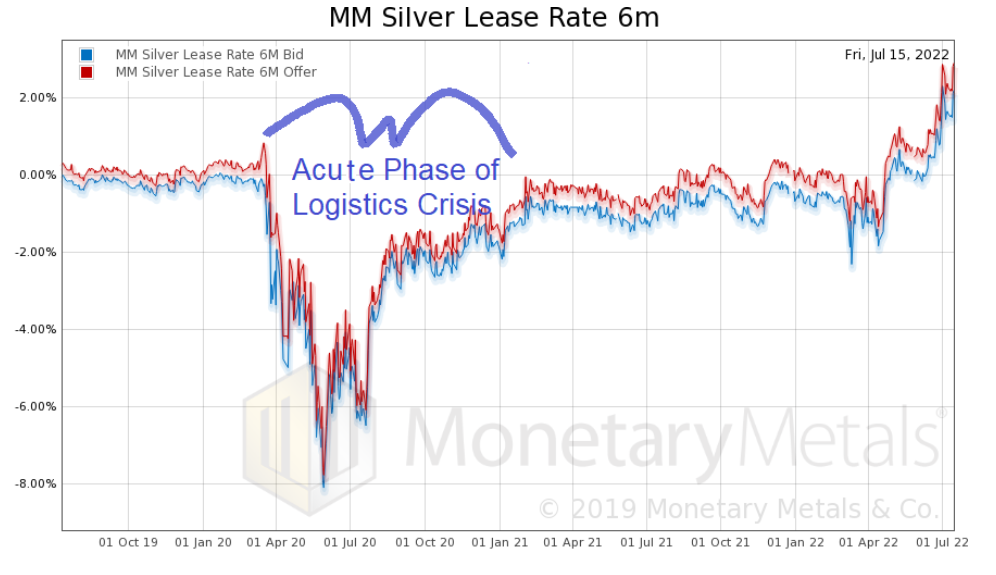

We discuss the recent news of JP Morgan’s spoofing and why the monetary metals are behaving so oddly.

If you follow the financial press, the conventional wisdom has come to the simple conclusion that the way to fight inflation is raising interest rates. Unfortunately, this is just not true.

Shinzo Abe's policies had a substantial impact both in Japan and around the world.

As we’ve hit the halftime mark for the investment year 2022, we are faced with a daunting two-headed monster.

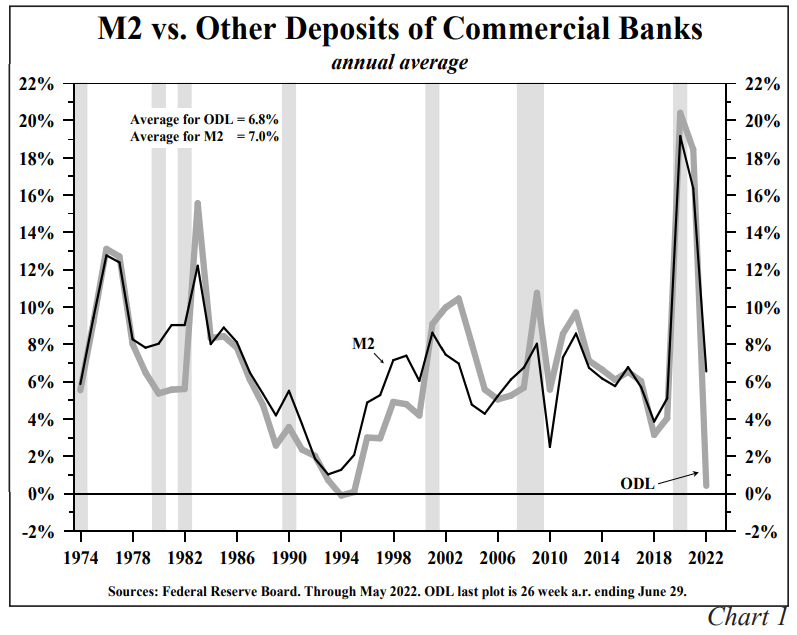

Reducing the money supply will help to curtail inflation.

Despite the Fed’s aggressive tightening policy, we think inflation still has a ways to run, though we remain cautiously optimistic about the economy.

We think the housing sector should hold steady with good structural trends, a potentially bad environment for housing bargains and a scenario for prolonged inflation.

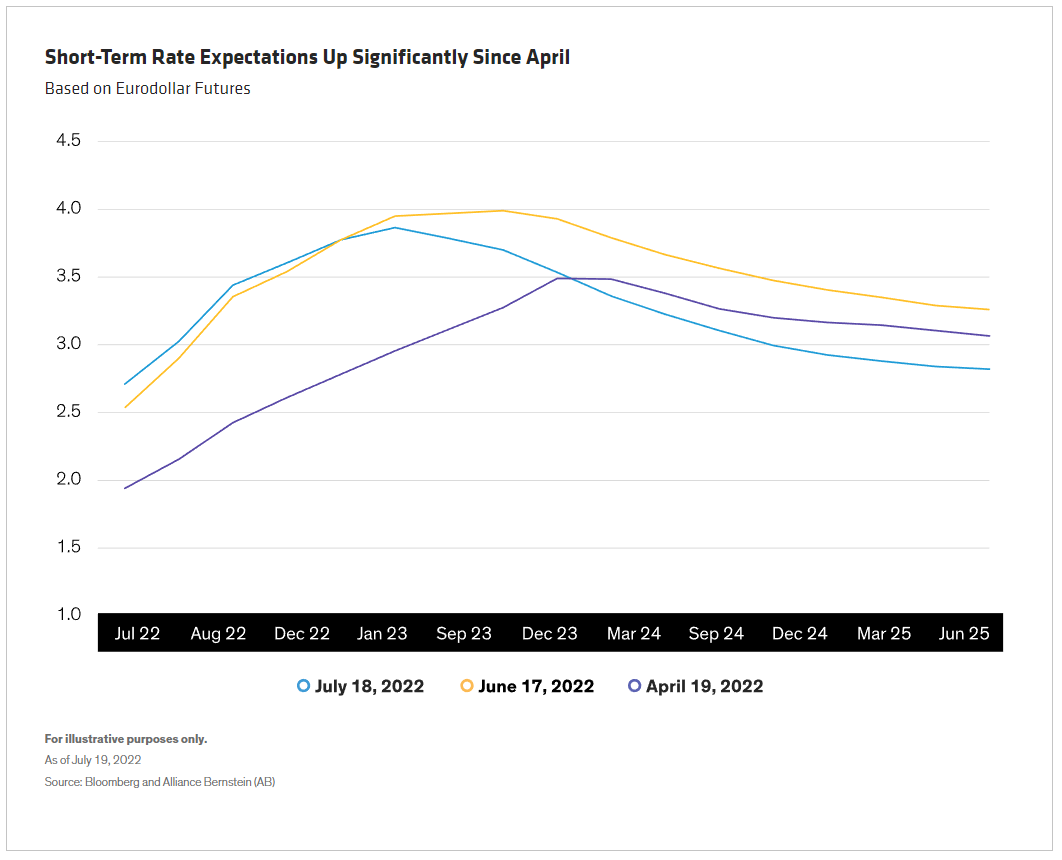

June’s U.S. CPI (Consumer Price Index) inflation data likely set alarms blaring in the minds of Federal Reserve officials.