Despite lingering geopolitical tensions, higher oil prices, and renewed inflation concerns, equities moved higher in April, supported by a strong start to the Q1 earnings season and resilient economic growth.

Decisions rarely stall because people need more time; they stall because people do not want to carry uncertainty by themselves. Writing forces them to do exactly that.

Morgan Stanley and JPMorgan Chase & Co. are leading the process, according to people familiar with the matter. A large majority of the financing is expected to be in the form of debt, with the rest equity, the people said, asking not to be identified discussing private information.

Abel, known as a shrewd operator who’s always looking for ways to improve profits at the $1 trillion conglomerate’s varied businesses, said he had just one thought at the time: The company had already shelled out the money to book the arena for the annual meeting in 2026.

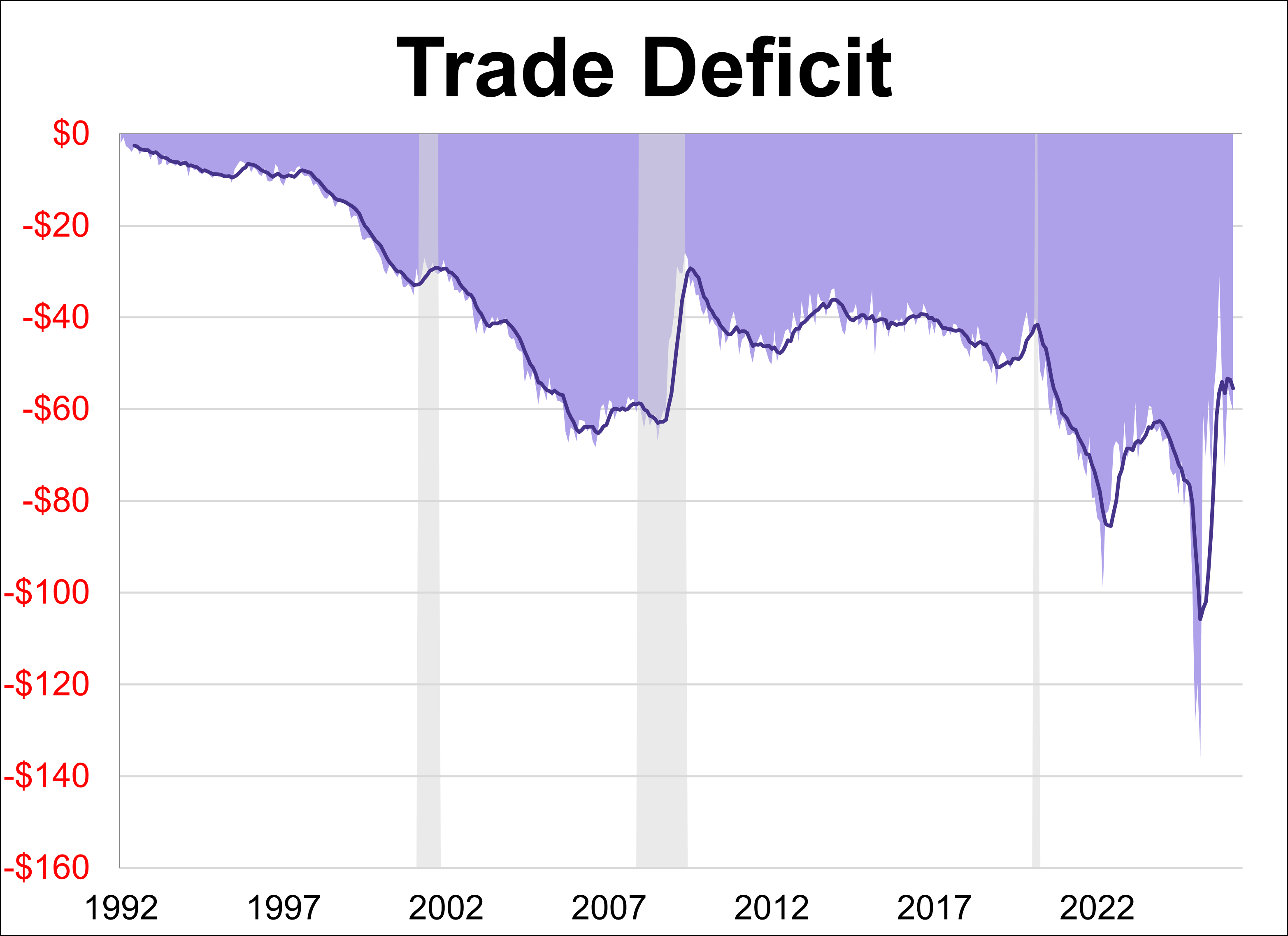

The U.S. trade deficit expanded over 4% in March to $60.31B after expanding nearly 6% the previous month. The latest reading barely missed the forecast of -$61.00B.

Women consistently report that the quality of their relationship with an advisor is their number one driver of satisfaction. They are not just looking for investment expertise. They are looking for partnership and a sense that their advisor understands what matters most to them.

There’s no doubt that Amazon will begin to take market share now that it has declared that its third-party logistics business is here to stay. This move allays concerns among potential customers that Amazon’s offerings wouldn’t be permanent or would take a back seat to its own volume during periods of peak freight.

The rationale is that government should be neutral on asset classes. It should not put its thumb on the scale by favoring some investment types over others. Marcia S. Wagner, founder of The Wagner Law Group, framed this clearly in a presentation at the 2026 Financial Planning Association SHIFT Conference.

An advisor who is involuntarily terminated should not assume the Broker Protocol is off the table. The text supports a good-faith argument that a terminated advisor can still qualify as a “departing” advisor who moves from one Broker Protocol signatory firm to another.

Investors are questioning the staying power of medical technology (medtech) stocks, which have fallen from grace since the COVID-19 pandemic. Yet we think innovation continues to create exciting opportunities in companies that march to a different beat than the rest of the healthcare sector.

While oil prices are likely to remain elevated in the near term, we do not view the current disruption as a lasting supply shock. A diplomatic resolution, or even progress toward one, should help bring prices lower by year-end. Although higher oil prices are a headwind, we believe both the economy and equity markets can absorb the impact with limited damage, as underlying fundamentals remain strong.

It’s no secret that college is expensive. And alongside mounting costs come almost as many strategies for mitigating them. When you need money to pay for college expenses, tapping your Roth IRA is one option you might consider.

There is also a popular notion that bond traders can see the future, that they know what inflation will be or if a recession is coming. But bond markets are often wrong. And they may be wrong now because bond yields are low relative to the risks the economy faces.

The complication is that the ceasefires stopped the escalation without resolving the underlying disruption. The Strait of Hormuz, which carries roughly 20% of global oil supply, remains effectively closed. Oil prices fell sharply on the ceasefire announcements (including the largest single-day decline since 2020), then climbed back above $100 per barrel.

Last week’s data was a good reminder that we are likely in a “resilient but uncertain” phase of the cycle.

It may be a cliche to invoke the pick-and-shovel sellers of the California Gold Rush, but what better way is there to frame what’s happening to Apple Inc.?

Get ready each week with high-conviction insights that go beyond media headlines.

Alphabet Inc. is selling its biggest-ever euro-denominated bond and tapping the Canadian dollar debt market just months after record-breaking deals in other currencies, showing the huge funding needs of its ambitions in artificial intelligence.

Students of game theory often start with a lesson in the prisoner’s dilemma: two agents would gain a better collective outcome by cooperating, but each has an individual incentive to take action that is at their partner’s expense.

April showers came in the form of more inflows raining down on the exchange-traded fund (ETF) market last month. Assets under management (AUM) have now grown to a staggering $14.7 trillion for the year. That’s punctuated by year-to-date (YTD) net inflows of over $636 billion.

What a week this was! On Tuesday, I participated on a panel at the Bitcoin Conference in Las Vegas, where I discussed why Bitcoin miners have a head start in the race for AI compute.

Kevin Warsh wants to make some big shifts in monetary policy at the Fed. Unfortunately, unless and until soon-to-be former Chairman Jerome Powell steps down from his regular seat on the Federal Reserve Board, Warsh will be Chairman in Name Only.

The Federal Reserve held rates steady as expected last week, but the real story was the shift in tone inside the Committee. Three dissents in favor of moving to a neutral bias are highly unusual, and I do not recall seeing dissents on a bias in this way before.

Join the experts at CoinShares for a fireside chat to get all of your questions answered about bitcoin, beyond just the basics.

When it comes to investing, it’s the Wild West out there. Our clients are hearing things from less scrupulous members of the financial services industry that appear true on the surface but are really aimed at separating people from their money.

The same forces that are straining the political marriage across the Atlantic are also creating a long‑term opportunity set in Europe. Advisors should position clients’ capital so that it benefits from that structural shift, while staying disciplined about quality, valuation, and risk.

The poor sentiment toward private credit funds has dragged down many high-quality BDCs, as well as weaker ones. The chaos and bad press surrounding private credit funds are not reasons to avoid BDCs. In fact, we think it’s a reason to consider them.

As the first-quarter reporting season winds down, companies are emerging from an earnings-related blackout. About 40% of corporates are currently in the so-called open buyback window, which is expected to remain open until June 12, according to Goldman Sachs’s buyback desk.

US transportation stocks plunged Monday morning after Amazon.com Inc. announced expanded logistics offerings that will turn it into a major competitor for parcel carriers and air freight companies, and also impact truckers and third-party brokers.

The world’s biggest technology companies posted strong earnings last week, showing that the artificial intelligence boom is alive and well. But in the stock market, investors are getting more granular as they try to divvy up the winners and losers in the AI trade.

Despite repeated wars, equity markets have delivered strong long-term returns, and in some stretches, market performance appears to have coincided with wartime episodes rather neatly. Viewed through the lens of financial markets, the implication seems almost intuitive: wars have not been bad for investors and may even have been supportive.

Robots are coming to the economy. It is inevitable, really, and there is nothing that will stop it. At some point in the not-so-distant future, robots will infiltrate every aspect of our lives, from office work and manufacturing to service work and trade skills, and even your home. Here are some numbers for you.

While the ETF leaderboard continues to be dominated by S&P 500 index-based products, there are many other success stories that are likely being missed. There are now more than 5,100 products for advisors, investors, and even analysts to keep up with. Let’s take a look at some funds that have sprouted in just the last few months.

We’re going to explore what happened at the Fed, and what changes we can expect. Let’s just say it’s not what some are predicting, at least in my humble opinion. Inflation is sadly a growing problem. And that complicates Kevin Warsh’s coming tenure as Fed chair.

This week marks the busiest of the Q1 2026 earnings season with 3,213 companies expected to report. The S&P 500® is projected to deliver its sixth consecutive quarter of double-digit earnings growth at 15.1%, fueled largely by a powerhouse 46% expansion in the Information Technology sector.

April saw a strong rally, which fully reversed the stock market’s losses in March. US markets set new all-time highs, and European stocks came within whispering distance of their all-time highs as well.

Automotive enthusiasts have coined the phrase malaise era to describe U.S. vehicles made from roughly 1973 to the early 1980s. New emissions and safety standards, plus high gasoline prices following the 1973 oil crisis, permanently reshaped the market.

The part of the bond ETF complex that’s growing fastest isn’t that part. It’s the active and outcome-oriented funds — multisector strategies, flexible income vehicles, securitized credit funds, options-overlay products — that charge 0.30 to 1 percentage point and promise more yield, less duration, or both. And the marketing pitch behind them quietly elides something important.

Shell (SHELL NA) announced last week that they are acquiring ARC Resources (ARX CN). Arc Resources is a gas business in the Montney Region of Canada and is a name that the investors of Smead Capital Management are fairly familiar with.

Equity markets are growing more selective around AI exposure this year. In the process, a rotation toward “HALO” sectors deemed less sensitive to AI disruption may be opening an opportunity for investors to diversify beyond AI in value and infrastructure equities.

Like Treasuries and Treasury Inflation-Protection Securities (TIPS), municipal bonds betrayed their normally docile reputations in March as the conflict in Iran stirred increased volatility for normally subdued corners of the bond market.

It’s happening. California looks likely to put a “one-time” tax of 5% on wealth above $1 billion on the ballot in November, and polls suggest it could pass — despite opposition from some economists (not so surprising) and Democratic politicians (more so).

Chuck emphasizes that value, not price, is the key driver of successful long-term investing. Investors should avoid trying to time the market and instead focus on buying quality businesses at sound valuations. If a stock is undervalued, it may present a buying opportunity.

The U.S. economy ended April with mixed signals: steady interest rates and high Fed dissent met persistent, energy-driven inflation. Despite these hurdles, accelerated Q1 growth and rising consumer confidence provided a buffer against ongoing global instability.

In this video, Chuck Carnevale explains one of the most common investor questions: when is the right time to buy or sell a stock? While there’s no perfect answer, he emphasizes that there is a smart, disciplined approach, centered on valuation.

April showed us just how sensitive markets can be to a small number of powerful forces: energy prices, inflation and geopolitical risk. The conflict in the Middle East dominated headlines, with a ceasefire helping to steady markets even as energy prices remained elevated.

Although sentiment remains sensitive to headlines around the Strait of Hormuz and energy markets, Franklin Templeton’s Emerging Markets Debt team sees an asset class that has shown it can absorb shocks, even as renewed geopolitical flare-ups or a broader risk-off episode could still test markets.

One of private equity’s biggest challenges right now is getting money back to investors. Advent and Cinven have just made a small dent in the industry’s mountain of unsold assets by agreeing the sale of TK Elevator to Finland’s Kone Oyj.

Streamlining the rules is undoubtedly appealing. The new proposal would do this, in part, by allowing the largest banks to use one method to calculate the risk of their assets instead of two, as currently required. That makes sense as far as it goes. Yet other requirements — including leverage ratios and certain capital surcharges — are being loosened or otherwise made more bank-friendly at the same time.

Artificial intelligence might be the most transformative technology ever devised. Exactly how its effects will work through the economy is impossible to say, but serious disruption of one kind or another seems likely. Millions of jobs — in the end, maybe most jobs — could radically change, and many will disappear entirely.