If you were considering taking the family on a European vacation, now may be a good time, as the U.S. dollar and euro achieved parity this week for the first time in 20 years.

These people, whose very job is to know the lessons of the past, either forgot them or chose to ignore them. Today we’ll look at how this manifested in the 2008 crisis period—and set up the conditions we face today.

With investors wondering whether we are finally through the worst of the selloff, our latest Strategic Income outlook tries to answer the question, “Are we there yet?”

As investment conditions become more difficult, many investors remain paralyzed, still enthralled by the charms of the Fed's QE program. That relationship no long works for investors so it is time to break up and do something different.

Investors are grappling with the reality of a new monetary backdrop in the US.

June’s U.S. inflation data will likely force central bankers into more restrictive territory – raising the odds of recession.

How many times have you heard that the US dollar will collapse because of Fed and fiscal policy?

This bear market we currently find us in is bringing tremendous opportunity.

One of the vexing questions for China watchers has been the lack of stimulus delivered, despite the maintenance of the government’s 5.5% GDP target for 2022 (although there is skepticism around the ability to reach that 5.5%).

Markets are expecting lower gasoline prices ahead.

Many of the participants in the short-term credit market use it as a place to deploy cash while waiting for higher risk opportunities.

As Robert Shiller has written, market participants are always in search of an explanatory narrative. J

The June jobs report was cheered by economic bulls given its strength in level terms, but rates of change among leading indicators don't favor a soft-landing outcome for the economy.

Global liquidity has tightened dramatically this year, which may be a headwind to global equity markets. However, not all central banks are tightening because not all countries have an inflation problem. Our latest research insight explains why we think Japan and China warrant a closer look.

Equity investors are anxious about the future after sharp market declines in the first half of 2022.

Headquartered in Brookfield, Connecticut, Photronics is a world leader in the critical photomasks used to manufacture semiconductor wafers.

In the first of a two-part series on the communications services sector, Mandana Hormozi of Franklin Mutual Series breaks down the streaming wars and uncovers hidden opportunities she sees within the rubble.

In a continuation of the first quarter, stocks and bonds struggled to find any sort of traction in the second quarter, leading to one of the roughest six-month starts to a calendar year on record.

Does the third quarter mean a new start to the year?

Sri Lanka is in turmoil.

There’s more pain ahead for still-frothy tech stocks…

Though risks are rising, strong hiring and purchase activity suggest that the economy can keep growing.

The “Fear Of Missing Out,” or “F.O.M.O.” is a centuries-old behavioral trait that began to get studied in 1996 by marketing strategist Dr. Dan Herman.

At -20%, the first half of this year officially went down as the worst 6-month period to start the year for the stock market (as measured by the S&P 500) since 1962 when it returned -22%.

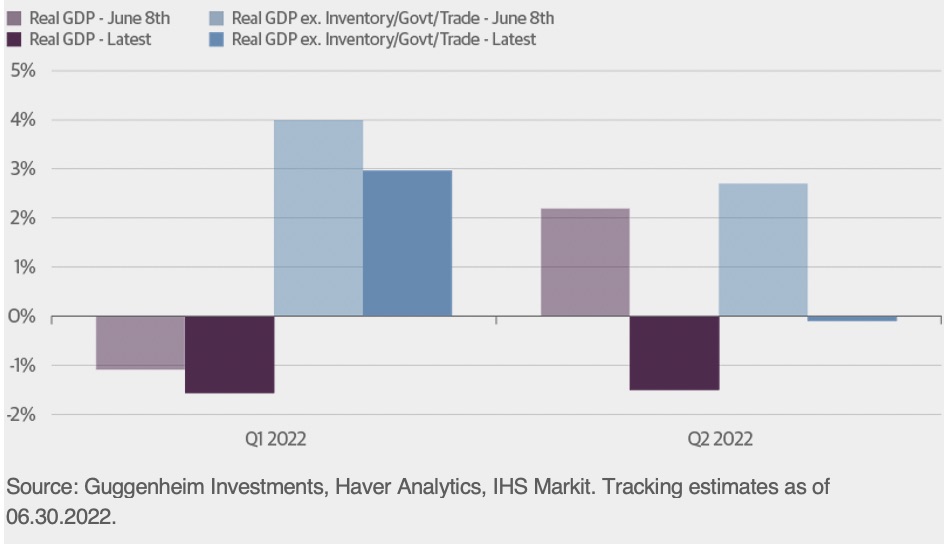

The path to lower inflation without causing a recession—the so-called “soft landing” —has been made significantly more challenging by the events of the last few months.

We believe index funds have immensely contributed to investors by permitting them to capture beta inexpensively.

Some investors think the US is already in a recession. As we wrote two weeks ago and as recent data have confirmed, we don’t think that’s the case.

Recent G-7 discussions about imposing caps on the price of Russian oil and gas have led to some head-scratching.

As Technical Research Analysts, we monitor indicators of internal stock market momentum, sentiment, and the like rather than studying individual company fundamentals.

The primary benefits offered by municipal bonds are generally well known to investors.

For the better part of the last decade, interest rates have been near zero and leverage has driven asset prices higher.

It’s a bull market for pessimism right now.

Gasoline consumers around the world, from families to businesses, have had to deal with record prices at the pump for months...

The economics profession has long had a vigorous academic argument over “natural” interest rates. What would rates be if we could somehow remove all the subjective actors—central banks, commercial lenders, government agencies—that conspire to set them? What would nature do if we left it alone?

Revenue above expectations, pandemic federal aid and reserves have strengthened states' financial outlook. But states will need to prepare as pandemic aid winds down and the economy slows.

Rough water is ahead, but equity markets may sail higher over the next 12 months...

Bear Market As a card-carrying self-appointed value investor, I relish a bear market and quite frankly recessions. To the astute and disciplined value investor, bear markets bring opportunity, and more to the point, safety. In this video, I will illustrate why I feel this way and why I believe you should as well.

Amid stormy markets, senior securitized credits hold potential for resilient returns.

Spiking inflation, rising interest rates and growing fears of a US recession dominated global equity markets in the second quarter. While the outlook is very cloudy, it’s important to evaluate what types of strategies can help investors in an economic downturn.

While a direct indexing strategy is a great addition to an investor’s portfolio, you’ll want to ensure your clients are properly diversified and also poised to reap the benefits of active management, while recognizing that active management doesn’t generate as many tax losses as tracking the index does.

The investing world seems highly uncertain these days. Investors are understandably having trouble balancing earnings, the Fed, fiscal policy, inflation, economic growth, disease control, and geo- and US politics. Read our latest report to learn about the two certain events that are central to our current portfolio positioning.

It’s a bull market for pessimism right now. We know the list of concerns is long and includes an aggressive Federal Reserve with a spotty (and that’s putting it kindly) track record of navigating a soft landing, stagflation, ongoing China lockdowns, disrupted supply chains, overly optimistic earnings estimates, the ongoing Russia-Ukraine war, and the latest—failing crypto firms.

The bond market is weird, but it’s full of clues. We have 8.6% inflation, but the highest interest rates have gone recently is about 3.4%, meaning real rates were still negative to the tune of 5%. This is confusing to me and a lot of other people.

Lao Tzu wrote, “A journey of a thousand miles begins with a single step.”

The Federal Reserve's pledge to curb inflation appears to have resonated with the market.

As an old saying states that statistics do not lie, but statisticians are darn liars.

As we move into the second half of 2022, there are lots of things to worry about.

The latest data suggest that we may already be in a recession.

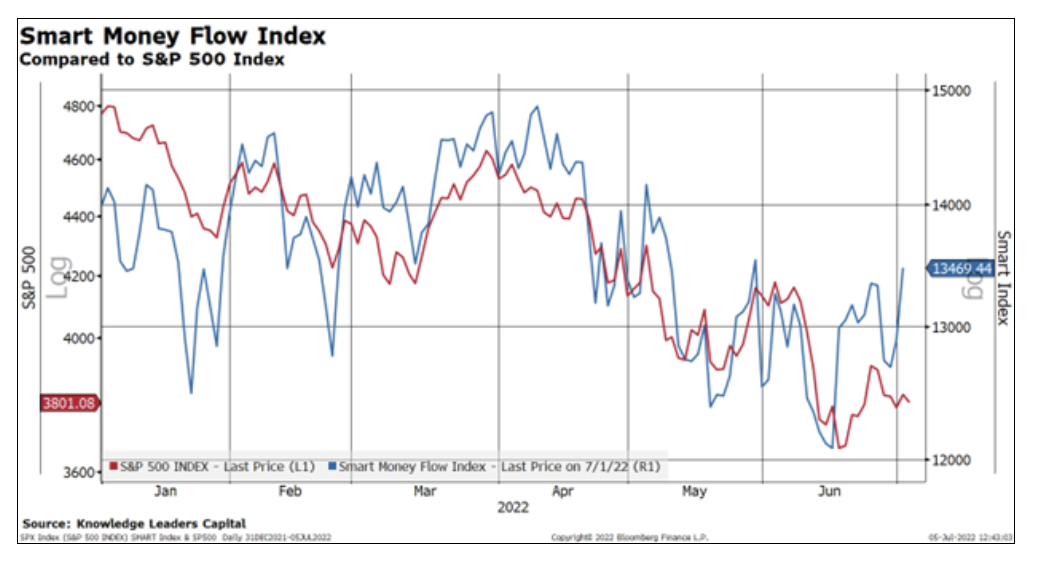

The Smart Money Index was constructed by Don Hays and measures the market action in the first half hour of trading and the last hour of trading.

Chris Galipeau, Senior Market Strategist of Putnam’s Capital Market Strategies group, recently spoke with Scott M. D’Orsi, CFA, a Portfolio Manager in Putnam’s Fixed Income group on the Active Insights podcast.